#bank run

Photo

#bank run#build back better#bt news#congress#bank bailouts#student debt#student loans#student loan crisis#cancel student loans#cancel student debt#student debt forgiveness#student debt relief#paid family leave#infrastructure#universal childcare#instagram

105 notes

·

View notes

Text

Angry depositors gathered in front of the Clarke Brothers Bank, an 80-year old private institution at 154 Nassau St., which closed as bankrupt, ca. 1929. Unprecedented withdrawals caused the crisis, and the payment of 100 cents on the dollar was promised to the skeptical depositors.

Photo: Bettmann Archive/Getty Images/Fine Art America

#vintage New York#1920s#bank run#bank closure#bankruptcy#bank failure#Great Depression#Great Depression causes#bank crisis#banking crisis#vintage NYC

22 notes

·

View notes

Link

6 Lessons YOU Can Learn from the Silicon Valley Bank Crash

When news of the Silicon Valley Bank crash broke, I sighed deeply. Because sighing deeply is the age-appropriate version of a toddler pounding their fists on the floor screaming “I don’ wanna, I don’ wanna, I DON’ WANNA!” That’s always how I feel when I have to understand some complicated new brouhaha caused by oligarchs’ greed, when all I truly need in this life is more naptime.

Guys, don’t worry. Because I am a grown-up woman with finely tuned coping mechanisms, I worked through my tantrum and I did it! I understand what the hell happened to Silicon Valley Bank.

Paragon of intellectual generosity that I am, I’m going to explain it back to you.

If you want an in-depth, technical breakdown, this ain’t gonna be it. I’m going to focus on what this means for us plebs. That means skipping all the boring parts, creatively employing childish metaphors, recklessly speculating about its impact on the future of the economy, and oversimplifying absolutely everything.

Complex, dense financial topics explained by babies, for babies. That’s the Bitches Get Riches brand promise!

Keep reading

#svb#silicon valley bank#silicon valley bank crash#bank run#bank collapse#economics#economy#money#bitches get riches

42 notes

·

View notes

Text

the call was coming from inside the fucking house

43 notes

·

View notes

Text

The "small nonprofit school" saved in the SVB bailout charges more than Harvard

There are no libertarians in a bank run. No sooner had venture capitalists whipped each other into a terrified Twitter frenzy at the imminent collapse of Silicon Valley Bank — a collapse caused by that selfsame frenzy — than the Ayn Rand-poisoned elite of Sand Hill Road started begging for Uncle Sucker to open the sluicegates:

https://twitter.com/EricNewcomer/status/1634300928621793283

If you’d like an essay-formatted version of this post to read or share, here’s a link to it on pluralistic.net, my surveillance-free, ad-free, tracker-free blog:

https://pluralistic.net/2023/03/23/small-nonprofit-school/#north-country-school

Now, on the one hand, it’s easy to dismiss these guys as very, very, very stupid. After all, they played a game of prisoner’s dilemma in which they were allowed to talk to each other as much as they wanted — and they still sold each other out:

https://newsletter.mollywhite.net/p/the-venture-capitalists-dilemma

But they still have the commonsense to realize that an America where $10k in student debt cancellation, school lunches for hungry children, and library budgets are out of reach, handing billions to a bank rescue a balance sheet overwhelmingly made up the investments of “high net worth” investors wouldn’t be popular.

After all, these guys have been crying about incipient guillotinism for years:

https://www.bloomberg.com/news/articles/2015-06-08/billionaire-cartier-owner-sees-wealth-gap-fueling-social-unrest

Sure, they don’t compare small rises in the top marginal tax-rate to Kristallnacht anymore:

https://www.npr.org/sections/alltechconsidered/2014/01/26/266685819/billionaire-compares-outrage-over-rich-in-s-f-to-kristallnacht

But they are locked and loaded for The Event, feathering elaborate subterranean, antipodean nests in the most luxurious bunkers New Zealand has to offer, against the day that the poors come to eat them:

https://www.cnn.com/2020/07/15/business/bunkers-new-zealand-intl-hnk/index.html

So amid the clamor for socialism-for-the-rich, these billionaires went on the hunt for average joes who could serve as the face of the bailout. Like the “Ohio mom with 4 kids and a husband who works in manufacturing, who owns a small business:”

https://www.businessinsider.com/mother-small-startup-ceo-fall-svb-not-1-problem-2023-3

She’s ex-McKinsey and raised $4m in VC for a $600/month life-planning app; her husband, another McKinsey alum, is a senior manager at a steel company (that is, he “works in manufacturing”).

