#tpd payout

Text

When claiming TPD benefits through a superannuation fund, some people ask, “Do I need a lawyer for a TPD claim?”

In brief, no. Although legally, anyone can make a TPD claim without a lawyer; it’s essential to understand that seeking TPD insurance benefits necessitates negotiating with an insurance company and super funds with extensive knowledge of the process, eligibility criteria, and restrictions.

Are you unsure if you need a lawyer to help you make a winning claim? Read on to understand the role of a lawyer in TPD claims and help you decide if hiring a lawyer is the right decision for you.

0 notes

Text

TPD, or Total and Permanent Disability, refers to a situation where an man or woman is not able to paintings due to a severe illness or harm. This disability can be bodily, intellectual, or a aggregate of both.

0 notes

Text

TPD: The Ultimate Guide to Total and Permanent Disability Insurance

When life takes unexpected turns, being financially prepared can be a lifesaver. Total and Permanent Disability insurance (TPD) provides a safety net in case of a severe injury or illness that leaves you unable to work. In this guide, we'll delve into the world of TPD insurance, exploring its features, benefits, claim process, and much more.

Understanding TPD Insurance

At its core, TPD insurance offers financial protection in the event of a disability that prevents you from earning an income. It ensures that you have a source of income to cover living expenses, medical bills, and other financial obligations. TPD insurance is typically available as a standalone policy or an add-on to life insurance.

The Types of TPD Cover

There are two main types of TPD cover: Own Occupation and Any Occupation. The Own Occupation cover provides a benefit if you're unable to work in your specific profession. On the other hand, the Any Occupation cover pays out if you're unable to engage in any form of gainful employment for which you're reasonably qualified.

Benefits of TPD Insurance

Financial Security: TPD insurance provides peace of mind, knowing that you won't be left financially stranded in the face of a disability.

Flexibility: The payout from TPD insurance can be used to cover medical expenses, mortgage payments, education costs, and more.

Debt Repayment: TPD cover can help you manage debts and loans while you're unable to work.

Reduced Stress: With financial worries alleviated, you can focus on recovery and rehabilitation.

Eligibility and Premiums

To be eligible for TPD insurance, you generally need to be within a specific age range and meet certain health criteria. Premiums vary based on factors like age, occupation, and chosen coverage amount. It's essential to understand these factors when considering TPD insurance.

Making a TPD Claim

Medical Documentation: You'll need to provide medical evidence that supports your disability claim.

Claim Forms: Fill out the necessary claim forms accurately and comprehensively.

Assessment Process: The insurance company will assess your claim, considering medical reports and other relevant information.

Waiting Period: There's usually a waiting period after the claim is approved before you receive the payout.

TPD vs. Workers' Compensation

While TPD insurance and workers' compensation both provide financial support for disabilities, they differ in scope. Workers' compensation typically covers disabilities sustained at work, while TPD insurance covers disabilities regardless of where they occur.

Is TPD Insurance Worth It?

The value of TPD insurance depends on your individual circumstances. If you have dependents, debts, or significant financial commitments, TPD insurance can offer invaluable security.

TPD Insurance: A Personal Connection

My own journey with TPD insurance began when a close friend faced a life-altering accident. Witnessing the financial strain it placed on their family, I understood the significance of TPD insurance in safeguarding against the unforeseen.

Conclusion

Total and Permanent Disability insurance is a crucial safety net that ensures your financial well-being even in the face of unexpected disabilities. By providing a reliable source of income, TPD insurance offers peace of mind, allowing you to focus on recovery and rebuilding. Assess your needs, explore policy options, and secure your future with TPD insurance.

FAQs About TPD Insurance

1. What is the waiting period for a TPD insurance claim? The waiting period varies by insurer but is typically around 90 days after the claim is approved.

2. Can I have TPD insurance alongside workers' compensation? Yes, you can have both TPD insurance and workers' compensation coverage simultaneously.

3. Are mental health conditions covered by TPD insurance? Yes, many TPD policies cover disabilities arising from mental health conditions.

4. How often should I review my TPD insurance policy? It's recommended to review your policy annually or whenever significant life changes occur.

5. Can I increase my TPD coverage after purchasing the policy? In most cases, you can increase your coverage amount, but it may require additional underwriting.

Please support us by hitting the like button on this prompt. This will encourage us to further improve this prompt to give you the best results.

0 notes

Text

‘Aussie Injury Lawyers’ Is Raising Awareness About Hidden TPD Insurance Payouts That Could Run Into Millions

http://dlvr.it/SpJTwb

0 notes

Text

Different Types of Personal Insurance

Personal insurance Sydney provides protection against the risks of illness, accidents and loss of income. There are different kinds of cover based on your needs and preferences.

There are some quick and easy plans available but you should be sure they meet your needs and are worth the cost. You might be able to get some discounts and rebates from health funds.

Life cover

Life cover is a type of personal insurance Sydney that pays out a lump sum to your beneficiaries if you die. This can help your family deal with the financial impact of your death, such as mortgage repayments and other household bills.

You can get life cover through a retail policy, directly with an insurer or through your superannuation. A broker will also give you tailored advice on securing cover.

