#Immuno-Oncology Clinical Trials Market

Text

In the rapidly growing field of global Immuno-oncology Clinical Trials Market size was valued at USD 8.92 billion in 2023 and is projected to reach USD 28.33 billion by 2032, growing at a CAGR of 13.7% from 2023 to 2032 according to a new report by Nova One Advisor.

0 notes

Text

The global immuno-oncology clinical trials market size was exhibited at USD 7.85 billion in 2022 and it is expected to hit around USD 28.33 billion by 2032, growing at a CAGR of 13.7% during the forecast period from 2023 to 2032.

0 notes

Text

Oncology Drugs Market Growth, Trends, Size, Share, Demand And Top Growing Companies 2031

In a landscape where the battle against cancer rages on, advancements in healthcare systems, public health measures, and novel pharmaceutical therapies have ushered in a new era of hope. According to the National Cancer Institute, the United States saw an estimated 1,806,590 new cancer cases and approximately 606,520 deaths due to the disease in 2020. However, over the past five decades, cancer survival rates have soared from 50% in 1970 to an impressive 70%, thanks to a trifecta of progress.

For more information: https://www.fairfieldmarketresearch.com/report/oncology-drugs-market

Unprecedented Growth Trajectory:

The global oncology therapy sales are forecasted to surpass US$ 300 billion by 2026, with oncology contributing 21.7% to total pharmaceutical sales. Fueling this growth are the top 10 pharmaceutical companies, which have declared oncology as their key focus area, driving multibillion-dollar M&A deals and strategic collaborations. Pfizer's acquisition of Array BioPharma for US$11 billion in 2019 and AbbVie's strategic partnership with Genmab for a bispecific antibody development deal worth US$3 billion are testament to this focus.

Diverse Indications Drive Demand:

While oncology represents over 20 different indications, a significant portion of revenue stems from just five of them: breast cancer, multiple myeloma, non-small-cell lung carcinoma (NSCLC), prostate cancer, and non-Hodgkin's lymphoma (NHL), which collectively accounted for approximately 65% of the market in 2020. Moreover, with breast, lung, and colorectal cancers expected to collectively account for ~50% of all new cancer diagnoses by 2026, the demand for innovative therapies continues to surge.

Disruptive Trends Reshape Landscape:

Innovation in oncology is accelerating, with disruptive technologies such as cell therapy, RNA therapy, viral vectors, and stem cell therapy gaining traction. Recent approvals of CAR-T cell therapies like Kymriah and Yescarta for acute lymphocytic leukemia (ALL) and diffuse large B-cell lymphoma (DLBCL) respectively signal a new frontier in cancer treatment. Precision medicine is also driving progress, with over 160 oncology biomarkers approved by 2019, paving the way for more targeted and effective therapies.

Impact of COVID-19:

Despite remarkable progress, oncology has been among the worst-hit therapeutic areas amid the COVID-19 pandemic. Decreased demand for physician-administered products, disruptions in cancer screenings, and a decline in new clinical trials have posed significant challenges. However, the industry remains resilient, adapting to the evolving landscape and ensuring continued innovation.

Immuno-Oncology Leads the Way:

Immuno-oncology sales are expected to soar to ~US$ 95 billion by 2026, with agents and protein kinase inhibitors comprising ~65% of sales. With over 550 active cell- and gene-therapy agents under clinical development, the future of cancer treatment looks promising. Investments in combination studies and the exploration of new mechanisms underscore the industry's commitment to advancing immuno-oncology therapies.Roche and Keytruda: Leading the Charge:

In a highly concentrated market where the top 10 companies capture over 75% of the market value, F. Hoffmann-La Roche AG (Roche) and Merck & Co. stand out as leaders. While Roche maintains its global leadership position, Merck's Keytruda is poised to become the world's top-selling oncology

0 notes

Text

PRISM MarketView Marks World Cancer Day

New York, N.Y., February 01, 2024 - PRISM MarketView, a leading provider of unbiased market insight and company news, today recognizes the tremendous contributions of companies striving to develop treatments for cancer, a complex disease driven by numerous factors. It is a leading cause of death worldwide, accounting for nearly 10 million deaths in 2020, and is the second leading cause of death in the United States.