Clearly, the ex-libertarian 0.01 percenters begging for relief needed to find someone else. Enter David Sacks, a billionaire Paypal mafiosi who waded into the debate with screenshots of an email from a “small, non-profit school” that would miss payroll if the bailout was not forthcoming:

https://twitter.com/DavidSacks/status/1636054055121453057

Sacks held this up as evidence that SVB’s depositors were “more diversified than the media narrative has allowed.” Sacks went on to claim that the bailout saved “innocent bystanders” like “teachers” from being “laid off.”

What is this small, nonprofit school? Writing in The American Prospect, Luke Goldstein sleuths it out: the “small, nonprofit school” is North Country School, an upstate New York boarding school where tuition runs $62k/year — more than Harvard or Yale:

https://prospect.org/economy/2023-03-22-david-sacks-bank-bailout/

North Country sounds like a great place to get an education. It’s got its own private ski-slope. The local city raised a $7m municipal bond on its behalf. There’s a rock-climbing range and horseback riding. The school emphasizes unstructured, outdoor education, with “farming, wilderness trips…even maple sugaring”:

https://northcountryschool.org/

Let’s be honest, this is the kind of education a lot of us dream of our kids having. No wonder that the alumna include numerous Rockefellers, and a scion of the Aga Khan family — claimed lineal descendants of the Prophet Muhammad.

As illustrious as the student body is, the trustees are even more gilt-edged. There’s a former Jpmorgan managing director, a former Google exec, Austrian nobility, the Welch’s grape heir and even JD Salinger’s kid. The chair ran a booze delivery company that sold to Uber. Together, they manage $30m in assets and raise $3m/year in donations, on top of $9m/year in revenues.

As Goldstein points out, it might be a lot to ask of the median small, nonprofit school trustee to investigate the soundness of the school’s bank. But these aren’t the median trustees of the median school. They’re raising millions from Vanguard and Fidelity and the JM Kaplan Fund. Perhaps it’s not asking too much that high-flying financiers craft a risk management plan for their deposits — or, you know, just have the nous not to stash all their money in a single bank account, diversifying their risk the way that any financial planner would tell them to do.

According to Sacks, if the FDIC had frozen SVB withdrawals, or imposed a 10 percent haircut on depositors with more than $250k in the bank, the “modestly paid workers who tend not to have a lot of savings to fall back on” who worked at the school would have been out in the cold. But with donors on tap who give $50,000 at a pop, it seems likely that the trustees could have tapped someone for a bridge loan.

It’s doubtless true that there are low-waged, precarious workers who would have been out in the cold if the FDIC hadn’t stepped in, but the wealthy “investors” who clamored for the bailout spent the last several years consistently, brutally, loudly calling for an end to covid relief, no student debt cancellation, and cuts to public services. The idea that they were worried about saving the janitors and receptionists of Silicon Valley strains credulity:

https://pluralistic.net/2023/03/18/2-billion-here-2-billion-there/#socialism-for-the-rich

You can’t be on record calling for tech billionaires to “Sharpen your blades boys 🔪” ahead of mass layoffs and also claim to be a champion of the middle-class:

https://pluralistic.net/2023/03/21/tech-workers/#sharpen-your-blades-boys

As Goldstein writes, “David Sacks couldn’t find a mom-and-pop institution to justify his cockeyed version of reality without turning to a VC colleague’s ultra-rich boarding school.” There might be mom-and-pop institutions on the SVB balance-sheet, but David Sacks evidently doesn’t know any of them.

