#asset backed loan

Text

Securing Your Future: Leveraging Asset-Backed Loans for Growth

In the pursuit of financial stability and growth, individuals and businesses often seek strategic avenues for securing capital. Asset-backed loans emerge as a viable solution, offering flexibility and accessibility while leveraging valuable assets as collateral. By exploring options such as asset backed loan, individuals and businesses can unlock the potential for growth and achieve their long-term financial objectives. This article delves into the benefits of asset-backed loans and how they can be utilized to secure your future effectively.

Understanding Asset-Backed Loans

An asset backed loan is a type of financing secured by tangible assets such as real estate, equipment, or inventory. Unlike unsecured loans, which rely solely on creditworthiness, asset-backed loans offer lenders added security, often resulting in more favorable terms and higher loan amounts. By pledging assets as collateral, borrowers can access capital to fund business expansion, consolidate debt, or pursue personal investments, all while retaining ownership and control over their assets.

Maximizing Returns with Fixed Deposits

For individuals seeking stability and guaranteed returns, fixed deposits represent a secure investment option. In Oman, where financial stability is paramount, investors often prioritize securing the highest fixed deposit rates in Oman to maximize returns on their savings. Fixed deposits offer a predictable stream of income with minimal risk, making them an attractive choice for conservative investors looking to safeguard their capital while earning competitive interest rates.

Empowering Consumers with Consumer Loans

Consumer loan provide individuals with access to funds for various personal expenses, such as home renovations, education, or healthcare. Unlike asset-backed loans, consumer loans are typically unsecured, meaning they do not require collateral. However, they may carry higher interest rates to compensate for the increased risk to lenders. By leveraging consumer loans, individuals can address immediate financial needs or pursue long-term goals without depleting their savings or liquidating assets.

Unlocking Growth Potential with Asset-Backed Loans

Asset-backed loans offer a unique opportunity for businesses to leverage existing assets to secure financing for growth initiatives. Whether expanding operations, purchasing equipment, or funding inventory, businesses can utilize asset backed loans to access capital quickly and efficiently. By pledging assets as collateral, businesses demonstrate their commitment to repayment, thereby enhancing their creditworthiness and potentially securing more favorable loan terms.

Diversifying Investment Portfolios

In addition to financing growth, asset-backed loan enable individuals to diversify their investment portfolios and optimize their wealth management strategies. By leveraging assets such as real estate or securities to secure loans, investors can access liquidity while maintaining exposure to asset appreciation potential. This approach allows investors to capitalize on investment opportunities without liquidating assets or disrupting long-term financial plans.

Conclusion

In conclusion, asset backed loans represent a powerful financial tool for individuals and businesses alike, offering the flexibility to access capital while leveraging valuable assets. Whether securing the highest fixed deposit rates in Oman for stable returns, utilizing consumer loans for personal expenses, or unlocking growth potential with asset-backed financing, individuals and businesses can secure their future effectively. By understanding the benefits and considerations of asset-backed loans, individuals and businesses can make informed decisions to optimize their financial strategies and achieve their long-term goals.

In summary, asset backed loans offer a versatile solution for securing capital and driving growth, providing individuals and businesses with the means to unlock their full financial potential. By leveraging valuable assets and exploring strategic financing options, individuals and businesses can navigate economic challenges, seize opportunities, and secure a prosperous future.

0 notes

Text

Someone just took a $14,500 loan on two Rolex watches at 12% APR, all on-chain, from an NFT-backed lending platform

Arcade, a de-fi lending platform for NFT, announced that someone took a loan on its platform, using two Rolex watches as collateral. The announcement said that the use of physical goods for on-chain transactions is opening up a new market for the decentralized finance space.

According to the physically backed NFT loan protocol platform, the transaction saw a borrower commit two Rolex watches for…

View On WordPress

#blockchain-secured loans#borrower uses Rolex watched for defi loan#cryptocurrency collateralized lending#digital asset financing#NFT lending platform#nft loan#non-fungible token borrowings#physically backed NFT lending#tokenization of assets

0 notes

Text

so apparently it's really fucking hard to get into the SAS. and ontop of that I've been getting tiktoks of people going around an army base asking why they joined. most responses were to pay off student loans, bills, school, (someone said there's was 6 years of prison or school and *mental note for idea*), the recruiter lied or spoilt them, barracks bunny.

141 (poly?) x notsobaddasssoldier!reader

and now i can't stop thinking of soldier!reader. who really half-assed their way through everything - only doing the job for the money and to pay off student loans + they had nothing better to do.

who somehow ends up being adopted by Price (kinda like Gaz i guess ???) all because reader happened to be in the right place at the right time and saved Price's ass while managing to complete a mission the Task Force were doing.

and it's not that you saved his ass or completed the mission that makes Price go *this is mine* - it's the fact that afterwards all you can say is-

"this shit is so not worth paying off my student loans."

"oh fuck i forgot to cancel my subscription. fuckk- waste of fucking money"

- all the while a building is burning in front of you but yeah just not at all concerned about what had just happened. so price just *grabs you by the back of your neck and holds you up, claiming you as part of his task force now.*

(lol you probably can't do that irl but this is fiction sooo suck my ass.)

and laswell's just like no... they are very much still green john. way too green. no.

but it's too late. he's already introducing you to the task force. singing your praises and you're just like

"man he promised to pay off my student loans and give me food." basically how ur recruiter got ya ass.

enough said. you get the whole off the books speech, saving the world by doing things others wouldn't like. but u couldn't give a rats ass - you should but nah...

and like... you know you're the rookie... you're still green... but some of the shit 141 do you just...

"so you just gonna kidnap the wife AND the child...? right... kid, you wanna watch bluey? here..."

"and you do this often...? crazy."

but you don't exactly protest. how could you with how much you get paid. you kinda just side-eye and look away when it's geta a lil crazy. *bombastic side-eye*

and the other 141 guys - oh my days. become just as enormed as price and want to start really trying to amplify your skills. but every time, they start explaining how to do things - the best way to go about a situation or how to fight a certain way.

you pull this face. like your top lip pulls back, your eyebrows scrunch together, and there's a slight frown on your lips as they speak. like you look confused/disgusted. but you don't even realise cause-

"why're you pulling that face?" 141

"that's... that's just my focusing face..."

"oh..." 141 feels bad

then when they do take you in feild you're shaking your head no. like you haven't been around that long. what the fuck? now you're bout to infiltrate an enemy base!?!?!

"can i just wait in the car?"

"no." price

"i'm gonna vomit."

"aim at the enemy." ghost

people think that because you're suddenly in this badass task force that surely they're just using you for your assets.

they all think you're the 141 barracks bunny. and maybe you should be pissed or annoyed or grossed out. but all you can do is sigh and pause from the burger price got you, and let out a long exhale.

"fuck... maybe i can just do onlyfans or be a pornstar... shit maybe it's not too late..."

"military is bascially sex work - selling my body..."

"not that different from what i'm doing now. body being used, check. body sore in the strangest places, check."

your tone so empty, blank and nonchalant, but there's a serious look in your eyes that when you grab your phone out to maybe do a little research on how you could do that, your phone is snatched from your hand by one of the guys and they walk out the room without a second look back.

with an annoyed huff, you go back to eating your burger. but suddenly, you turn to the person who genuinely thought you were a barracks bunny.

"hey you think if i be a barracks bunny i get out of missions and shit?"

"...that's not how it works..." rando.

"fuck."

and maybe you try...

like you go to price's office and the guys are already in there, chatting about something that you should really pay attention too but you can't be assed. instead you unashamedly start to speak...

"if i suck ya'll dicks can i get out the mission?"

"no. you still have to join." gaz says amused

"even if you-" *que long sigh from price* "even if you suck our dicks."