To mark World Cancer Day, which will be held on February 4, PRISM MarketView highlights emerging companies working to improve the lives of cancer patients and their families by developing and commercializing innovative new treatments for cancer.

Panbela Therapeutics, Inc.

Biopharmaceutical company, Panbela Therapeutics, is developing disruptive therapeutics for patients with urgent unmet medical needs. The company's lead product candidates are Ivospemin (SBP-101), which has completed a Phase Ia/Ib clinical trial for the treatment of patients with metastatic pancreatic ductal adenocarcinoma. The company has entered a research agreement with the Johns Hopkins University School of Medicine for the development of Ivospemin. Panbela recently announced it has reached 50% enrollment for its global randomized, double-blind placebo-controlled ASPIRE clinical trial to evaluate ivospemin in combination with gemcitabine and nab-Paclitaxel in patients with metastatic pancreatic ductal adenocarcinoma. Panbela’s market cap stands at approximately $672,341.

Lisata Therapeutics, Inc.

Lisata Therapeutics, Inc., is developing and commercializing innovative therapies for the treatment of solid tumors. Its lead oncology product candidate is LSTA1, which is in Phase 1b/2a and 2b clinical studies for the treatment of solid tumor, including metastatic pancreatic ductal adenocarcinoma (mPDAC), in combination with a range of anti-cancer regimens. The company recently announced it had treated the first patient in a Phase 2a trial evaluating LSTA1 in patients with newly diagnosed glioblastoma multiforme (GBM). LSTA1 has been granted orphan drug designation by the FDA for malignant glioma. Lisata’s market cap stands at $21.163 million.

Rigel Pharmaceuticals, Inc.

Biotechnology company, Rigel Pharmaceuticals, is developing therapies that enhance the lives of patients with cancer. The company's commercialized products include Rezlidhia, a non-intensive monotherapy for the treatment of adult patients with relapsed or refractory (R/R) acute myeloid leukemia (AML). The company has entered a strategic development collaboration with The University of Texas MD Anderson Cancer Center for the development of REZLIDHIA (Olutasidenib) in acute myeloid leukemia (AML) and other hematologic cancers. The company recently announced a collaboration with CONNECT, an international collaborative network of pediatric cancer centers, to evaluate REZLIDHIA® in combination with temozolomide as maintenance therapy in newly diagnosed pediatric and young adult patients with high-grade glioma. Rigel’s market cap is currently $210.116 million.

AIM ImmunoTech

AIM ImmunoTech is an immuno-pharma company focused on the research and development of therapeutics to treat multiple types of cancers. The company's lead product candidate is Ampligen, which the company is evaluating for the treatment of renal cell carcinoma, malignant melanoma, non-small cell lung, ovarian, breast, colorectal, prostate and pancreatic cancer. The company recently announced is had enrolled the first subject in a Phase 1b/2 clinical trial combining AIM’s Ampligen® (rintatolimod) with AstraZeneca’s anti-PD-L1 immune checkpoint inhibitor Imfinzi® (durvalumab) for the treatment of late-stage pancreatic cancer. AIM ImmunoTech’s market cap is $20.851 million.

Essa Pharma

Essa Pharma, a clinical stage pharmaceutical company, is focused on the development of small molecule drugs for the treatment of prostate cancer. The company recently presented updated dose escalation data from its Phase 1/2 study evaluating masofaniten in combination with enzalutamide for the treatment of prostate cancer at the 2024 ASCO Genitourinary Cancers Symposium. It has collaboration agreements in place with Bayer Consumer Care AG; Janssen Research & Development, LLC; and Astellas Pharma Inc. and its share price has been trending upwards since October 2023. Essa Pharma’s market cap is currently sitting at $364.35 million.

About PRISM MarketView:

Established in 2020, PRISM MarketView is dedicated to the monitoring and analysis of small cap stocks in burgeoning sectors. We deliver up-to-the-minute financial market news, provide comprehensive investor tools and foster a dynamic investor community. Central to our offerings are proprietary indexes that observe emerging sectors, including biotech, clean energy, next-generation tech, medical devices and beyond. Visit us at prismmarketview.com and follow us on Twitter.

PRISM MarketView does not provide investment advice.