Stepped premium policies cost more in the early years but become much cheaper with age. This favours people who plan to hold their life insurance for many years to come.

TPD (Total and Permanent Disability) is an optional extra that can pay a lump sum if you suffer a serious illness or injury, making it more difficult for you to work.

You can use the Budget Direct Life Insurance calculator to work out how much life cover you may need. It takes into account your current and future financial circumstances, including any mortgages or large debts, school fees, ongoing living expenses and lifestyle.

Trauma cover

If you’re diagnosed with a critical illness, trauma cover can help ease the financial stress of recovering. It can also provide a safety net for your family.

Trauma cover pays a lump sum for a range of specified medical conditions, including cancer and heart disorders. It can be purchased separately or bundled with life and total permanent disability (TPD) insurance.

You choose the level of trauma cover based on your financial needs. You can also increase or decrease the amount at any time. Alternatively, you can select inflation protection which adds incremental increases (usually 5%) to your sum insured.

Accident cover

Personal accident cover is designed to compensate for a loss of income* when you're injured and unable to work. The payout can help to manage living expenses, bills and any ongoing loan payments while you recover.

It also provides financial security to your family in case of accidental death. This can be a good option for the self-employed and contractors who aren't covered by workers' compensation.

You can choose between a number of options for your personal accident insurance policy including the waiting period and benefit level you want to receive. This will have an impact on your premium.

The University of Sydney maintains a Personal Accident Policy for all full and part time students, non student members and volunteers as well as staff of the Sport Unit. This covers you while on campus and/or engaged in University, course and sport related activities and practical placement or community placement activities, as well as travel to and from these activities.

Home insurance

Home insurance is designed to cover the cost of repairing or replacing your property should something happen to it. This can include a fire, storm or flood as well as theft and vandalism.

The amount of insurance you need will depend on your needs and the value of your property. Check that you’re not underinsured by using an insurer’s building and contents calculators, or a professional valuation from a licensed builder or valuer.

It also helps to have the right insurance product to meet your needs, and the right advice from an experienced insurance broker. The team at Morgans Sydney will help you navigate the home insurance market, find the best policy for your needs and keep you updated on any policy changes. We have a range of home insurance products to suit your lifestyle and budget. Contact us today to discuss your options. We can also recommend other insurance products you may not have considered, including landlord and travel insurance.

0 notes

Text

Temporary Disability Benefits in CA Workers Comp Cases

Temporary disability payments in workers comp cases can be an important source of income for accident victims who are unable to work for a period of time. Knowing your rights along these lines can help you sort through the process if you need to file a claim.

In fact, many people get confused about temporary disability and worker’s compensation. The following information will help you understand the differences.

TEMPORARY DISABILITY BENEFITS IN CA

Let’s begin by defining temporary disability benefits in CA and how they’re different from worker’s compensation.

What is Temporary Disability?

Benefits for temporary disabilities, which are part of workers comp, fall into two categories. These two classifications include:

Temporary total disability (TTD); and

Temporary partial disability (TPD), is commonly referred to as “wage-loss TD”.

Both are reimbursements that are designed to make up for missed wages while you are unwell or injured and recuperating. If you are completely unable to work while recovering, TTD payments are made as well.

If you are able to return to work, but only for a short time or with only a few tasks that pay less, you will still receive TPD benefits.

Should your doctor place limitations on the kind of job you may perform or your company only offers part-time work that complies with your restrictions, you may still receive temporary disability. You won’t pay taxes on the compensation.

WORKERS COMPENSATION BENEFITS

For workers injured on the job, worker’s compensation provides a safety net for employers. Nearly every firm in California is required to purchase the protection. Workers comp covers missed wages, medical expenses, attendant care, travel expenses to and from the doctor, prescriptions, and vocational rehabilitation.

To receive the money, you need to alert your employer about your accident and ask for time off to receive the compensation. These benefits last as long as you’re in recovery and you need medical care. Like temporary disability, these payments are tax-free.

FILING FOR SHORT TERM DISABILITY – HOW IT CAN COMPLICATE THINGS

What throws a wrench in the whole process is if an employee files a short-term disability claim, which is separate from workers comp. In this case, you need to consult with a temporary disability benefits lawyer immediately. You should seek their counsel anyway if you’re hurt on the job, as they can help you file your claim successfully.

In some cases, an employer may try to force an employee to use their short-term disability insurance instead of filing for workers comp. Also, you need to watch out if an employer wants you to take your time filing a claim. Doing so can limit your recovery options.

If you have your workers’ comp claim disputed, that’s when you should use short-term disability – only as a stop-gap measure. This might prove helpful if you’re needing money to survive and are waiting for the resolution of your worker’s comp claim.

If you receive workers comp later, you’ll need to reimburse your short-term disability insurance company for the payout.

HOW STD DIFFERS FROM TEMPORARY DISABILITY

The difference between temporary disability and short-term disability is that short-term disability (STD) is private insurance while temporary disability benefits are part of worker’s compensation – given to you for your lost wages when you cannot work. Therefore, temporary disability is a form of short-term disability, but it is a state-mandated payment.

TTD and TTP payments are only made to you if you’re injured on the job and cannot perform your assigned tasks, or can only do so with limitations.