"that's fucked up. i should've done porn."

and with the most hurt and broken-hearted look on your face, you leave the office, closing the door with a dramatic sigh. the guys just stare at the door in... confusion, amusement, and maybe arousal if ya'll dig that

idk man just gimmie more soldier!reader who just really ain't the fucked, there for money, lowkey hungry and doesn't know what the fuck is happening. kinda a pet or little sibling energy that the 141 love.

bonus*

"wait so they aren't sucking our dicks?" *soap says getting slapped in the back of the head by ghost

a/n: brain is rottinnggg. i should be doing so much other shit but... cod just consumes my brain 24/7

#my post#x reader#poly 141#poly 141 x reader#john price x reader#kyle gaz garrick#simon ghost riley#kyle garrick x reader#simon riley x reader#johnny mactavish#johnny mactavish x reader#johnny soap mactavish#captain price x reader#captain john price x reader#platonic 141#?#task force x reader#task force 141#platonic!141 x reader#boowrites#cod mwii#mwii#cod#simon riley#ghost x reader#kyle gaz garrick x reader#simon ghost riley x reader#cod mwii imagines

3K notes

·

View notes

Text

Things Biden and the Democrats did, this week #19

May 17-24 2024

President Biden wiped out the student loan debt of 160,000 more Americans. This debt cancellation of 7.7 billion dollars brings the total student loan debt relieved by the Biden Administration to $167 billion. The Administration has canceled student loan debt for 4.75 million Americans so far. The 160,000 borrowers forgiven this week owned an average of $35,000 each and are now debt free. The Administration announced plans last month to bring debt forgiveness to 30 million Americans with student loans coming this fall.

The Department of Justice announced it is suing Ticketmaster for being a monopoly. DoJ is suing Ticketmaster and its parent company Live Nation for monopolistic practices. Ticketmaster controls 70% of the live show ticket market leading to skyrocketing prices, hidden fees and last minute cancellation. The Justice Department is seeking to break up Live Nation and help bring competition back into the market. This is one of a number of monopoly law suits brought by the Biden administration against Apple in March and Amazon in September 2023.

The EPA announced $225 million in new funding to improve drinking and wastewater for tribal communities. The money will go to tribes in the mainland US as well as Alaska Native Villages. It'll help with testing for forever chemicals, and replacing of lead pipes as well as sustainability projects.

The EPA announced $300 million in grants to clean up former industrial sites. Known as "Brownfield" sites these former industrial sites are to be cleaned and redeveloped into community assets. The money will fund 200 projects across 178 communities. One such project will transform a former oil station in Philadelphia’s Kingsessing neighborhood, currently polluted with lead and other toxins into a waterfront bike trail.

The Department of Agriculture announced a historic expansion of its program to feed low income kids over the summer holidays. Since the 1960s the SUN Meals have served in person meals at schools and community centers during the summer holidays to low income children. This Year the Biden administration is rolling out SUN Bucks, a $120 per child grocery benefit. This benefit has been rejected by many Republican governors but in the states that will take part 21 million kids will benefit. Last year the Biden administration introduced SUN Meals To-Go, offering pick-up and delivery options expanding SUN's reach into rural communities. These expansions are part of the Biden administration's plan to end hunger and reduce diet-related disease by 2030.

Vice-President Harris builds on her work in Africa to announce a plan to give 80% of Africa internet access by 2030, up from just 40% today. This push builds off efforts Harris has spearheaded since her trip to Africa in 2023, including $7 billion in climate adaptation, resilience, and mitigation, and $1 billion to empower women. The public-private partnership between the African Development Bank Group and Mastercard plans to bring internet access to 3 million farmers in Kenya, Tanzania, and Nigeria, before expanding to Uganda, Ethiopia, and Ghana, and then the rest of the continent, bring internet to 100 million people and businesses over the next 10 years. This is together with the work of Partnership for Digital Access in Africa which is hoping to bring internet access to 80% of Africans by 2030, up from 40% now, and just 30% of women on the continent. The Vice-President also announced $1 billion for the Women in the Digital Economy Fund to assure women in Africa have meaningful access to the internet and its economic opportunities.

The Senate approved Seth Aframe to be a Judge on the US Court of Appeals for the First Circuit, it also approved Krissa Lanham, and Angela Martinez to district Judgeships in Arizona, as well as Dena Coggins to a district court seat in California. Bring the total number of judges appointed by President Biden to 201. Biden's Judges have been historically diverse. 64% of them are women and 62% of them are people of color. President Biden has appointed more black women to federal judgeships, more Hispanic judges and more Asian American judges and more LGBT judges than any other President, including Obama's full 8 years in office. President Biden has also focused on backgrounds appointing a record breaking number of former public defenders to judgeships, as well as labor and civil rights lawyers.

#Thanks Biden#Joe Biden#kamala harris#student loans#student loan forgiveness#ticketmaster#Africa#free lunch#hunger#poverty#internet#judges#politics#us politics#american politics

1K notes

·

View notes

Text

Asset Backed Securities

Securitisation or structured finance is a central cog in the global economic machinery. Securitised assets are pools of re-packaged homogeneous illiquid assets linked to security interest payments emanating from the steady cash flows generated from the asset or loan pool.

0 notes

Text

Elon Musk must have a humiliation fetish.

I wonder if it felt good, deliciously forbidden, nice and naughty when he went on his hands and knees to beg other companies to loan him money, or when he had to liquidate his assets, lying on his back like a little submissive dog.

He claims he only bought Twitter so he could unban Donald Trump.

Who notoriously said this about Musk:

See?

Elon Musk must get off to this kind of talk.

He likes it when other rich men verbally abuse him like a bad little puppy.

He must get off, trundling on all fours, little anal plug tail tucked between his legs.

He must like it when daddy trump embarrasses him publicly.

I suppose I can understand humiliation fetishes...I just wish he didn't have to anal fuck American democracy at the same time.

Keep your kinks in the bedroom please.

Donald Trump can whip your balls at his mansion.

We don't need to see him do it on Twitter.

We didn't consent to your humiliation play, Muskrat.

4K notes

·

View notes

Text

Wealth Building: Money Topics You Should Learn About If You Want To Make More Money

Budgeting: This means keeping track of how much money you have and how you spend it. It helps you save money and plan for your needs.

Investing: This is like putting your money to work so it can grow over time. It's like planting seeds to grow a money tree.

Saving: Saving is when you put some money aside for later. It's like keeping some of your treats for another day.

Debt Management: This is about handling money you owe to others, like loans or credit cards. You want to pay it back without owing too much.

Credit Scores: Think of this like a report card for your money habits. It helps others decide if they can trust you with money.

Taxation: Taxes are like a fee you pay to the government. You need to understand how they work and how to pay them correctly.

Retirement Planning: This is making sure you have enough money to live comfortably when you're older and no longer working.

Estate Planning: This is like making a plan for your stuff and money after you're no longer here.

Insurance: It's like paying for protection. You give some money to an insurance company, and they help you if something bad happens.

Investment Options: These are different ways to make your money grow, like buying parts of companies or putting money in a savings account.

Financial Markets: These are places where people buy and sell things like stocks and bonds. It can affect your investments.

Risk Management: This is about being careful with your money and making smart choices to avoid losing it.

Passive Income: This is money you get without having to work for it, like rent from a property you own.

Entrepreneurship: It's like starting your own business. You create something and try to make money from it.

Behavioral Finance: This is about understanding how your feelings and thoughts can affect how you use money. You want to make good choices even when you feel worried or excited.

Financial Goals: These are like wishes for your money. You need a plan to make them come true.

Financial Tools and Apps: These are like helpers on your phone or computer that can make it easier to manage your money.

Real Estate: This is about buying and owning property, like a house or land, to make money.

Asset Protection: It's about keeping your money safe from problems or people who want to take it.