New York State is a good place to be a Silicon Valley banker. For one thing, the Southern District of New York is an exceptionally nice place to be a bankrupt billionaire, which is why SVB’s investors now claim that their headquarters are at 387 Park Ave, 2,951 miles from the Santa Clara HQ the company listed on all its filings:

https://pluralistic.net/2023/03/18/2-billion-here-2-billion-there/#socialism-for-the-rich

In New York, elite boarding schools get federal rescues, so long as they can claim some nexus with SVB. But, as Goldstein writes, NY city and state schools are in outright financial crisis, with no aid in sight. The State University of New York system is drowning in debt. NYC schools are about to bring down massive layoffs, having lost $469m out of their budgets:

https://comptroller.nyc.gov/newsroom/testimony-of-new-york-city-comptroller-brad-lander-to-the-new-york-city-council-committee-on-education-on-resolution-283-2022-to-immediately-reverse-doe-reductions-to-school-budgets-for-fy-2023/

The FDIC stepped in to rescue SVB, claiming that it wouldn’t cost the public anything — instead, the money would come from increases in the entire bank system’s insurance premiums. But as Adam Levitin writes for Credit Slips, banks “will pass those premiums through to customers because the market for banking services is less competitive than the market for capital…higher costs for increased insurance premiums are likely to flow to the least price-sensitive and most ‘sticky’ customers: less wealthy individuals”

“So average Joes are going to be facing things like higher account fees or lower APYs, without gaining any benefit. Instead, the benefit of removing the cap would flow entirely to wealthy individuals and businesses. This is one massive, regressive cross-subsidy.”

https://www.creditslips.org/creditslips/2023/03/the-regressive-cross-subsidy-of-uncapping-deposit-insurance.html

Nothing about this bailout intrinsically protects anyone’s job. Yes, if the companies that banked with SVB went under, they’d have fired everyone. But tech companies are firing everyone anyway, 280,000 and counting, in profitable companies where they do stock-buybacks big enough to pay every worker’s salary for the next quarter-century:

https://pluralistic.net/2023/03/21/tech-workers/#sharpen-your-blades-boys

I’m kickstarting the audiobook for my next novel, a post-cyberpunk anti-finance finance thriller about Silicon Valley scams called Red Team Blues. Amazon’s Audible refuses to carry my audiobooks because they’re DRM free, but crowdfunding makes them possible

[Image ID: A vast castle surrounded by a stately brick wall bearing an ornate gilt-framed sign reading 'Small, non-profit school,' in gothic lettering. Atop the wall is a caricature of Humpty Dumpty, looking distressed. He has a SVB logo over his chest. He is being restrained by tiny, top-hatted bankers.]

#pluralistic#bank run#venture capitalists dilemma#prisoners dilemma#north country school#david sacks#svb#silicon valley bank#bailouts

43 notes

·

View notes

Text

#Stocks drop on #bank fears

View On WordPress

#America#bank run#banking#banks#Credit Suisse#crypto#cryptocurrency#europe#meme#memes#money#news#stock market#stocks#tech#technology#united states

45 notes

·

View notes

Text

7 notes

·

View notes

Text

“Big banks including JPMorgan Chase & Co. and PNC Financial Services Group Inc. are vying to buy First Republic Bank in a deal that would follow a government seizure of the troubled lender, according to people familiar with the matter.

A seizure and sale of First Republic by the Federal Deposit Insurance Corp. could come as soon as this weekend, the people said.

The San Francisco-based bank has teetered for weeks following the March 10 failure of fellow Bay Area lender Silicon Valley Bank. The SVB meltdown spurred panicky First Republic customers to pull around $100 billion in deposits in a matter of days.

The stock has lost some 97% of its value since.

(…)

A seizure and sale of First Republic would cap the astonishing collapse of a lender that was, until recently, the envy of finance. With some $233 billion in assets at the end of the first quarter, it would be the second-largest bank to fail in U.S. history.”

