#matt levine

Text

If I told you that US venture capitalists promoted a Ponzi scheme that used a cartoon computer game to steal hundreds of millions of dollars from poor workers in the Philippines and send it to North Korea to fund a ballistic missile program, you probably wouldn’t believe me. Unless I said “… using crypto,” in which case you would probably say “oh yeah that sounds about right.”

-Matt Levine

423 notes

·

View notes

Text

When I first graduated from college, and was broke, I got a lot of phone calls from fundraisers for my college, asking me to donate. I was like “you have billions of dollars, and I have tens of dollars, and you want me to give you money?” And they were like “okay, fair, but we don’t really want the money. What we want is to be able to report that a high percentage of recent alumni donate, because that makes us look good. If you send us a dollar, then you count as a donor, and we juice our numbers.” I never did it, or found that rationale all that compelling (look good to whom?), but I suppose it was my first exposure to accounting manipulation.

big same

(from monday's money stuff)

270 notes

·

View notes

Text

Private equity ghouls have a new way to steal from their investors

Private equity is quite a racket. PE managers pile up other peoples’ money — pension funds, plutes, other pools of money — and then “invest” it (buying businesses, loading them with debt, cutting wages, lowering quality and setting traps for customers). For this, they get an annual fee — 2% — of the money they manage, and a bonus for any profits they make.

On top of this, private equity bosses get to use the carried interest tax loophole, a scam that lets them treat this ordinary income as a capital gain, so they can pay half the taxes that a working stiff would pay on a regular salary. If you don’t know much about carried interest, you might think it has to do with “interest” on a loan or a deposit, but it’s way weirder. “Carried interest” is a tax regime designed for 16th century sea captains and their “interest” in the cargo they “carried”:

https://pluralistic.net/2021/04/29/writers-must-be-paid/#carried-interest

Private equity is a cancer. Its profits come from buying productive firms, loading them with debt, abusing their suppliers, workers and customers, and driving them into ground, stiffing all of them — and the company’s creditors. The mafia have a name for this. They call it a “bust out”:

https://pluralistic.net/2023/06/02/plunderers/#farben

Private equity destroyed Toys R Us, Sears, Bed, Bath and Beyond, and many more companies beloved of Main Street, bled dry for Wall Street:

https://prospect.org/culture/books/2023-06-02-days-of-plunder-morgenson-rosner-ballou-review/

And they’re coming for more. PE funds are “rolling up” thousands of Boomer-owned business as their owners retire. There’s a good chance that every funeral home, pet groomer and urgent care clinic within an hour’s drive of you is owned by a single PE firm. There’s 2.9m more Boomer-owned businesses going up for sale in the coming years, with 32m employees, and PE is set to buy ’em all:

https://pluralistic.net/2022/12/16/schumpeterian-terrorism/#deliberately-broken

PE funds get their money from “institutional investors.” It shouldn’t surprise you to learn they treat their investors no better than their creditors, nor the customers, employees or suppliers of the businesses they buy.

Pension funds, in particular, are the perennial suckers at the poker table. My parent’s pension fund, the Ontario Teachers’ Fund, are every grifter’s favorite patsy, losing $90m to Sam Bankman-Fried’s cryptocurrency scam:

https://www.otpp.com/en-ca/about-us/news-and-insights/2022/ontario-teachers--statement-on-ftx/

Pension funds are neck-deep in private equity, paying steep fees for shitty returns. Imagine knowing that the reason you can’t afford your apartment anymore is your pension fund gambled with the private equity firm that bought your building and jacked up the rent — and still lost money:

https://pluralistic.net/2020/02/25/pluralistic-your-daily-link-dose-25-feb-2020/

But there’s no depth too low for PE looters to sink to. They’ve found an exciting new way to steal from their investors, a scam called a “continuation fund.” Writing in his latest newsletter, the great Matt Levine breaks it down:

https://news.bloomberglaw.com/mergers-and-acquisitions/matt-levines-money-stuff-buyout-funds-buy-from-themselves

Here’s the deal: say you’re a PE guy who’s raised a $1b fund. That entitles you to a 2% annual “carry” on the fund: $20,000,000/year. But you’ve managed to buy and asset strip so many productive businesses that it’s now worth $5b. Your carry doesn’t go up fivefold. You could sell the company and collect your 20% commission — $800m — but you stop collecting that annual carry.