Philanthropy: This means giving money to help others, like donating to charities or causes you care about.

Compounding Interest: This is like a money snowball. When you save or invest your money, it can grow over time. As it grows, you earn even more money on the money you already earned.

Credit Cards: When you borrow money or use a credit card to buy things, you need to show you can pay it back on time. This helps you build a good reputation with money. The better your reputation, the easier it is to borrow more money when you need it.

Alternate Currencies: These are like different kinds of money that aren't like the coins and bills you're used to like Crypto. It's digital money that's not controlled by a government. Some people use it for online shopping, and others think of it as a way to invest, like buying special tokens for a game.

885 notes

·

View notes

Text

i guess im doing more of these.

meet the female scout! she's the daughter of a crime family from los angeles. speaks with a bit of a valley girl accent(of course), and has a keen interest in fashion and money. luckily for her, the gravel wars have a lot of the latter. not so much of the former.

the female scout is similar to the scout in that she's not so much a fighter as much as she is a very good athlete. the perks of coming from a rich background means that she has a wide array of proficiencies, from sprinting to croquet(her favourite game), she's perfect for her role as a scout on her team.

before her time as a mercenary on RED, the family which the female scout is from took a favour from Saxton Hale, helping them gain more power in Los Angeles by giving them firearms. Saxton thought that they were going to use them to take more control by force, but it turns out that they just sold the guns for money. He didn't mind though, seeing as how they owed him and he was going to get his money back one way or another.

And he did come back eventually, looking for payment for the loans. Not wanting to actually pay him back, the family gave them their only daughter, soon to be known as the female scout, as an asset to the company.

Saxton, having no need for her, took her in anyway and gave her off to Miss Pauling for the Gravel Wars instead. The female scout has been fighting ever since.

the female scout wasn't exactly told why she was going to the war, other than she needed to "prove herself to be a worthy member of the family" and to take her first steps into the adult world.

well, if the adult world consisted of having piss thrown at them and people running around naked and covered in honey, then she was more than prepared by the end of her first week. however, despite the female scout's more snobbish personality, she has a bit of a strange way of viewing the world.

coming from high crime, she's not unfamiliar to the more dubious surgical practices of the medic and is only surprised that he actually puts his patients back together instead of burying somewhere remote. blood and guts is all game as long as it doesn't stain her clothes. good thing everyone wears red.

#tf2#team fortress 2#scout tf2#tf2 femscout#idk i feel like her name would be lucy#but i dont really want to give names out yet#jeremy probably tries to get with her#but she thinks shes totally out of his league#miss pauling however???#headcanonning that shes cousins with bidwell#explains why they have contacts with australians#my art

564 notes

·

View notes

Text

THIS ISN'T COMMON KNOWLEDGE BUT SHOULD BE...ABOUT MEDICAID....

If you ever find yourself in the position of living in the home of a parent who is disabled and requires full-time care and you are their primary caregiver for at least 2 years, and they intend to leave their assets to you after they pass, make sure to transfer ownership of their assets, home/land in your name ASAP...or they will require you to pay back any benefits received and claim those assets even out from under you, as soon as your loved one passes.

This is yet another way that generational assets /wealth are easily taken out of marginalized communities.

It is a loan.

And the sharks circle as soon as your loved one passes.

Here's an article about it:

Decided to add context.

I don't like to talk about it here, because ehh, social media is for my vapid entertainment thoughts for me.

It's a hobby/getaway/ place to get semi-social with strangers and online friends with shared interests, but I don't want anyone else to go through what I am... Of course, this applies specifically to the U.S.'s broken healthcare system.

So, for those who don't know, my mom passed recently. I am an only child with no siblings or children. My whole life during that time was 24/7 care.

She had insurance, but it wasn't enough to cover everything that she needed, so Medicaid was the obvious solution, right?

The government takes care of our disabled elderly who have worked until retirement, right?

It seemed like the routine thing to do, I had never heard anything during the process about having to pay it back,but sure enough, less than 12 weeks after her passing, I was hit with a warning (which I followed up on and was told I would NOT be charged because of my caregiver status) and then 2 weeks later the "bill".

The lady I spoke to, totally changed her attitude from the first time I spoke to her to the point where I felt scammed. Out came a patronizing voice certain people use with children, that measured whiny thing (it's always a red-flag to me and makes me instantly dislike you if you do this even with kids, btw... speak to kids like PEOPLE).

I feel like an idiot.

I have been doing this for over a decade and didn't think to transfer any assets of hers during that time because it *was* hers.

I wanted her to feel as empowered about that as possible.

Not a single soul said I should transfer those assets to keep this from happening and now I'm facing down what feels like some kind of weird conspiracy to take the land and house.

FYI, there have been weird inquiries, the census came to mark down my mother's death literally *immediately* after she passed...and odd timing called the day of the notice to "help", with all the southern Christian signifiers (bless your heart we'll be praying for you)....

It feels so seedy.

Anyway, all this to say if you find yourself in a similar position....

TRANSFER THOSE ASSETS INTO YOUR NAME 2 years into caregiving or they will take them from you, house etc..

#medicaid#currently dealing with this#hoping to get a waiver#I'm doing what i can to navigate the system...I hope to negotiate a lower settlement or something... I can pay part since I did save some#I am terrified and coming off some illnesses myself#I am working on it with someone (s) who has some knowledge of the system#whatever happens I'll keep you updated...again if/when there's a solution I'll share to help others PASS ALONG this knowledge#to all you know this could potentially effect

383 notes

·

View notes

Text

Maximizing Capital: Asset-Backed Loans vs. Financing from Large Corporates

In the realm of business financing, two popular methods stand out for companies looking to maximize their capital efficiently: asset-backed loans and financing from large corporate houses. Each financing method offers unique benefits and caters to different needs and scenarios. This article delves into the nuances of asset-backed loans and financing from large corporate houses, including specialized options like pre-owned vehicle loans, to help businesses make informed decisions.

Understanding Asset-Backed Loans

An asset-backed loan is a type of financing secured by an asset. This means that the loan is backed by collateral, such as real estate, inventory, or other tangible assets. The primary advantage of an asset-backed loan is that it typically offers lower interest rates due to the reduced risk for lenders. Businesses can leverage assets that they already own to obtain funding, which can be particularly advantageous for small to medium enterprises (SMEs) that might not have extensive credit histories.

The flexibility of asset-backed loans is also seen in specific variants like pre-owned vehicle loans. These are a form of asset-backed loan where the purchased vehicle itself serves as collateral. Pre-owned vehicle loans can be a cost-effective option for businesses needing to expand their operational fleet without the hefty price tag of new vehicles.

The Role of Financing from Large Corporate Houses

On the other side of the spectrum, fd from large corporate houses refers to funding provided by major corporations, often in the form of loans or lines of credit. This type of financing is typically targeted at larger, more established companies that require substantial amounts of capital. One of the key benefits of financing from large corporate houses is the potential for tailored financing solutions that align with specific business needs and growth strategies.

Moreover, businesses often turn to financing from large corporate houses for strategic investments due to the potential for larger loan amounts and longer repayment periods. This form of financing can be particularly useful for companies looking to make significant capital investments or undergo large-scale expansions.

Comparing the Two Options

When comparing asset-backed loans to financing from large corporate houses, several factors need to be considered. Asset-backed loans are generally more accessible for SMEs and offer quicker disbursement of funds, which can be crucial for immediate business needs. On the other hand, financing from large corporate houses may offer more competitive interest rates for large borrowing amounts but usually requires a more rigorous approval process.

Pre-owned vehicle loan, as a subset of asset-backed loans, provide a practical example of how assets can be efficiently used to support business operations without the extensive credit requirements or the need to engage with large corporate financing options.