Media Contact

Company Name: Prism MarketView

Email: [email protected]

Phone: 646-863-6341

Website: https://prismmarketview.com

#press release#prism mediawire#stock market#investing#prismdigitalmedia#prismmarketview#healthcare#nasdaq#worldcancerday#biopharmaceuticals#Pharmaceutical

0 notes

Text

Innovations and Research in Oncology API Manufacturers in India

The fight against cancer is one of the most significant challenges in modern healthcare. Oncology, the branch of medicine dedicated to cancer treatment, relies heavily on Active Pharmaceutical Ingredients (APIs) to develop effective therapies. In India, a growing number of pharmaceutical companies are making remarkable strides in oncology API manufacturing, driving innovations and conducting groundbreaking research to develop more effective cancer treatments.

This article explores the innovations and research initiatives undertaken by oncology API manufacturers Indian, shedding light on their contributions to the global fight against cancer.

Cutting-Edge Innovations

Personalized Medicine: Indian oncology API manufacturers are at the forefront of the trend toward personalized cancer treatments. By utilizing advanced genomic and molecular techniques, they can develop APIs that target specific genetic mutations in patients' tumors. This precision medicine approach minimizes side effects and maximizes treatment effectiveness.

Biosimilars: The development of biosimilar APIs for cancer drugs has gained momentum in India. Biosimilars are highly similar versions of existing biologic medications, offering cost-effective alternatives for cancer patients. Indian manufacturers are investing in research to create biosimilar versions of essential oncology drugs, expanding access to treatment.

Immuno-Oncology APIs: The field of immuno-oncology has witnessed groundbreaking developments in recent years. Indian API manufacturers are actively engaged in the research and production of APIs that enhance the immune system's ability to target and destroy cancer cells. These innovations are changing the landscape of cancer therapy.

Nanotechnology in Drug Delivery: Nanotechnology is revolutionizing drug delivery, allowing APIs to target cancer cells more effectively while minimizing damage to healthy tissue. Indian researchers are exploring the potential of nanoscale drug carriers, known as nanomedicines, to improve the efficacy of oncology APIs.

Continuous Manufacturing: Continuous manufacturing processes are being adopted by Indian oncology API manufacturers, offering advantages in terms of cost efficiency and quality control. This innovation streamlines production and ensures a more consistent supply of essential cancer medications.

Research Initiatives

Clinical Trials and Drug Development: Indian pharmaceutical companies are actively involved in clinical trials for novel oncology APIs. These trials are essential for evaluating the safety and efficacy of new drugs and bringing them to market faster.

Collaborations with Global Partners: Indian oncology API manufacturers are collaborating with international pharmaceutical companies and research institutions to pool resources and expertise. These collaborations accelerate research and development efforts.

Targeted Therapies: Research efforts in India are focused on identifying new molecular targets for cancer therapies. This research can lead to the development of innovative APIs that specifically target cancer cells, improving treatment outcomes.

Drug Formulation and Delivery: Beyond APIs, Indian researchers are working on novel drug formulations and delivery systems. These innovations enhance drug stability, patient compliance, and treatment effectiveness.

Drug Resistance Studies: Understanding mechanisms of drug resistance in cancer is crucial for improving treatment outcomes. Indian researchers are conducting studies to decipher these mechanisms and develop APIs that can overcome drug resistance.

Challenges and Opportunities

While Indian oncology API manufacturers have made significant strides in innovations and research, they face challenges such as regulatory compliance, the need for substantial investment in research and development, and the global competition. However, several opportunities exist:

Global Demand: The global demand for affordable and high-quality cancer medications is on the rise. Indian manufacturers can tap into this growing market by producing innovative APIs and biosimilars.

Government Support: The Indian government has been supportive of the pharmaceutical industry. Incentives and policy initiatives encourage research and development, making it an attractive environment for API manufacturers.

Skilled Workforce: India boasts a highly skilled workforce in the pharmaceutical and healthcare sectors. This talent pool is a valuable asset for driving innovations and research.

Conclusion

Indian oncology API manufacturers are making significant contributions to the global fight against cancer through innovations and research. Their commitment to developing personalized medicines, biosimilars, immuno-oncology therapies, and more demonstrates their dedication to improving cancer treatment outcomes.

While challenges exist, the opportunities for growth and advancement in this critical field are substantial. As Indian companies continue to invest in research and development, the future of oncology API manufacturing in India looks promising, bringing hope to cancer patients worldwide.