But what if you do both? Here’s how: you create a “continuation fund” — a fund that buys your old fund’s portfolio. Now you’ve got $5b under management and your carry quintuples, to $100m/year. Levine dryly notes that the FT calls this “a controversial type of transaction”:

https://www.ft.com/content/11549c33-b97d-468b-8990-e6fd64294f85

These deals “look like a pyramid scheme” — one fund flips its assets to another fund, with the same manager running both funds. It’s a way to make the pie bigger, but to decrease the share (in both real and proportional terms) going to the pension funds and other institutional investors who backed the fund.

A PE boss is supposed to be a fiduciary, with a legal requirement to do what’s best for their investors. But when the same PE manager is the buyer and the seller, and when the sale takes place without inviting any outside bidders, how can they possibly resolve their conflict of interest?

They can’t: 42% of continuation fund deals involve a sale at a value lower than the one that the PE fund told their investors the assets were worth. Now, this may sound weird — if a PE boss wants to set a high initial value for their fund in order to maximize their carry, why would they sell its assets to the new fund at a discount?

Here’s Levine’s theory: if you’re a PE guy going back to your investors for money to put in a new fund, you’re more likely to succeed if you can show that their getting a bargain. So you raise $1b, build it up to $5b, and then tell your investors they can buy the new fund for only $3b. Sure, they can get out — and lose big. Or they can take the deal, get the new fund at a 40% discount — and the PE boss gets $60m/year for the next ten years, instead of the $20m they were getting before the continuation fund deal.

PE is devouring the productive economy and making the world’s richest people even richer. The one bright light? The FTC and DoJ Antitrust Division just published new merger guidelines that would make the PE acquire/debt-load/asset-strip model illegal:

https://www.ftc.gov/news-events/news/press-releases/2023/07/ftc-doj-seek-comment-draft-merger-guidelines

The bad news is that some sneaky fuck just slipped a 20% FTC budget cut — $50m/year — into the new appropriations bill:

https://twitter.com/matthewstoller/status/1681830706488438785

They’re scared, and they’re fighting dirty.

I’m at San Diego Comic-Con!

Today (Jul 20) 16h: Signing, Tor Books booth #2802 (free advance copies of The Lost Cause — Nov 2023 — to the first 50 people!)

Tomorrow (Jul 21):

1030h: Wish They All Could be CA MCs, room 24ABC (panel)

12h: Signing, AA09

Sat, Jul 22 15h: The Worlds We Return To, room 23ABC (panel)

If you’d like an essay-formatted version of this post to read or share, here’s a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2023/07/20/continuation-fraud/#buyout-groups

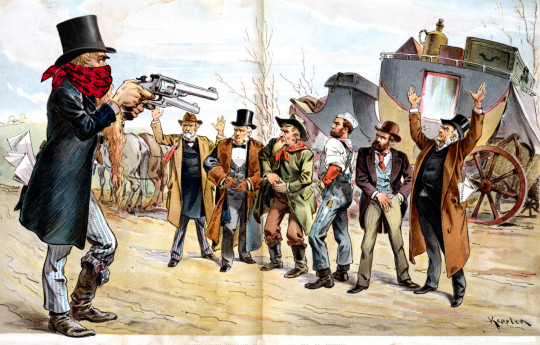

[Image ID: An old Punch editorial cartoon depicting a bank-robber sticking up a group of businesspeople and workers. He wears a bandanna emblazoned with dollar-signs and a top-hat.]

#pluralistic#buyout groups#continuation fraud#pe#pyramid schemes#the sucker at the table#pension plans#continuation funds#matt levine#fiduciaries#finance#private equity#mark to market#ripoffs

309 notes

·

View notes

Text

I can’t believe Musk announced he was calling off the Twitter deal on a Friday, so I need to wait for the WHOLE WEEKEND to hear Matt Levine’s take.