Strategic Considerations

Choosing between an asset-backed loan and financing from large corporate houses depends largely on the specific needs and circumstances of the business. For companies with solid credit histories and a need for large-scale funding, financing from large corporate houses could be the way forward. Conversely, for businesses that require quick funding or have unutilized assets, asset-backed loans might be the more practical choice.

In particular, businesses looking to acquire vehicles might find pre-owned vehicle loans advantageous due to their lower cost and the straightforward nature of the collateral arrangement. This makes pre-owned vehicle loans an attractive option for companies keen on optimizing their capital expenditures.

Conclusion

In conclusion, both asset-backed loans and financing from large corporate houses offer viable pathways for businesses to secure the necessary capital for growth and operational efficiency. By understanding the benefits and limitations of each, businesses can strategically choose the option that best suits their needs, whether it's leveraging assets for an asset-backed loan or utilizing financing from large corporate houses for more substantial financial support. As businesses consider their options, including pre-owned vehicle loans, it's clear that the right financing choice can significantly impact their capital optimization and long-term success.

0 notes

Text

The CHIPS Act treats the symptoms, but not the causes

If you'd like an essay-formatted version of this post to read or share, here's a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2024/02/07/farewell-mr-chips/#we-used-to-make-things

There's this great throwaway line in 1992's Sneakers, where Dan Aykroyd, playing a conspiracy-addled hacker/con-man, is feverishly telling Sydney Poitier (playing an ex-CIA spook) about a 1958 meeting Eisenhower had with aliens where Ike said, "hey, look, give us your technology, and we'll give you all the cow lips you want."

Poitier dismisses Aykroyd ("Don't listen to this man. He's certifiable"). We're meant to be on Poitier's side here, but I've always harbored some sympathy for Aykroyd in this scene.

That's because I often hear echoes of Aykroyd's theory in my own explanations of the esoteric bargains and plots that produced the world we're living in today. Of course, in my world, it's not presidents bargaining for alien technology in exchange for cow-lips – it's the world's wealthy nations bargaining to drop trade restrictions on the Global South in exchange for IP laws.

These bargains – which started as a series of bilateral and then multilateral agreements like NAFTA, and culminated in the WTO agreement of 1999 – were the most important step in the reordering of the world's economy around rent-extraction, cheap labor exploitation, and a brittle supply chain that is increasingly endangered by the polycrisis of climate and its handmaidens, like zoonotic plagues, water wars, and mass refugee migration.

Prior to the advent of "free trade," the world's rich countries fashioned debt into a whip-hand over poor, post-colonial nations. These countries had been bankrupted by their previous colonial owners, and the price of their freedom was punishing debts to the IMF and other rich-world institutions in exchange for loans to help these countries "develop."

Like all poor debtors, these countries were said to have gotten into their predicament through moral failure – they'd "lived beyond their means."

(When rich people get into debt, bankruptcy steps in to give them space to "restructure" according to their own plans. When poor people get into debt, bankruptcy strips them of nearly everything that might help them recover, brands them with a permanent scarlet letter, and subjects them to humiliating micro-management whose explicit message is that they are not competent to manage their own affairs):

https://pluralistic.net/2021/08/07/hr-4193/#shoppers-choice

So the poor debtor nations were ordered to "deregulate." They had to sell off their state assets, run their central banks according to the dictates of rich-world finance authorities, and reorient their production around supplying raw materials to rich countries, who would process these materials into finished goods for export back to the poor world.

Naturally, poor countries were not allowed to erect "trade barriers" that might erode the capacity of this North-South transfer of high-margin goods, but this was not the era of free trade. It wasn't the free trade era because, while the North-South transfer was largely unrestricted, the South-North transfer was subject to tight regulation in the rich world.

In other words, poor countries were expected to export, say, raw ore to the USA and reimport high-tech goods, with low tariffs in both directions. But if a poor country processed that ore domestically and made its own finished goods, the US would block those goods at the border, slapping them with high tariffs that made them more expensive than Made-in-the-USA equivalents.

The argument for this unidirectional trade was that the US – and other rich countries – had a strategic need to maintain their manufacturing industries as a hedge against future geopolitical events (war, but also pandemics, extreme weather) that might leave the rich world unable to provide for itself. This rationale had a key advantage: it was true.

A country that manages its own central bank can create as much of its own currency as it wants, and use that money to buy anything for sale in its own currency.

This may not be crucial while global markets are operating to the country's advantage (say, while the rest of the world is "willingly" pricing its raw materials in your country's currency), but when things go wrong – war, plague, weather – a country that can't make things is at the rest of the world's mercy.

If you had to choose between being a poor post-colonial nation that couldn't supply its own technological needs except by exporting raw materials to rich countries, and being a rich country that had both domestic manufacturing capacity and a steady supply of other countries' raw materials, you would choose the second, every time.

What's not to like?

Here's what.

The problem – from the perspective of America's ultra-wealthy – was that this arrangement gave the US workforce a lot of power. As US workers unionized, they were able to extract direct concessions from their employers through collective bargaining, and they could effectively lobby for universal worker protections, including a robust welfare state – in both state and federal legislatures. The US was better off as a whole, but the richest ten percent were much poorer than they could be if only they could smash worker power.

That's where free trade comes in. Notwithstanding racist nonsense about "primitive" countries, there's no intrinsic defect that stops the global south from doing high-tech manufacturing. If the rich world's corporate leaders were given free rein to sideline America's national security in favor of their own profits, they could certainly engineer the circumstances whereby poor countries would build sophisticated factories to replace the manufacturing facilities that sat behind the north's high tariff walls.

These poor-country factories could produce goods ever bit as valuable as the rich world's shops, but without the labor, environmental and financial regulations that constrained their owners' profits. They slavered for a business environment that let them kill workers; poison the air, land and water; and cheat the tax authorities with impunity.

For this plan to work, the wealthy needed to engineer changes in both the rich world and the poor world. Obviously, they would have to get rid of the rich world's tariff walls, which made it impossible to competitively import goods made in the global south, no matter how cheaply they were made.

But free trade wasn't just about deregulation in the north – it also required a whole slew of new, extremely onerous regulations in the global south. Corporations that relocated their manufacturing to poor – but nominally sovereign – countries needed to be sure that those countries wouldn't try to replicate the American plan of becoming actually sovereign, by exerting control over the means of production within their borders.

Recall that the American Revolution was inspired in large part by fury over the requirement to ship raw materials back to Mother England and then buy them back at huge markups after they'd been processed by English workers, to the enrichment of English aristocrats. Post-colonial America created new regulations (tariffs on goods from England), and – crucially – they also deregulated.

Specifically, post-revolutionary America abolished copyrights and patents for English persons and firms. That way, American manufacturers could produce sophisticated finished goods without paying rent to England's wealthy making those goods cheaper for American buyers, and American publishers could subsidize their editions of American authors' books by publishing English authors on the cheap, without the obligation to share profits with English publishers or English writers.

The surplus produced by ignoring the patents and copyrights of the English was divided (unequally) among American capitalists, workers, and shoppers. Wealthy Americans got richer, even as they paid their workers more and charged less for their products. This incubated a made-in-the-USA edition of the industrial revolution. It was so successful that the rest of the world – especially England – began importing American goods and literature, and then American publishers and manufacturers started to lean on their government to "respect" English claims, in order to secure bilateral protections for their inventions and books in English markets.

This was good for America, but it was terrible for English manufacturers. The US – a primitive, agricultural society – "stole" their inventions until they gained so much manufacturing capacity that the English public started to prefer American goods to English ones.

This was the thing that rich-world industrialists feared about free trade. Once you build your high-tech factories in the global south, what's to stop those people from simply copying your plans – or worse, seizing your factories! – and competing with you on a global scale? Some of these countries had nominally socialist governments that claimed to explicitly elevate the public good over the interests of the wealthy. And all of these countries had the same sprinkling of sociopaths who'd gladly see a million children maimed or the land poisoned for a buck – and these "entrepreneurs" had unbeatable advantages with their countries' political classes.