0 notes

Text

India Immuno-Oncology Drugs Market Is Estimated To Witness High Growth Owing To Increasing Adoption of Immunotherapy

The India Immuno-Oncology Drugs Market is estimated to be valued at US$265 Mn in 2022 and is expected to exhibit a CAGR of 13.1% over the forecast period of 2021-2028, as highlighted in a new report published by Coherent Market Insights.

Market Overview:

The India Immuno-Oncology Drugs Market refers to the use of immunotherapy drugs for the treatment of various types of cancer. These drugs work by stimulating the body's immune system to recognize and attack cancer cells. The market is driven by the increasing adoption of immunotherapy drugs due to their effectiveness in treating cancer, especially in advanced stages. Immuno-oncology drugs offer advantages such as targeted therapy, reduced side effects compared to traditional chemotherapy, and improved survival rates. The need for these products arises from the growing prevalence of cancer in India and the need for more effective treatment options.

Market Key Trends:

One key trend in the India Immuno-Oncology Drugs Market is the development of combination therapies. Researchers and pharmaceutical companies are exploring the potential of combining immunotherapy drugs with other treatment modalities, such as chemotherapy or targeted therapy, to enhance their efficacy. For example, the combination of immune checkpoint inhibitors with chemotherapy has shown promising results in clinical trials for various types of cancers. This trend is driven by the need for more effective treatment options and the desire to improve patient outcomes.

PEST Analysis:

Political: The political factors impacting the India Immuno-Oncology Drugs Market include government regulations and policies related to drug approvals, pricing, and reimbursement. The regulatory framework plays a crucial role in determining the accessibility and affordability of these drugs.

Economic: Economic factors influencing the market include healthcare expenditure, insurance coverage, and affordability of immunotherapy drugs. The economic viability of these drugs is an important consideration for patients and healthcare providers.

Social: Social factors such as awareness about cancer and its treatment options, patient preferences, and cultural beliefs impact the adoption of immunotherapy drugs. Education campaigns and initiatives to raise awareness about cancer care can drive market growth.

Technological: Technological advancements in the field of immuno-oncology, such as the development of novel biomarkers and diagnostic tools, are driving the market. The integration of artificial intelligence and machine learning in cancer research and drug development also presents opportunities for market growth.

Key Takeaways:

1: The India Immuno-Oncology Drugs Market Demand is expected to witness high growth, exhibiting a CAGR of 13.1% over the forecast period. This growth is attributed to increasing adoption of immunotherapy in cancer treatment, driven by its effectiveness and advantages over traditional chemotherapy.

2: The fastest growing and dominating region in the India Immuno-Oncology Drugs Market is India due to the high prevalence of cancer and improving healthcare infrastructure. The country has a large patient population seeking advanced treatment options.

3: Key players operating in the India Immuno-Oncology Drugs Market include Amgen Inc., AstraZeneca Plc, Bristol-Myers Squibb, Celgene Corporation, Eli Lilly and Company, Merck & Co., F. Hoffmann-La Roche AG, Johnson & Johnson, Novartis International AG, and AbbVie Inc. These companies invest heavily in research and development to bring innovative immunotherapy drugs to the market.

In conclusion, the India Immuno-Oncology Drugs Market is poised to experience significant growth due to the increasing adoption of immunotherapy for cancer treatment. The development of combination therapies, along with favorable political, economic, social, and technological factors, further contribute to market expansion. Key players play a crucial role in driving innovation and bringing advanced therapies to cancer patients in India and globally.

#Immuno-Oncology Drugs Market#Immuno-Oncology Drugs Market Demand#Immuno-Oncology Drugs Market Insights#Immuno-Oncology Drugs Market Outlook#Immuno-Oncology Drugs Market Value#Immuno-Oncology Drugs Market Share#Immuno-Oncology Drugs Market Forecast#chemotherapy#antibodies#personalized medicine#cancer treatments#Cancer

0 notes

Text

0 notes

Text

Immuno Oncology Market: Empowering the Body to Fight Cancer

Introduction:

The field of cancer treatment has witnessed groundbreaking advancements over the years. Among these, Immuno Oncology (IO) Market has emerged as a revolutionary approach to combat cancer. This article delves into the realm of Immuno Oncology, exploring its mechanisms, current market players, trends, growth potential, challenges, regulatory landscape, and future prospects.