HOW MUCH ARE TEMPORARY DISABILITY PAYMENTS?

What you receive in temporary disability benefits in California will depend on what you were earning at the time of your accident. You’ll receive a percentage of your average earnings. You may also ask your workers comp adjuster for a projected estimate.

You’ll need to provide medical proof when submitting the claim – showing medical evidence that your injury is preventing you from working.

WHEN CAN YOU RECEIVE TEMPORARY DISABILITY PAYMENTS?

In California, you can receive temporary disability every two weeks, beginning with the first payment, which is paid 7 days after you make a claim. Again, you’ll need to provide a medical report that states you cannot work or must cut down on the hours you previously worked.

HOW LONG DO TEMPORARY DISABILITY PAYMENTS LAST?

You can collect temporary disability up until your doctor says you can return to work. In some cases, he or she may suggest making some modifications. If you don’t feel you’re ready to return to your job, notify your personal injury attorney.

In some instances, a doctor may tell a patient that they don’t expect them to improve – which is referred to as a phase known as “maximum medical improvement” (MMI). This means that you should file for permanent disability right away.

In some cases, you may reach the limit on the temporary disability benefits allowed, according to state law. In California, you are restricted to 104 weeks of payments within a five-year time frame. This window of time begins on the date of your injury.

ARE THE SERVICES OF AN ATTORNEY ABSOLUTELY NECESSARY FOR YOUR WORKERS’ COMP CASE?

Although you do not necessarily need an attorney to handle your workers’ compensation claim, it is generally a good idea to contact a legal professional.

Your attorney will try to get you as much money as possible. They know what it takes to file a successful claim quickly and efficiently.

CALL A TEMPORARY DISABILITY BENEFITS LAWYER NOW

Temporary disability payments are a form of short-term workers’ compensation payments. In most cases, you will receive these payments if you have been injured while on the job and cannot work as a result.

0 notes

Link

https://tpdclaimslawyers.com.au/permanent-impairment-claim-lawyers/

0 notes

Text

Carter Capner Law

Carter Capner Law provides insurance and compensation recovery services to the people of Queensland and in the city of Brisbane. Our team of no win no fee lawyers guarantee expert and cost-effective insurance and compensation legal services to individuals and families.

The ‘no win no fee’ fee terms we offer in most compensation practice areas ensures accessibility to legal services that are guaranteed for quality.

Car and Vehicle Accidents

Sickness & Accident policy claims apply to injuries resulting from car, motorcycle, truck, boat and bicycle accidents. Our Brisbane car accident lawyers can review your injuries and your policy and determine the extent to which you qualify for an insurance payout. You will likely be entitled to medical costs and other expenses as well as a sum determined by the nature and extent of your injury.

Workplace Accidents

Income replacement and TPD claims policy coverage extends to accidents occurring in the workplace. Negotiating a payment from the insurer for injuries sustained in the workplace is often a difficult process. Our Brisbane workers compensation lawyers can guide you through negotiation and if required, litigation to compel payment of the insurance claim for the full amount due to you.

Travel Accidents

If you have suffered travel injuries because of the actions or negligence of someone else, then you may be able to make a claim for personal injury compensation. We can help you with your compensation claim and guide you through the process. See how our travel injury lawyers in Brisbane can help you now.

Medical Accidents

All healthcare providers are required to meet strict regulatory standards or for clinical oversights and failings, delayed diagnoses, failure to perform medical procedures with appropriate skill, and failure to provide follow-ups and referrals.

Public Liability Accidents

If you have suffered Public Liability injuries because of the actions or negligence of someone else, then you may be able to make a claim for personal injury compensation. We can help you with your compensation claim and guide you through the process. See how our Brisbane Public Liability Lawyers can help you now.

Recreational Accidents

If you have suffered a recreational accident because of the actions or negligence of someone else, then you may be able to make a claim for personal injury compensation. We can help you with your compensation claim and guide you through the process. See how our expert Recreational Injury lawyers in Brisbane can help you now.

Other insurance payouts

Income replacement and sickness & accident policy coverage applies to injuries occurring in most circumstances. Carter Capner can assist you with your claim for your injuries such as sexual abuse / sexual assault. Go to Compensation Claims for more information.

1 note

·

View note

Text

Life Insurance coverage in Singapore – The Fundamentals of Complete Life and Time period Insurance coverage

This entire insurance coverage factor actually does take some time to wrap your head round. The phrases “entire life insurance coverage” and “time period insurance coverage” don’t actually imply or clarify very a lot to the common individual.

The typical Singaporean can also be educated from a younger age to run away from individuals who wish to have such conversations with you, as in the event that they had been contaminated zombies. Nonetheless, in some unspecified time in the future in your adulting, you come to the dreadful realisation that insurance coverage isn’t avoidable for ever and that there’s worth to getting a minimum of some form of life insurance coverage coverage.

We’re right here to arm you with some primary data earlier than you face an insurance coverage agent, so you understand what you’re entering into.

Contents

Complete life vs time period insurance coverage – what’s the distinction?

Endowment vs investment-linked entire life insurance coverage insurance policies

What’s the distinction by way of premiums (value)?

Who should purchase entire life insurance coverage?