For globalization to work, it wasn't enough to deregulate the rich world – capitalists also had to regulate the poor world. Specifically, they had to get the poor world to adopt "IP" laws that would force them to willingly pay rent on things they could get for free: patents and other IP, even though it was in the short-term, medium-term, and long-term interests of both the nation and its politicians and its businesspeople.

Thus, the bargain that makes me sympathetic to Dan Aykroyd: not cow lips for alien tech; but free trade for IP law. When the WTO was steaming towards passage in the late 1990s, there was (rightly) a lot of emphasis on its deregulatory provisions: weakening of labor, environmental and financial laws in the poor world, and of tariffs in the rich world.

But in hindsight, we all kind of missed the main event: the TRIPS (Agreement on Trade-Related Aspects of Intellectual Property Rights). This actually started before the WTO treaty (it was part of the GATT, a predecessor to the WTO), but the WTO spread it to countries all over the world. Under the TRIPS, poor countries are required to honor the IP claims of rich countries, on pain of global sanction.

That was the plan: instead of paying American workers to make Apple computers, say, Apple could export the "IP" for Macs and iPhones to countries like China, and these countries would produce Apple products that were "designed in California, assembled in China." China would allow Apple to treat Chinese workers so badly that they routinely committed suicide, and would lock up or kill workers who tried to unionize. China would accept vast shipments of immortal, toxic e-waste. And China wouldn't let its entrepreneurs copy Apple's designs, be they software, schematics or trademarks.

Apple isn't the only company that pursued this strategy, but no company has executed it as successfully. It's not for nothing that Steve Jobs's hand-picked successor was Tim Cook, who oversaw the transfer of even the most exacting elements of Apple manufacturing to Chinese facilities, striking bargains with contractors like Foxconn that guaranteed that workers would be heavily – lethally! – surveilled and controlled to prevent the twin horrors of unionization and leaks.

For the first two decades of the WTO era, the most obvious problems with this arrangement was wage erosion (for American workers) and leakage (for the rich). China's "socialist" government was only too happy to help Foxconn imprison workers who demanded better wages and working conditions, but they were far more relaxed about knockoffs, be they fake iPods sold in market stalls or US trade secrets working their way into Huawei products.

These were problems for the American aristocracy, whose investments depended on China disciplining both Chinese workers and Chinese businesses. For the American people, leakage was a nothingburger. Apple's profits weren't shared with its workforce beyond the relatively small number of tech workers at its headquarters. The vast majority of Apple employees, who flogged iPhones and scrubbed the tilework in gleaming white stores across the nation, would get the same minimal (or even minimum) wage no matter how profitable Apple grew.

It wasn't until the pandemic that the other shoe dropped for the American public. The WTO arrangement – cow lips for alien technology – had produced a global system brittle supply chains composed entirely of weakest links. A pandemic, a war, a ship stuck in the Suez Canal or Houthi paramilitaries can cripple the entire system, perhaps indefinitely.

For two decades, we fought over globalization's effect on wages. We let our corporate masters trick us into thinking that China's "cheating" on IP was a problem for the average person. But the implications of globalization for American sovereignty and security were banished to the xenophobic right fringe, where they were mixed into the froth of Cold War 2.0 nonsense. The pandemic changed that, creating a coalition that is motivated by a complex and contradictory stew of racism, environmentalism, xenophobia, labor advocacy, patriotism, pragmatism, fear and hope.

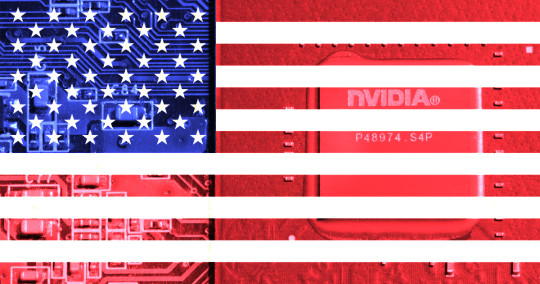

Out of that stew emerged a new American political tendency, mostly associated with Bidenomics, but also claimed in various guises by the American right, through its America First wing. That tendency's most visible artifact is the CHIPS Act, through which the US government proposes to use policy and subsidies to bring high-tech manufacturing back to America's shores.

This week, the American Economic Liberties Project published "Reshoring and Restoring: CHIPS Implementation for a Competitive Semiconductor Industry," a fascinating, beautifully researched and detailed analysis of the CHIPS Act and the global high-tech manufacturing market, written by Todd Achilles, Erik Peinert and Daniel Rangel:

https://www.economicliberties.us/our-work/reshoring-and-restoring-chips-implementation-for-a-competitive-semiconductor-industry/#

Crucially, the report lays out the role that the weakening of antitrust, the dismantling of tariffs and the strengthening of IP played in the history of the current moment. The failure to enforce antitrust law allowed for monopolization at every stage of the semiconductor industry's supply-chain. The strengthening of IP and the weakening of tariffs encouraged the resulting monopolies to chase cheap labor overseas, confident that the US government would punish host countries that allowed their domestic entrepreneurs to use American designs without permission.

The result is a financialized, "capital light" semiconductor industry that has put all its eggs in one basket. For the most advanced chips ("leading-edge logic"), production works like this: American firms design a chip and send the design to Taiwan where TSMC foundry turns it into a chip. The chip is then shipped to one of a small number of companies in the poor world where they are assembled, packaged and tested (AMP) and sent to China to be integrated into a product.

Obsolete foundries get a second life in the commodity chip ("mature-node chips") market – these are the cheap chips that are shoveled into our cars and appliances and industrial systems.

Both of these systems are fundamentally broken. The advanced, "leading-edge" chips rely on geopolitically uncertain, heavily concentrated foundries. These foundries can be fully captured by their customers – as when Apple prepurchases the entire production capacity of the most advanced chips, denying both domestic and offshore competitors access to the newest computation.

Meanwhile, the less powerful, "mature node" chips command minuscule margins, and are often dumped into the market below cost, thanks to subsidies from countries hoping to protect their corner of the high-tech sector. This makes investment in low-power chips uncertain, leading to wild swings in cost, quality and availability of these workhorse chips.

The leading-edge chipmakers – Nvidia, Broadcom, Qualcomm, AMD, etc – have fully captured their markets. They like the status quo, and the CHIPS Act won't convince them to invest in onshore production. Why would they?

2022 was Broadcom's best year ever, not in spite of its supply-chain problems, but because of them. Those problems let Broadcom raise prices for a captive audience of customers, who the company strong-armed into exclusivity deals that ensured they had nowhere to turn. Qualcomm also profited handsomely from shortages, because its customers end up paying Qualcomm no matter where they buy, thanks to Qualcomm ensuring that its patents are integrated into global 4G and 5G standards.

That means that all standards-conforming products generate royalties for Qualcomm, and it also means that Qualcomm can decide which companies are allowed to compete with it, and which ones will be denied licenses to its patents. Both companies are under orders from the FTC to cut this out, and both companies ignore the FTC.

The brittleness of mature-node and leading-edge chips is not inevitable. Advanced memory chips (DRAM) roughly comparable in complexity to leading-edge chips, while analog-to-digital chips are as easily commodified as mature-node chips, and yet each has a robust and competitive supply chain, with both onshore and offshore producers. In contrast with leading-edge manufacturers (who have been visibly indifferent to the CHIPS incentives), memory chip manufacturers responded to the CHIPS Act by committing hundreds of billions of dollars to new on-shore production facilities.