“The Federal Deposit Insurance Corp. has asked banks including JPMorgan Chase & Co., PNC Financial Services Group Inc., US Bancorp and Bank of America Corp. to submit final bids for First Republic Bank by Sunday after gauging initial interest earlier in the week, according to people with knowledge of the matter.

The regulator reached out to banks late Thursday seeking indications of interest, including a proposed price and an estimated cost to the agency’s deposit insurance fund. Based on those submissions Friday, the regulator invited some firms to the next step in the bidding process, the people said, asking not to be named discussing the confidential talks.

(…)

JPMorgan is among a small number of giant banks that have already amassed more than 10% of nationwide deposits, making the firm ineligible under US regulations to acquire another deposit-taking institution. Authorities would have to make an exception to allow the country’s largest bank to get even bigger.”

5 notes

·

View notes

Text

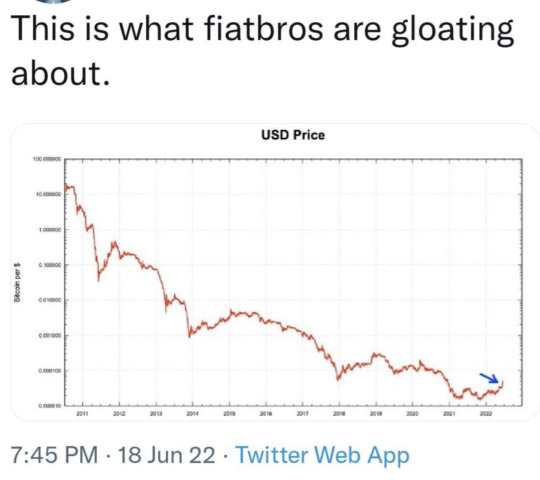

hey.

fiatbro

would you like a doge bag?

#crypto#cryptocurreny trading#recession#bitcoin#crypto exchange#fake money#scam#alt text#millennials#sec commissioner#bankruptcy#bank run#capitalist hell#market capitalisation#capitalism#colonizers#climate catastrophe#oligarchs#elon musk#dogecoin

20 notes

·

View notes

Link

It’s not obvious to me why venture capitalists should be so in control of what tech gets funded, who designs it, how it gets developed, why it gets deployed, and where the returns go. If it is simply a question of capital, we can and should explore alternatives to the privately run VC system prioritizing tech that degrades and commodifies more of our life, gambles on these developments with other people’s money, and in the blink of an eye causes regular panics that threaten to upend life for countless people. If it is a question of talent, we can and should recognize that these people are not any smarter or more talented than us—they just have more capital to throw at problems, better connections to ensure things work out their way, and less shame preventing them from pursuing what they want. If it is a question of politics, then we should ask whether a system that subsidizes a bunch of well-connected, wealthy libertarians as they enrich one another with lottery tickets is truly the only way we can and should develop technology. I hope not.

#silicon-valley#finance#article#bank run#vulture capitalism#VC#tech bros#technology#economy#economics#Silicon Valley Bank

10 notes

·

View notes

Text

50% Potential Loss to the Great Triumvirate: Stocks, Bonds, and Real Estate

Proverbs 22:7 The rich rules over the poor, and the borrower is the slave of the lender.

Proverbs 22:16 Whoever oppresses the poor to increase his own wealth, or gives to the rich, will only come to poverty.

Michael Douville took the time to talk with President of Pento Portfolio Strategies, Michael Pento.

For those who are interested in a deep discussion about bonds, debt, and lending. How…

View On WordPress

#bank run#bonds#cash#Debt#FDIC#GDP#Global Economy#gross domestic product#liquidity#money supply#real estate#recession#risk#stock market#stocks

2 notes

·

View notes

Photo

A bank run during the 1930s.

3 notes

·

View notes

Last Seen Blogs

good-beanswrites

Headcanon time

stardollacademy-blog

Academy

coolarcadecoffee

Untitled

t-annhauser

{ Tannhäuser }

xgoldennovex

hi-ho come roll me over