How does “restricted pay” work?

What’s “give up worth”?

What’s the distinction between entire life and time period insurance coverage?

An insurance coverage coverage supplies safety for monetary losses suffered from a selected occasion. Within the case of life insurance coverage, the “occasion” is the lack of your life, or within the case of complete everlasting incapacity (TPD). To place it merely, a life insurance coverage coverage is designed such that in the event you die, the insurer’s payout ought to be sufficient to your dependents to reside on when you’re gone.

However before you purchase any form of life insurance coverage, you’ll want to determine whether or not you’ll go for entire life insurance coverage or time period insurance coverage. What’s the distinction between them, and which is best for you?

Time period insurance coverage

Complete life insurance coverage (endowment)

Complete life insurance coverage (investment-linked)

Essential goal

Safety

Safety + potential to develop financial savings

Safety + potential to reap funding returns

Protection

Most plans cowl dying and complete everlasting incapacity (TPD)

Protection Interval

A selected time period interval or as much as a particular age

Normally as much as finish of life

Normally as much as finish of life

What’s paid upon dying of insured?

Sum assured

Sum assured + accrued bonuses if any

Sum assured + worth of models in fund

What’s paid if coverage is surrendered early?

Nothing, since there isn’t any money worth

Money worth (assured + non-guaranteed bonuses if any)

Worth of models in funding sub-fund

Each time period and entire life insurance coverage present safety within the occasion of complete everlasting incapacity (TPD) and dying. The 2 principal variations between them are: (a) how lengthy the coverage will cowl you and (b) how a lot cash you get again if nothing occurs to you.

Time period insurance coverage supplies you with safety just for a set time frame, say 20 or 30 years, after which the plan expires. If nothing occurs to you and also you don’t make a declare, you get nothing (aside from a letter thanking you for giving them cash for the final 30 years).

Such a protection is cheaper, and it is smart in the event you plan to offer to your dependants for a restricted time. For instance, till your youngest little one finishes tertiary schooling.

Alternatively, entire life insurance coverage covers you until the tip of your life, so long as you proceed to pay the premiums.

It’s rather more costly, but it surely has the potential to develop the cash you paid. The potential progress varies relying on whether or not your entire life insurance coverage is an endowment plan or an investment-linked coverage (ILP). Extra on these within the subsequent part.

In both case, the “benefit” of entire life insurance coverage over time period insurance coverage is that, even in the event you terminate and give up the coverage, you may get again a number of the financial worth.

]]>

Sponsored Message

Give your family members the monetary safety they deserve and luxuriate in nice financial savings. Singapore Life is providing as much as 15% off once you apply for a Time period Life or Important Sickness plan by 30th September. Discover out extra right here.

Again to prime

Endowment vs investment-linked entire life insurance coverage insurance policies

In Singapore, entire life insurance coverage often features a financial savings or funding part, named endowment and investment-linked coverage (ILP) respectively.

Resulting from these options, some individuals see their entire life insurance policies as an funding/financial savings plan as an alternative of simply being a plain previous safety plan. These added options make entire life insurance coverage costlier than time period insurance coverage.

Endowment Insurance policies

Endowment insurance policies are sometimes seen as a method that can assist you construct up monetary self-discipline because the financial savings part is constructed into the month-to-month insurance coverage premiums.

For example, let’s say you pay a month-to-month insurance coverage premium of $250 to your endowment coverage. Of this quantity, $100 would possibly go into the insurance coverage safety part, and $150 will go into the financial savings part.

After a set interval of say 20 years, it is possible for you to to get again a number of the money worth accrued, relying on the assured and non-guaranteed advantage of your coverage.

Funding Linked Insurance policies (ILP)

For an ILP, the financial savings part will likely be changed with an funding part the place a part of the premiums go into shopping for models in funding funds.

In contrast to endowment insurance coverage insurance policies, ILPs often don’t include assured values. The worth of the ILP relies on the efficiency of the fund you’ve purchased into. So yeah, you could possibly get zilch if issues don’t go effectively and this represents a possible alternative value as you could possibly have made that cash work some place else for you.

Some customers like ILPs as a result of they like the concept they will make investments and have monetary safety by way of a single monetary product. There’s even have a variety of funds to select from that fits totally different funding targets and danger urge for food.

Whether or not you select to purchase a time period insurance coverage, endowment plan or ILP, the primary factor is to determine in case your selection fulfils your monetary goal and takes into consideration the long-term prices concerned.

Again to prime

Let’s evaluate the premiums for entire life vs time period insurance coverage

Whereas life insurance coverage was the “go-to” insurance coverage for most individuals, with elevated monetary literacy, extra individuals are open to getting time period insurance coverage as an alternative.

One of many best benefits of selecting a time period insurance coverage as an alternative of a life plan is the substantial financial savings you get from decrease premiums. So if you understand you want insurance coverage safety however are in a section of life the place you possibly can’t afford setting apart very a lot each month, this turns into your best option for now.

Right here’s a simulation of how a lot insurance coverage premium an individual pays for all times and time period insurance coverage based mostly on the next standards: 35-year-old man, non-smoker with sum assured of $500,000. Let’s name him Mr Siva.