Intel is a curious case: in a world of fabless leading-edge manufacturers, Intel stands out for making its own chips. But Intel is in a lot of trouble. Its advanced manufacturing plans keep foundering on cost overruns and delays. The company keeps losing money. But until recently, its management kept handing its shareholders billions in dividends and buybacks – a sign that Intel bosses assume that the US public will bail out its "national champion." It's not clear whether the CHIPS Act can save Intel, or whether financialization will continue to hollow out a once-dominant pioneer.

The CHIPS Act won't undo the concentration – and financialization – of the semiconductor industry. The industry has been awash in cheap money since the 2008 bailouts, and in just the past five years, US semiconductor monopolists have paid out $239b to shareholders in buybacks and dividends, enough to fund the CHIPS Act five times over. If you include Apple in that figure, the amount US corporations spent on shareholder returns instead of investing in capacity rises to $698b. Apple doesn't want a competitive market for chips. If Apple builds its own foundry, that just frees up capacity at TSMC that its competitors can use to improve their products.

The report has an enormous amount of accessible, well-organized detail on these markets, and it makes a set of key recommendations for improving the CHIPS Act and passing related legislation to ensure that the US can once again make its own microchips. These run a gamut from funding four new onshore foundries to requiring companies receiving CHIPS Act money to "dual-source" their foundries. They call for NIST and the CPO to ensure open licensing of key patents, and for aggressive policing of anti-dumping rules for cheap chips. They also seek a new law creating an "American Semiconductor Supply Chain Resiliency Fee" – a tariff on chips made offshore.

Fundamentally, these recommendations seek to end the outsourcing made possible by restrictive IP regimes, to undercut Wall Street's power to demand savings from offshoring, and to smash the market power of companies like Apple that make the brittleness of chip manufacturing into a feature, rather than a bug. This would include a return to previous antitrust rules, which limited companies' ability to leverage patents into standards, and to previous IP rules, which limited exclusive rights chip topography and design ("mask rights").

All of this will is likely to remove the constraints that stop poor countries from doing to America the same things that postcolonial America did to England – that is, it will usher in an era in which lots of countries make their own chips and other high-tech goods without paying rent to American companies. This is good! It's good for poor countries, who will have more autonomy to control their own technical destiny. It's also good for the world, creating resiliency in the high-tech manufacturing sector that we'll need as the polycrisis overwhelms various places with fire and flood and disease and war. Electrifying, solarizing and adapting the world for climate resilience is fundamentally incompatible with a brittle, highly concentrated tech sector.

Pluralizing high-tech production will make America less vulnerable to the gamesmanship of other countries – and it will also make the rest of the world less vulnerable to American bullying. As Henry Farrell and Abraham Newman describe so beautifully in their 2023 book Underground Empire, the American political establishment is keenly aware of how its chokepoints over global finance and manufacturing can be leveraged to advantage the US at the rest of the world's expense:

https://pluralistic.net/2023/10/10/weaponized-interdependence/#the-other-swifties

Look, I know that Eisenhower didn't trade cow-lips for alien technology – but our political and commercial elites really did trade national resiliency away for IP laws, and it's a bargain that screwed everyone, except the one percenters whose power and wealth have metastasized into a deadly cancer that threatens the country and the planet.

Image:

Mickael Courtiade (modified)

https://www.flickr.com/photos/197739384@N07/52703936652/

CC BY 2.0

https://creativecommons.org/licenses/by/2.0/

#pluralistic#chips act#ip#monopolies#antitrust#national security#industrial policy#american economic liberties project#tmsc#leading-edge#intel#mature node#lagging edge#foundries#fabless

251 notes

·

View notes

Text

On Wednesday, Senate Health, Education, Labor and Pensions (HELP) Chair Bernie Sanders (I-Vermont) and Rep. Pramila Jayapal (D-Washington) reintroduced a proposal to make higher education free at public schools for most Americans — and pay for it by taxing Wall Street.

The College for All Act of 2023 would massively change the higher education landscape in the U.S., taking a step toward Sanders’s long-standing goal of making public college free for all. It would make community college and public vocational schools tuition-free for all students, while making any public college and university free for students from single-parent households making less than $125,000 or couples making less than $250,000 — or, the vast majority of families in the U.S.

The bill would increase federal funding to make tuition free for most students at universities that serve non-white groups, such as Historically Black Colleges and Universities (HBCUs). It would also double the maximum award to Pell Grant recipients at public or nonprofit private colleges from $7,395 to $14,790.

If passed, the lawmakers say their bill would be the biggest expansion of access to higher education since 1965, when President Lyndon B. Johnson signed the Higher Education Act, a bill that would massively increase access to college in the ensuing decades. The proposal would not only increase college access, but also help to tackle the student debt crisis.

“Today, this country tells young people to get the best education they can, and then saddles them for decades with crushing student loan debt. To my mind, that does not make any sense whatsoever,” Sanders said. “In the 21st century, a free public education system that goes from kindergarten through high school is no longer good enough. The time is long overdue to make public colleges and universities tuition-free and debt-free for working families.”

Debt activists expressed support for the bill. “This is the only real solution to the student debt crisis: eliminate tuition and debt by fully funding public colleges and universities,” the Debt Collective wrote on Wednesday. “It’s time for your member of Congress to put up or shut up. Solve the root cause and eliminate tuition and debt.”

These initiatives would be paid for by several new taxes on Wall Street, found in a separate bill reintroduced by Sanders and Rep. Barbara Lee (D-California) on Wednesday. The Tax on Wall Street Speculation would enact a 0.5% tax on stock trades, a 0.1% tax on bonds and a 0.005% tax on trades on derivatives and other types of assets.

The tax would primarily affect the most frequent, and often the wealthiest, traders and would be less than a typical fee for pension management for working class investors, the lawmakers say. It would raise up to $220 billion in the first year of enactment, and over $2.4 trillion over a decade. The proposal has the support of dozens of progressive organizations as well as a large swath of economists.

“Let us never forget: Back in 2008, middle class taxpayers bailed out Wall Street speculators whose greed, recklessness and illegal behavior caused millions of Americans to lose their jobs, homes, life savings, and ability to send their kids to college,” said Sanders. “Now that giant financial institutions are back to making record-breaking profits while millions of Americans struggle to pay rent and feed their families, it is Wall Street’s turn to rebuild the middle class by paying a modest financial transactions tax.”

#us politics#news#truthout#sen. bernie sanders#progressives#progressivism#Democrats#senate health education labor and pensions committee#College for All Act of 2023#tax Wall Street#tax the rich#tax the 1%#tax the wealthy#college for all#student debt#student loan debt#tuition-free college#Historically Black Colleges and Universities#pell grants#Higher Education Act#Rep. Barbara Lee#rep. pramila jayapal#2023

466 notes

·

View notes

Text

Money in Astrology

Hey yall! I’m back today with a new post that’s going to discuss all things about your money! Yes, you can use astrology to help better your financials and what you can do to live a comfortable life that suits you!

To understand your money situation, you need 3 different charts to look at, Look at this like a cake, there’s 3 charts which means 3 layers:

First layer is your Natal Chart: this is the base on how to gain money. It’s the abilities you were born with and what you’ve learned from past lives

2nd layer is your Progessed chart: this is the 2nd layer to how to gain money. Progressed chart is the stage you are in life currently

3rd layer is your Solar Return Chart: this is the final layer to gain money. Solar return aka “your birthday” is the overall energy of that year for you.

The frosting of the cake is you putting this all together.

For one example: let’s say in your natal chart you have a Gemini 2h, Progressed has Cancer 2h and Solar has Aquarius 2h. Let’s put it all together.