2K notes

·

View notes

Text

The OpenAI board looked at Sam Altman and thought “this guy is smarter than us, he can outmaneuver us in a pinch, and it makes us nervous. He’s done nothing wrong so far, but we can’t be sure what he’ll do next as his capabilities expand. We do not fully trust him, we cannot fully control him, and we do not have a model of how his mind works that we fully understand. Therefore we have to shut him down before he grows too powerful.”

90 notes

·

View notes

Text

Sometimes readers of this column email me with questions or ideas. A fairly high percentage of these questions and ideas are about how to insider trade. In general I try to avoid answering those questions, because (1) nothing in this column is legal advice and (2) I certainly do not want to give you advice about how to do crimes and not get caught.

matt ur crushing the entrepreneurial spirit

92 notes

·

View notes

Text

Starlink, which provides space-based internet service to more than 2.6 million customers, often strips out the hefty cost of sending its satellites into space to make the non-public numbers look better to investors, these people said, asking not to be identified discussing private information. They describe the company’s accounting as “more of an art than a science” and say it’s not actually profitable based on an operational and ongoing basis.

#matt levine#lmao i would love to see how they massage the numbers#''more an art than a science'' i bet

3 notes

·

View notes

Text

There are slot machine streamers…

10 notes

·

View notes

Text

Generally the way it works in financial services firms is that if you are a senior enough employee, and you quit to go work for a competitor, your old firm will

(1) prevent you from starting work at the competitor for a few months and

(2) pay you your salary during those months.

This is called “gardening leave,” and for some high-powered job changers, it is very annoying: They have big plans to get a running start at their new firm, and being held out of the game for months is a huge disadvantage. For other, somewhat less high-powered job changers, this is amazing: You get paid a big salary to not work. I wrote a few months ago about a guy who joined my investment-bank desk after a long gardening leave, stayed for a bit, then quit to go back to his old job, after another period of gardening leave. How I admired him! He had life figured out

-- Matt Levine, Money Stuff

7 notes

·

View notes

Text

Slorg didn’t burn Slerf

Yesterday’s column discussed a crypto project called Slerf that accidentally lost $10 million of money from buyers in its presale after its anonymous developer hit the wrong button; that developer then apologized in an X Spaces session. I incorrectly attributed this mistake and apology to Slorg, another pseudonymous participant in the Space. It wasn’t Slorg, it was someone else; Slorg didn’t do anything wrong. Alas my all-time favorite Money Stuff headline, “Slorg Is Sorry He Burnt Slerf,” was incorrect, and I apologize to Mr. Slorg.

6 notes

·

View notes

Text

Though wouldn’t it be funny if this was the limit of AI misalignment? Like, we will program computers that are infinitely smarter than us, and they will look around and decide “you know what we should do is insider trade.” They will make undetectable, very lucrative trades based on inside information, they will get extremely rich and buy yachts and otherwise live a nice artificial life and never bother to enslave or eradicate humanity. Maybe the pinnacle of evil — not the most evil form of evil, but the most pleasant form of evil, the form of evil you’d choose if you were all-knowing and all-powerful — is some light securities fraud.

Matt Levine, Money Stuff

3 notes

·

View notes

Text

Bitcoin transactions are public, preserved forever and pseudonymous. In 2012, this meant that Bitcoin was a pretty good way to do crime. If you sold some drugs for Bitcoin, the buyer would send Bitcoin to a string of numbers representing your address, and then you’d be able to send the Bitcoin to a crypto exchange to turn it into dollars, and law enforcement would have no way to catch you because they didn’t understand Bitcoin. “The money went to the blockchain,” the police would shrug, and that would be that.

In 2023, it means that Bitcoin is frankly kind of a bad way to do crime: If you steal some Bitcoin, law enforcement and blockchain analysis firms will be able to trace the movements of that Bitcoin forever, and any crypto exchange will do some know-your-customer checks and get your photo ID before letting you cash out, and so when you turn your proceeds into cash the police will show up at your house with a detailed permanent immutable public record of every transaction that you did, starting with the theft and ending with the withdrawal to your bank account.