Kind

Life insurance coverage coverage

Annual value

Whole quantity paid

Time period

FWD Insurance coverage Time period Life

$510

$510 x 30 years = $15,300

Time period

Nice Japanese Max Time period Worth

$840

$510 x 30 years = $25,200

Complete life

NTUC Restricted Pay Safety

$10,038

$10,038 x 29 years = $291,103

Complete life

AXA Life MultiProtect

$13,440

$13,440 x 30 years = $403,200

As you possibly can see, the distinction within the quantity of premiums paid between time period and entire life insurance coverage is big.

This is the reason some monetary advisors even advocate “purchase time period and make investments the remaining”. In different phrases, purchase a time period coverage for the required safety, after which use the cash you didn’t use to take a position. This can be a technique that has the potential to develop your cash in the event you make the appropriate funding selections.

Alternatively, some customers prefer to get an entire life coverage as a result of it presents some money worth do you have to determine to give up the coverage.

Primarily based on the assured give up worth (after 30 years) for the above entire life insurance policies, one can anticipate to obtain $246,000 and $307,000 for the NTUC and AXA plan respectively. Utilizing these values, it signifies that the full premiums paid to your entire life coverage will likely be diminished considerably this brings it extra on-par to time period plans by way of value.

One necessary consideration when selecting to take up a time period plan is that the protection time period could expire at a time the place you’ll proceed to wish safety (or want it most).

For the above case, the time period plan will expire when Mr Siva is 65 years previous. Relying on his state of affairs, Mr Siva could wish to proceed getting life insurance coverage protection for one more 20 years.

Nonetheless, relying on his well being at 65, some firms could think about him “uninsurable”. Even when he does qualify for a brand new insurance coverage plan, premiums are going to be very costly at that age, and he could not be capable of afford them throughout his retirement years.

Again to prime

Who should purchase entire life insurance coverage?

Whereas it might appear that the “purchase time period and make investments the remaining” mantra makes complete financial sense, there are cases the place shopping for entire life insurance coverage is usually a better option.

Whether or not you want life insurance coverage actually relies on your stage in life. If you’re a younger 20-something with no dependents and restricted obligations, you’ll possible not want an entire life insurance coverage coverage.

However say you’re 40-year previous, and the only breadwinner in a household with two younger youngsters and aged dad and mom. In such a case, entire life insurance coverage can assist to offer monetary safety to your family members whereas concurrently serving to you construct up some retirement funds to your golden years.

Life insurance coverage protection is a method of caring for your loved ones, since you don’t need them to endure when any misfortunate befalls you. In a survey by NTUC Revenue revealed in April 2019, 48% of 329 married adults surveyed expressed that they had been motivated to purchase life insurance coverage as a result of they need their family members to take care of the identical lifestyle when catastrophe strikes.

The opposite state of affairs the place entire life insurance coverage could make sense is to your younger little one. You would possibly assume, “why would my 2-year previous want entire life insurance coverage?”

For one, it ensures insurability and no-exclusions since most younger youngsters have a clear invoice of well being. Many dad and mom additionally take up an entire life coverage with endowment plan with a view to begin saving for his or her little one’s future schooling. Additionally, your little one is prone to get pleasure from decrease premiums when getting insured from a youthful age.

For those who’re getting an entire life coverage for a kid, selecting a restricted pay possibility will be a good suggestion. Your little one can get a life-long protection with premium funds for as quick as 12 years. It may well thus be a significant present for a younger little one as an alternative of saving cash in a financial institution deposit account that can’t beat inflation.

Again to prime

How does “restricted pay” work?

Getting a life insurance coverage with restricted pay interval means you solely have to pay premiums for a restricted variety of years in change for a lifetime’s protection.

Say for example, Andy (male, non-smoker, age 35) decides to make premium funds of S$250 per thirty days for under 15 years for his entire of life plan up until age 50.

For the subsequent 15 years, Andy pays about S$45,000 for a sum assured of S$100,000. The insurance coverage protection will proceed for remainder of his life even after he ends his premium cost at age 50. Relying on his insurer and plan, he’ll possible even be entitled to some accrued money worth if he surrenders his coverage when he reaches 65 years previous.

What is that this “give up worth” factor?

Once you purchase a life insurance coverage, you could have a give up proper – the chance to terminate your life insurance coverage contract in change for its money worth. You may solely do that in the event you’ve not made any claims earlier than.

Once you select to give up your coverage, you’ll hand over the remaining protection whereas your insurer presents you with a money give up worth, which is how a lot cash you’ll obtain in return.

Do observe that the give up worth of your coverage will likely be decrease than the dying profit payout. Which means you’ll obtain much less cash by surrendering your coverage as in comparison with having the dying profit once you move on. Thus, it’s usually not advisable to give up your coverage. Not solely will you lose out by way of financial worth, however taking over a brand new insurance coverage coverage at a later age will most likely incur the next premium cost.

In the end, there’s no proper or incorrect in selecting whether or not to get a time period plan or entire life insurance coverage – all of it relies on what you want and the way a lot you possibly can afford.