So let’s say you’re a writer for a journalism company because Gemini rules over writing and Journalism. This is what you were naturally drawn to do to make a living. Now let’s say 10 years has passed by and now your 2h is in Cancer in your progressed chart. You’re still a writer because that’s still your natal placement, but now you want shift things up so instead of working for a company, you work from home (Cancer 2h)writing from a blog/website you created, something like Patreon. Instead of the regular 9-5, you make your own money but still doing what you original love which is writing. Now let’s say you want to know how your upcoming year financial will be. So you see you have an Aquarius 2h in your solar return chart which is perfect if you have an internet type of job that you’re trying to grow. Aquarius rules online and groups of people so your subscribers may grow that year which means more money.

Now planets in the 2h, and aspects if you have planets in the 2h influence this as well. Like if you have Aquarius moon in the 2h, you may feel alienated from you family during this time because you’re so focused on your blog. Your subscribers may start to feel more like family to you etc.

I know that was a long example but I want you all to really understand how to interpret this in your own lives and charts. I have Virgo 3h so I’m all about the details 🤪

Now that we got what kind of charts to look for and how to interpret them, let’s discuss what to actually look for in these charts!

1. The 2nd House + Planets in the 2h(if you have any), if not look for the 2h ruler + planetary degrees and house degrees (if your using Placidus house system)

-the 2h rules over physical money in general so this is is where you first look to get an idea to see what you can do to make it. This house is where you will start to build your wealth. 2h also rules over our values and assets. How you value and see money based on your upbringing can be seen here as well.

2. The House where Taurus rules in your charts

-Taurus rules the 2h naturally so wherever it rules in your charts, that’s an area where you can make money from as well.

3. Your Venus sign + degree + house placement + aspects to Venus

-Venus rules over money because it rules over Taurus. So even if you don’t know what to do by just looking at your 2h or Taurus house, look at your Venus placement

4. The 8th house. Use the same process for this house as you did the the 2h.

-the 8h is the opposite of the 2h. The 2h is physical money but the 8h is the power of money. It’s how you use your money in your life. 8h also rules other people money such as your partner. You can gain money through inheritance, you can have lots of debts too. 8h rules over loans as well.

5. Scorpio. Use the same process as Venus

-Scorpio is ruled by modern ruler Pluto and traditional ruler Mars. Pluto means “wealth” . I personally think it shows the power of wealth. Mars rules over action, Passionate and drive. You can make money and build wealth by using your Scorpio placements and house. What are you passionate about, what the thing that lights your soul on fire? That’s what you can make money from. Scorpio rules over alchemy, you can turn your passion into a goldmine. Money can change and end lives which is very Scorpio energy

6. 11th house

-not many people talk about the 11th house when it comes to money but it does play a role. It rules over “collected wealth” because it’s what you’ve been saving during your working career years. Using derivative houses (counting the houses) STARTING from the 10th house, it’s 2 spaces away from the 11h. So 10, 11=2 because we only counted 2 spaces over. The 2 represents the 2h.

If you’re confused about the derivative house method, go to my pinned post and scroll to learning tools and scroll down to derivative astrology post to get a better idea.

-The 11h also rules over connections and networking. You can literally make money based off of who you know and who knows you.

7. The house Aquarius sits

-like I said above, Aquarius rules over groups of people and networking. We are in a digital age now so making money off the internet is easy to do now compared to 20 years ago when technology was just coming up. Social media influencer is an actual career now that comes with lots privileges if you stick with it and meet the right people. Also look and see where Uranus and Saturn sits because aqua is ruled by both of these planets.

Thank you all for reading and if you need a birth chart, I’m open to help ya! Look at my pinned post for more details

#astrology#astrology community#knowledge#love astrology#astro observations#advanced astrology#birth chart#money#money in astrology

191 notes

·

View notes

Text

One thing I wonder about is: If you were designing a financial system from scratch, in 2024, would you come up with banking? That central traditional trick of banks — that they fund themselves with safe short-term demand deposits, and use depositors’ money to invest in risky longer-term loans, with all of the run risk and regulatory supervision and It’s a Wonderful Life-ness that that involves — would you recreate that if you were starting over?

Part of me feels like, if you started a new civilization and put smart but ahistorical tech people in charge of designing a financial system, it would never occur to them to recreate traditional banking. It is so messy and opaque and imprecise, using a shifting pile of demand deposits to fund long-term loans. Plenty of people — insurance companies, retirement savers — want to earn a return on their money and don’t need it anytime soon; their money can be locked up in long-term loans. The money that people keep in the bank just to pay rent and buy sandwiches doesn’t need to be pooled and invested in risky loans; it should just sit in the vault.

This idea — that bank deposits should just sit in the vault (or, realistically, in electronic money at the Federal Reserve), while risky loans should be funded by long-term investors who intend to take those risks — is sometimes called “narrow banking.” It has a long intellectual pedigree, it came back into vogue after the 2008 financial crisis, and it got attention again after last spring’s US regional banking crisis. All those crises! The traditional business of banking is necessarily crisis-prone; using risky long-term loans to back risk-free short-term demand deposits involves a fundamental mismatch, and every so often that flares up into a crisis.

And so, since 2008, but more visibly since last spring, banking really has become narrower. Private credit is the lending side of “narrow banking”: Private credit firms raise dedicated funds, with locked-up money, from investors who intend to invest in long-term loans to earn a return. And private credit is the hottest area of finance, making buyout loans and investment-grade corporate loans and funding consumer loans. And private credit is booming not just as a competitor to banks, but as a funding source for banks: Banks have the relationships and technology to make loans, but not the money, so they partner with private credit to fund the loans.

Meanwhile the deposit side of “narrow banking” is something like banks taking their customers’ money and parking it at the Federal Reserve. And in fact some money has shifted out of banks (which are not narrow) and into government money-market funds (which park the money in Fed repo or Treasury bills). Even within banks, there is less lending.

...

That’s narrow banking. I admit I have a certain emotional soft spot for traditional banking. There is something magical about how banking transmutes risky assets (loans) into risk-free liabilities (deposits). “A banking system is a superposition of fraud and genius that interposes itself between investors and entrepreneurs,” wrote Steve Randy Waldman in 2011; it allows society to use the money of risk-averse depositors to fund risky investments in growth. But it is possible that this magic no longer works: In a world of financial transparency and fast communications technology and flighty deposits, you can’t really expect to hide the risks of the banking system; you have to fund the loans with people who know they’re funding the loans.

I will say, though, that I have also written a lot about crypto over the last few years. Crypto really created a new financial system from scratch, and it started with a very strong philosophical bias against traditional banking. And then it really did recreate traditional banking! And also traditional banking crises: In 2022, it turned out that one of the main uses of crypto was to turn customer demand deposits (of crypto) into extremely risky loans (of crypto), which ended as badly as you’d have expected. “One possibility,” I wrote last year, “is that fractional reserve banking is deeply rooted in human nature.” If you started the financial system over, maybe banking would develop again. Even if actual banking is getting narrower now.

Matt Levine on narrow banking, we talk about this a lot as banks are so fundamental to how our entire civilisation currently functions and yet they're basically just hacks that lurch from crisis to crisis, more evolved than engineered

71 notes

·

View notes

Video

youtube

Is Crypto Really Going To Crash? (Yes)

Crypto is going to crash and could take your savings with it.

In June 2022, Bitcoin dropped over 30 percent to its lowest values since December 2020, and Ethereum, the second-most valuable cryptocurrency, fell about 35 percent. TerraUSD, a so-called “stablecoin,” also collapsed when its underlying cryptocurrency LUNA lost 97 percent of its value in just 24 hours, apparently destroying some investors’ life savings. The implosion helped trigger a crypto meltdown that erased $300 billion in value across the market.

As cryptocurrency prices plummeted, Celsius Network — an experimental cryptocurrency lender — announced it was freezing withdrawals “due to extreme market conditions.”