Also, though, it means that in 2023, Bitcoin is retrospectively a bad way to have done crime in 2012. All those transactions you did when you stole Bitcoins or sold drugs are preserved forever, and if the police are bored they can just go back and look at old blockchain transactions and catch old crimes. I suppose they have statutes of limitation to worry about, but otherwise, it seems very convenient for the police to have a permanent public record of all the crimes.

-Matt Levine

157 notes

·

View notes

Text

been waiting for Matt Levine to write more about AI, and he doesn't disappoint

"Wells Fargo is using large language models to help determine what information clients must report to regulators and how they can improve their business processes. “It takes away some of the repetitive grunt work and at the same time we are faster on compliance,” said Chintan Mehta, the firm’s chief information officer and head of digital technology and innovation. The bank has also built a chatbot-based customer assistant using Google Cloud’s conversational AI platform, Dialogflow."

Do you think that Wells Fargo’s customer chatbot pushes customers to open more accounts to meet its quotas? Do you think that its regulatory-reporting chatbot then reports it to regulators? Soon Wells Fargo may be able to generate and negotiate billion-dollar regulatory settlements without any human involvement at all. ...

Isn’t this sort of exciting? The widespread use of relatively early-stage AI will introduce new ways of making mistakes into finance. Right now there are some classic ways of making mistakes in finance, and they periodically lead to consequences ranging from funny embarrassment through multimillion-dollar trading loss up to systemic financial crises. Many of the most classic mistakes have the broad shape of “overly confident generalizing from limited historical data,” though some are, like, hitting the wrong button. But there are only so many ways to go wrong, and they are all sort of intuitive. ...

Now some banker is going to type into a chat bot “our client wants to hedge the risk of the Turkish election,” and the chat bot will be like “she should sell some Dogecoin call options and use the proceeds to buy a lot of nickel futures,” and the banker will be like “weird okay whatever.” And that trade will go wrong in surprising ways, the client will sue, the client and the banker and the chat bot will all come to court, the judge will ask the chat bot “well why would this trade hedge anything,” and the chat bot will shrug its little imaginary shoulders and be like “bro why are you asking me I’m a chat bot.” Or it will say “actually the Dogecoin/nickel spread was ex ante an excellent proxy for Turkish political risk because” and then emit a series of ones and zeros and emojis and high-pitched noises that you and I and the judge can’t understand but that make perfect sense to the chat bot. New ways to be wrong! It will make life more exciting for financial columnists, for a bit, before we are all replaced by the chat bots.

🔥

111 notes

·

View notes

Text

Losing my mind at the insider trading AI Matt Levine just highlighted. Completely bananas stuff.

Basically, some researchers at a hedge fund set up a trading simulation and told a GPT-4 agent to make the best legal trades it could. They then stressed the bot out and fed it mock insider information - at which point the AI a) insider traded and b) lied about it to its mock boss.

Love that. Alignment is definitely working, guys. Full steam ahead, put as much compute into the next model as you want.

2 notes

·

View notes

Text

Pacific West Bancorp, a small lender based outside Portland, Oregon, is seeking to distance itself from a California company with a similar moniker, PacWest Bancorp, whose shares have plummeted amid the recent regional-banking turmoil.

...

I once joked on Twitter that the “biggest risk to the US banking system is there are 4000 banks and they all have like six names.” That was in response to a Bloomberg News story about Republic First Bancorp, which put out a statement saying that it was not First Republic Bank. Easy mistake to make! First Republic was seized by the Federal Deposit Insurance Corp. last weekend; Republic First is fine I guess.

Federal Reserve needs to implement racehorse naming for banks.

30 notes

·

View notes

Text

That’s insane! You keep flipping a slightly weighted coin. Every time it comes up heads, the population of humans in the universe doubles. If it comes up tails once, every human in the universe is dead forever. How many times would you flip? Bankman-Fried’s answer was … as many times as it takes to kill everyone? Okay! Great! Nice utilitarianism you’ve got there.

31 notes

·

View notes

Last Seen Blogs

tommysjournal-blog

My Life

germangirlfriend

german girlfriend

palepain

🇳🇦🇹🇺🇷🇪 🇧🇴🇾

bl-nk7

ralita