Complete life insurance coverage prices extra, however it may be a handy possibility for many who need each monetary safety in addition to a financial savings/funding part. Alternatively, a time period life insurance coverage plan presents a terrific cost-effective possibility for many who need (solely) pure safety.

What are your ideas on shopping for life insurance coverage? We wish to hear from you.

Associated articles

Well being Insurance coverage in Singapore – The whole lot You Must Know to Survive 2018

The Most cost-effective Automobile Insurance coverage Insurance policies in Singapore (UPDATED 2018)

The Finest Journey Insurance coverage in Singapore – 2018 Overview

]]>

Tags: Featured, Life Insurance coverage

from insurancepolicypro http://insurancepolicypro.com/?p=81

1 note

·

View note

Text

Most people fail to realize the importance of this protection

When it comes to planning your protection needs, even the best of us overlook the importance of Personal Accident (PA) insurance.

They can’t be blamed, because even insurance representatives including agents and bank telemarketers do not understand the importance of a PA policy. Most would focus on selling the relatively low cost of the policy, and the benefits of being able to claim for certain medical expenses.

I myself was not covered by any Personal Accident policy until 4 years ago when as a favor for my help, a friend who works as an insurance agent bought me a PA plan as a gift.

Even then, all I knew about the plan was it allowed me to claim medical expenses in the event of an accident, even if it meant going for alternative medicine, such as a Sinseh (Traditional Chinese Medicine Practitioner) or a Chiropractor.

But as I joined the industry, I realized that a PA plan is not just a medical reimbursement policy. Beyond medical reimbursement, it also covers accidental death, partial dismemberment, hospital income, and total permanent disability. As I always share with my colleagues, there are only 3 major ways to die – Old age, major illness, or an accident. Statistics reveal that approximately 1 in 20 Singaporean, die in an accident. So, do you now realize, how important PA insurance is?

Here are more reasons why you need to get covered for PA

1. Medical Reimbursement

As mentioned, most PA policies allow you to seek medical reimbursement in the event of an accident. You might think that this is not very much different compared to a hospitalization policy. However, the key difference is, you do not need to be hospitalized to be able to make a claim from your PA policy. More importantly, it covers you 24/7 worldwide.

You might have suffered a fracture that requires an MRI to be done, yet it’s not serious enough to warrant a stay at the hospital. That would have cost you well over a thousand dollars, and adding on the subsequent consultation fees, it’s not a bill one would like to be burdened with.

Real Life Example:

Recently, a friend approached me to plan for a Life policy. After going through her needs and a budget, I proposed a Life policy with a PA rider – the policyholder gets a discount for his PA policy when it’s tagged on as a rider to a Life policy. She was hesitant at first, choosing to use his spare budget for a higher sum assured. While that could mean a higher commission for me, I was insistent on my original proposal which provided for a well-rounded protection and she took the recommendation.Just weeks after the policy was in-forced, I received a text from that very friend. She had just injured her back while practising Yoga. The bill which included a visit to the orthopedic and an MRI scan amounted to over $1,700. Had I not insisted what I thought was the best policy for my client, she might not have been covered adequately.

2. Accidental Death, Partial Dismemberment, and Total Permanent Disability - All covered in one plan

Most people who think insurances are scams might have heard of stories from people who could not claim from their Life Insurance policy for a permanent injury such as the loss of an eye, an arm, or a leg.

While unfortunate, these injuries do not fall under the definition of a Total Permanent Disability* in a Life Insurance policy. In fact, a PA policy is the only insurance which pays out for a partial dismemberment down to the loss of a finger or a toe. Payouts range from 1% to 150% of the sum assured.

* Classical definition of Total Permanent Disability requires at least 2 of the above: Loss in Sight in one eye, one arm, or one leg. One macabre (but easily understood) way of explaining it was: Place your eyes, hands and legs in a bag – only when 2 are rendered unusable, is TPD then claimable.

3. Low-cost plan with coverage when you need it most

While your family might suffer financial hardship without you around, their financial wellbeing could be worse if you were bedridden and are unable to provide for yourself and your family. For less than a dollar a day, a PA policy provides a $100,000 sum assured, with all the above benefits and more. It is truly a hidden gem in the world of financial planning.

Moral of the Story: Plan your Coverage

Fundamentally, most personal accident policies offer you protection from an accident. However, the benefits vary from plan to plan, and it is important to discuss your needs with your financial planner.

He or she might be able to review your policies to ensure that you have decent coverage for your limited budget. For example, if you’re self-employed, you might want to be covered for a temporary disability income if the accident leaves you out of work for an extended period.

And because accidents can happen so frequently, it is also important to obtain your protection from a representative that you can count on being there for you – the last thing you want to do when something happens, is having to go to a counter or going through endless answering machines.

If you are looking for reliable representatives, be sure to drop us a message on our Facebook Messenger

1 note

·

View note

Text

Lump-Sum Workers Compensation Claims: A Guide To Understanding Your Benefits.

A worker who has suffered an injury at work can receive two types of Workers’ Compensation. The first is a lump sum, and the second is periodic payments. Each has its respective pros and cons, and when choosing between them, you must consider your financial situation and the specific details of your case to select the option that will provide you with the most money.