These crypto crashes and freezes have fueled worries that the complex crypto banking and lending system is on the brink of ruin.

But this crash shouldn’t surprise anyone familiar with the industry – or anyone who remembers the financial crashes of 1929 and 2008.

Let me explain.

In the murky world of crypto decentralized finance, known as DeFi, it’s hard to understand who provides money for loans, where the money flows, or how easy it is to trigger currency meltdowns.

There are no standards for issues of custody, risk management, or capital reserves. There are no transparency requirements. Investors often don’t know how their money is being handled. Deposits are not insured.

It’s a Ponzi scheme. Like all Ponzi schemes, getting rich depends on how many other investors follow you into it – until somebody’s left holding the worthless crypto coin.

Why isn’t this market regulated? Follow the money.

The crypto industry is pouring huge amounts into political campaigns. It has hired scores of former government officials and regulators to lobby on its behalf — including three former chairs of the Securities and Exchange Commission, three former chairs of the Commodity Futures Trading Commission, three former U.S. senators, and even former Treasury Secretary Larry Summers.

In the past, cryptocurrencies kept rising by attracting new investors and big Wall Street money, along with celebrity endorsements. But all Ponzi schemes topple eventually – just like the Wild West finances of the 1920s did.

Back then, Americans had been getting rich by speculating on shares of stock, as other investors followed them into these risky assets — pushing their values ever upwards. When the toppling occurred in 1929, it plunged the nation and the world into the Great Depression.

That crash resulted in the Glass-Steagall Act, signed into law by Franklin D. Roosevelt in 1933. Glass-Steagall separated commercial banking from investment banking, putting an end to the giant Ponzi scheme that had overtaken the American economy and led to the Great Crash of 1929.

It took a full generation to forget that crash and allow the forces that caused it to repeat their havoc.

By the mid-1980s, as the stock market soared, speculators noticed they could make even more money if they gambled with other people’s money, as speculators did in the 1920s. They pushed Congress to deregulate Wall Street, arguing that the United States financial sector would otherwise lose its competitive standing internationally.

The final blow was in 1999, when the Clinton administration succumbed to intensive lobbying and ditched what remained of Glass-Steagall. With its repeal, American finance once again became a betting parlor.

Inevitably, Wall Street suffered another near-death experience when its Ponzi schemes began toppling in 2008, just as they had in 1929. While the U.S. government bailed out the biggest banks and financial institutions, millions of Americans lost their jobs, their savings, and their homes – but only a single banking executive went to jail. In the wake of the 2008 financial crisis, a new but watered-down version of Glass-Steagall was enacted — the Dodd-Frank Act.

Which brings us — nearly a century after Glass-Steagall — to today’s crypto crash.

If we should have learned anything from the crashes of 1929 and 2008, it’s that regulation of financial markets is essential. Otherwise they turn into Ponzi schemes — leaving small investors with nothing and endangering the entire economy.

It’s time for the Biden administration and Congress to end the crypto Ponzi scheme.

In the meantime, share this video so your friends and family don’t fall for it.

2K notes

·

View notes

Text

Watcher's Expenses

I didn't major in accounting: I took three classes and it grinded my brain to a fine powder. However, after graduating with a business admin degree, being a former eager fan of their videos, and from a cursory glance over their socials, there's a lot to consider in their spending behavior that really could start racking up costs. Some of these things we've already noticed, but there are other things I'd like to highlight, and I'll try to break it down into the different categories of accounting expenses (if I get something wrong, let me know. I was more concentrated in marketing 🤷♀️). I'm not going to hypothesize numbers either, as that would take out more time than I'm willing to afford-- you can assume how much everything costs. Anyways, here's my attempt at being a layman forensic accountant:

Note: All of this is assuming they're operating above board and not engaging in any illegal practices such as money laundering, tax evasion, not paying rent, etc.

Operating Expenses

Payroll: 25+ staff salaries and insurance

Overhead Expenses

CEO/founder salaries

Office space leasing or rent (In L.A, one of the most expensive cities in the US)

Utilities (water, electricity, heating, sanitation, etc.)

Insurance

Advertising Costs

Telephone & Internet service

Cloud Storage or mainframe

Office equipment (furniture, computers, printers, etc.)

Office supplies (paper, pens, printer ink, etc.)

Marketing costs (Social media marketing on Instagram, Youtube, SEO for search engines, Twitter, etc. Designing merchandise and posters, art, etc. )

Human Resources (not sure how equipped they are)

Accounting fees

Property taxes

Legal fees

Licensing fees

Website maintenance (For Watchertv.com, Watcherstuff.com, & Watcherentertainment.com)

Expenses regarding merchandising (whoever they contract or outsource for that)

Inventory costs

Potentially maintenance of company vehicles

Subsequent gas mileage for road trips

Depreciation (pertains to tangible assets like buildings and equipment)

Amortization (intangible assets such as patents and trademarks)

Overhead Travel and Entertainment Costs (I think one of the biggest culprits, evident in their videos and posts)

The travel expenses (flights, train trips, rental cars, etc. For main team and scouts)

Hotel expenses for 7-8 people at least, or potentially more

Breakfasts, lunches and dinners with the crew (whether that's fully on their dime or not, I don't know; Ryan stated they like to cover that for the most part)

Recreational activities (vacation destinations, amusement parks, sporting activities etc.)

The location fees

Extraneous Overhead costs (not sure exactly where these fall under, but another culprit, evident in videos and posts)

Paying for guest appearances

Expensive filming & recording equipment (Cameras, sound equipment, editing software subscriptions, etc.)

The overelaborate sets for Ghost files, Mystery Files, Puppet History, Podcasts etc. (Set dressing: Vintage memorabilia, antiquated tech, vintage furniture, props, etc.)

Kitchen & Cooking supplies/equipment

Office food supply; expensive food and drink purchases for videos

Novelty items or miscellaneous purchases (ex. Ghost hunting equipment, outfits, toys, etc.)

Non-Operating Expenses

These are those expenses that cannot be linked back to operating revenue. One of the most common examples of non-operating expenses is interest expense. This is because while interest is the cost of borrowing money from a creditor or a bank, they are not generating any operating income. This makes interest payments a part of non-operating expenses.

Financial Expenses

Potential loan payments, borrowing from creditors or lenders, bank loans, etc.

Variable Expenses

Hiring a large amount of freelancers, overtime expenditure, commissions, etc.

PR consultations (Not sure if they had this before the scandal)

Extraordinary Expenses

Expenses incurred outside your company’s regular business activities and during a large one-time event or transactions. For example, selling land, disposal of a significant asset, laying off of your employees, unexpected machine repairing or replacement, etc.

Accrued Expenses

When your business has incurred an expense but not yet paid for it.

------------------------------------------------------------------------------------------------------------------------

(If there's anything else I'm missing, please feel free to add or correct things)

To a novice or a young entrepreneur, this can be very intimidating if you don't have the education or the support to manage it properly. I know it intimidates the hell out of me and I'm still having to fill in the gaps (again, if I've mislabeled or gotten anything wrong here, please let me know). For the artistic or creative entrepreneur, it can be even harder to reconcile the extent of your creative passions with your ability to operate and scale your business at a sustainable rate. That can lead to irresponsible, selfish, and impulsive decisions that could irreparably harm your brand, which is a whole other beast of its own.

My guess at this point is that their overhead and operation expenses are woefully mismanaged; they've made way too many extraneous purchases, and that they had too much confidence in their audience of formerly 2.93 million to make up for the expenses they failed to cover.

It almost seems as if their internal logic was, "If we make more money, we can keep living the expensive lifestyle that we want and make whatever we want without anyone telling us we can't, and we want to do it NOW, sooner rather than later because we don't want wait and compromise our vision." But as you can see, the reality of fulfilling those ambitions is already compromised by the responsibility of running a business.