Lump-sum claims are also known as "total permanent disability" (TPD) or "total and permanent disability" (TPD) claims. They are designed to provide a lump-sum payment for the total cost of workers compensation cover if you are deemed totally and permanently disabled.

The lump sum is calculated based on your pre-injury earnings. The maximum amount payable is $415,000 (2017).

Note: Lump sum settlements are not the same as lump-sum buyouts, which are agreements in which the injured worker gives up the right to additional medical care and lost wages in exchange for a more significant initial settlement amount.

Lump-Sums Payments

A lump-sum payment is an option that allows you to receive compensation for your permanent disability at a single, upfront cost rather than waiting for the end of the claim process. Lump-sum charges are available in the United States if:

● You have suffered a permanent impairment or disability;

● Your injury has left you unable to continue working; and

● You have reached maximum medical recovery and are qualified for a lump sum payment under USA's lump sum provisions.

They can be used as a form of rehabilitation or awarded to a claimant who has sustained permanent injuries while working. Lump sums are based on the severity of the damage, and they are not subject to income taxes. A lump sum is available in most states and at the discretion of the insurance company or employer.

The trend in the past of paying lump sums to workers' compensation claimants has changed. Now, companies are paying lump sums to those who have suffered severe injuries to help them return to gainful employment.

Most workers are not even aware that they have options in a lump sum settlement and may negotiate a higher price by presenting their employer with a plan for the future use of the money.

Once the parties agree to settle a claim for a lump sum, the injured worker will receive instructions on how to claim their funds. The Department of Industrial Accidents (DIA) handles all lump sum settlements and can answer any questions you might have.

However, these payouts are not awarded to everyone, and there are specific criteria required before a lump sum payment is approved.

Who is eligible for Lump-Sum Payment?

Just because you've been injured at work doesn't mean you'll automatically eligible for lump sum payment. So, who is eligible for lump-sum payments for workers' comp? In most cases, the answer is someone who has been injured on the job and is receiving ongoing treatment. However, some other situations may qualify you for a lump sum payment.

To be eligible for a lump-sum payment:

● You must have been injured while working.

● You must also have been treated by a licensed workers' compensation doctor and have had a reasonable number of visits to your doctor or rehabilitator.

Every state has its own workers' compensation laws and regulations. The eligibility criteria for lump sums vary from state to state. In most states, if you become permanently disabled after a work-related injury, you will be eligible for up to three years worth of payments.

When determining the amount of a lump sum award, the state is required to consider your ability to work. If you can work in another job, you will receive a large payment, but if you are permanently disabled, you may receive a smaller amount. A Workers' Comp Lawyer can help you determine how much money you may be entitled to receive by filing a claim with the workers' compensation board.

If you plan to file a Workers' Compensation Claim, check out our Workers' Compensation blog.

Contact the experienced and helpful team of attorneys at Pistiolas Workers' Compensation Lawyers today if you're currently looking into workers compensation claims.

If you have any questions about Lump-sum Workers' comp payments and how they work, feel free to give us a call at 844-414-1768.

Don't hesitate to contact us today for a free consultation for all your legal needs.

https://workerscomplawcalifornia.com/

0 notes

Text

TPD insurance is designed to provide financial support through a lump sum payment, known as a TPD benefit, for Australians who can’t work due to an injury or illness. Many workers don’t know this coverage is included in their superannuation fund. Thankfully, you can access this valuable insurance benefit when you can’t earn an income.

0 notes

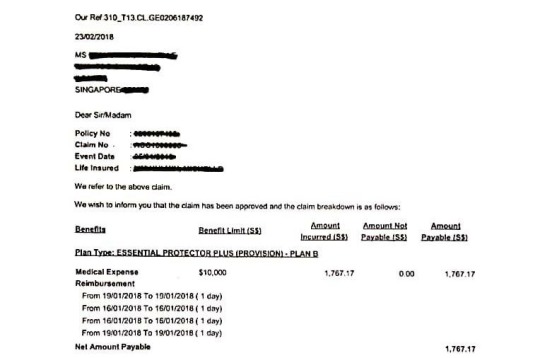

Text

Successful superannuation TPD claims help relieve the financial burden that accompanies an unexpected illness, injury or mental illness that stops you from working. Are you considering making a TPD claim? Our legal guide explains Total and Permanent Disability claims and reveals how to make the most of TPD insurance claims.

0 notes

Photo

If you've suffered a permanent disability, Financial Advisors Brisbane can help you get the payout you deserve with our Total and Permanent Disablement (TPD) insurance policy. Don't struggle to pay your medical expenses or debts - let us help you get back on your feet....

0 notes

Text

Permanent disability Insurance

When a person is unable to work and may never work again as a result of injuries sustained in an accident or other mishap, this is referred to as total permanent disability (TPD). Individuals must insure themselves with total and permanent disablement coverage because the future is uncertain, and if a mishap occurs, who will bear the entire burden of the family? When a person is covered by insurance, his or her children's loans are discharged if the person is unable to work for a period of time or until death. Unisuper offers TPD coverage based on your age or as a fixed amount. The following are the reasons why total and permanent disability insurance is important:

Support your family- If you are forced to leave your job due to an unfortunate event, you will face a slew of financial difficulties, and as your debt piles up, life will become increasingly difficult for you and your family. In such cases, total and permanent disability insurance provides a sigh of relief for the family because you are paid a lump sum amount and, in some cases, your child loan is discharged. Unisuper has some good TPD insurance plans.

Type of occupation- You should talk to your financial advisor about the type of total and permanent disability insurance you should get. Different insurers have different payout expectations. Your premium would be higher if you worked for yourself, but you would not have any difficulties settling your claim. While other occupations, such as job premiums, may be less expensive, settling claims is quite difficult. Unisuper ensures that you have no difficulties in settling your claim.

Disability types covered- You should think about the type of coverage you need based on your job. Consider how much money you would require if your income were to be interrupted due to an accident. Not all disabilities are covered, but those that are, provide a substantial return. Different company's terms and conditions may differ. Consider all options and choose the one that best suits your work. Loss of one or both hands or legs, as well as loss of vision, are common injuries. Unisuper offers flexible total and permanent disability coverage based on your specific needs.

Conclusion

These are some of the most important factors to consider when purchasing total and permanent disability insurance.

0 notes

Text

He Lost a Fortune in Eight Days

1

That time I was pissed that I lost a twenty dollar bill

He Lost a Fortune in Eight Days. I lost a $20 bill. I feel more aggrieved.

There was this time, last week I think it was, I lost track of a twenty. I'm still mad.

I wonder how this guy goes on.

He lost $8 BILLION in 10 days. You'd have to keep me in a padded room with no access to sharp objects.

It was the “biggest single-firm meltdown since the financial crisis,” per the WSJ, and it’s causing introspection in finance about the ability of private family offices to cause market havoc.

Morning Brew

Gee, ya think?

2

To say the tide is turning on this one would be a massive understatement.

The Chief of Police in Minneapolis is going to take the witness stand in the Derek Chauvin trial. It's not expected to go well for Chauvin, to put it mildly.

Minneapolis police chief Medaria Arradondo is expected to take the stand as soon as today, as testimony in the Derek Chauvin trial continues for a second week.

Yahoo News

Arradondo, who fired Chauvin and three other officers last summer after George Floyd died was murdered, has said this was murder and will, in fact, state that Chauvin did not follow the training MPD are given.

This could be devastating. Or not. I'm still skeptical AF one juror just won't see what happened here.

Full coverage here.

3

Just another day at Facebook

The exposed data includes the personal information of over 533 million Facebook users from 106 countries, including over 32 million records on users in the US, 11 million on users in the UK, and 6 million on users in India. It includes their phone numbers, Facebook IDs, full names, locations, birthdates, bios, and, in some cases, email addresses.

Business Insider

Meh, it's two years old (says Zuck) and everybody knew your phone number and they don't care about you any way. Meanwhile, get ready for some spam–it's what's for dinner now.

4

Florida man…in this case, it's the “Guvna”

Ron DeSantis has some explainin' to do, but he won't, because that's just not his thing.

Manatee County in Florida was under a state of emergency over the weekend and more than 300 homes were ordered evacuated because of a leak at a wastewater reservoir.

A significant leak was discovered Friday at the wastewater pond located at Piney Point, a former phosphate plant.

NPR

In fact, it's really no big deal, even though I ordered you to leave your house:

(DeSantis) said in a press conference Sunday that the water being dumped wasn't radioactive and that it's primarily salt water “mixed with legacy process water and stormwater runoff.”

So you should be alright. I mean, when has a government official at the highest level downplayed a drinking water issue?

5

This guy was the assailant:

Justin Arthur-Ray Davis (no relation)

A man has been arrested after stalking his former female colleague for over a month, shooting her husband and attempting to kidnap her from her own home.

The incident occurred on Friday, April 2, in Tulsa, Oklahoma, when the unnamed target of the kidnapping was leaving for work in the morning as her husband escorted her to her vehicle when they saw the suspect, Justin Arthur-Ray Davis, sitting in his truck nearby, according to a statement from the Tulsa Police Department (TPD).

“Davis has been stalking the victim for over a month after he resigned at their mutual work place,” TPD said. “She has made reports of Davis sitting outside her apartment and leaving candy and food on her door step.”

It was then that Davis got out of his truck with a shotgun and chased after the couple with it as they ran back into their apartment.

ABC News

It gets worse.

6

To think I used to call it “shitcoin.” My bad.

Daniel Maegaard, 30, of Brisbane, Australia, made a fortune not once, but twice: First, by hedging bets on various cryptocurrencies from 2013-2017, then, more recently, by getting in early on the explosion of non-fungible tokens (NFTs).

It’s a rare tale of how extreme risk-taking, timing, intuition, and a lot of luck resulted in a multi-million dollar payout.

And it began just 8 years ago, with an investment of a few thousand dollars.

The Hustle

Ah, to be young again. But wait, I didn't have “a few thousand dollars” then, either

The article was originally published here!

He Lost a Fortune in Eight Days

0 notes

Last Seen Blogs

notesandchai

taking notes drinking chai getting by

whore4kai

Gabriella♡

insanechayne

I’ve Been Diagnosed As A Threat To Society

fluid-isolation

You Have No Idea

szonjablade

cheetos is life