Understanding Immuno Oncology:

What is Immuno Oncology?

Immuno Oncology, also known as immunotherapy, is a specialized branch of cancer treatment that harnesses the body's immune system to recognize and attack cancer cells. Unlike traditional treatments like chemotherapy and radiation, IO stimulates the patient's immune response, helping it identify and eliminate cancer cells more effectively.

How does Immuno Oncology work?

IO treatments utilize various techniques to bolster the immune system. One of the key approaches involves using checkpoint inhibitors, which inhibit specific proteins that restrain the immune system, thereby allowing it to target cancer cells more efficiently.

The role of the immune system in cancer treatment:

The immune system plays a vital role in recognizing abnormal cells, including cancerous ones. However, cancer cells can develop strategies to evade the immune system. IO works to reverse this evasion, enabling the immune system to recognize and destroy cancer cells.

Key Players in the Immuno Oncology Market:

Pharmaceutical Companies:

Leading pharmaceutical companies have invested significantly in IO research and development. They are actively engaged in clinical trials and launching innovative IO therapies.

Biotechnology Firms:

Biotech companies are at the forefront of developing novel IO treatments. Their agility and focus on cutting-edge research have led to several promising advancements.

Research Institutions:

Academic and research institutions also play a crucial role in IO research. They contribute valuable insights and collaborate with industry players to drive progress.

Current Trends and Advancements:

Checkpoint Inhibitors:

Checkpoint inhibitors have revolutionized cancer treatment. They target specific proteins like PD-1 and CTLA-4, enhancing the immune system's ability to attack cancer cells.

CAR-T Cell Therapy:

CAR-T cell therapy involves modifying a patient's T-cells to express chimeric antigen receptors (CARs), enabling them to recognize and destroy cancer cells more effectively.

Cancer Vaccines:

Cancer vaccines are designed to stimulate the immune system to recognize and remember cancer cells, aiding in their elimination.

Adoptive Cell Transfer:

Adoptive cell transfer involves extracting, modifying, and reinfusing a patient's T-cells to boost their cancer-fighting capabilities.

Market Size and Growth Potential:

Global Immuno Oncology Market Size:

The IO market has experienced rapid growth in recent years, and it is projected to continue expanding at a substantial rate.

Factors driving market growth:

Increasing cancer prevalence, rising demand for effective and targeted therapies, and supportive government initiatives are fueling the growth of the IO market.

Future projections:

The IO market is poised for further growth, with ongoing research and development paving the way for groundbreaking treatments.

Challenges and Opportunities:

Managing Side Effects:

While IO treatments offer promising results, they can also cause immune-related side effects that need careful management.

Patient Access and Affordability:

Ensuring broad patient access to IO therapies and addressing cost concerns remain critical challenges.

Emerging Markets:

IO presents significant opportunities in emerging markets, where there is a rising demand for advanced cancer treatments.

Regulatory Landscape:

FDA Approval Process:

IO therapies undergo rigorous evaluation by regulatory authorities like the FDA to ensure safety and efficacy before approval.

Compliance and Safety:

Continuous monitoring of IO treatments is crucial to identify and address potential safety concerns.

International Regulations:

The IO market is subject to varying regulations across different countries, necessitating compliance with diverse standards.

Collaborations and Partnerships:

Industry-Academia Collaborations:

Collaborations between pharmaceutical companies and academic institutions foster innovation and knowledge exchange.

Cross-Industry Partnerships:

Partnerships between different industries can lead to innovative IO solutions and improved patient outcomes.

Future Outlook:

Innovations on the horizon:

Ongoing research holds the promise of introducing novel IO therapies with even higher efficacy.

Potential breakthroughs:

Combination therapies, personalized medicine, and targeting rare cancers are some areas that hold potential for significant breakthroughs.

Conclusion:

The Immuno Oncology market represents a transformative era in cancer treatment, where the body's own defense mechanisms are harnessed to fight the disease. With continuous advancements, collaborations, and regulatory support, the IO market is poised to offer new hope to cancer patients worldwide.

For more insights on the immuno-oncology market forecast, download a free report sample

0 notes

Text

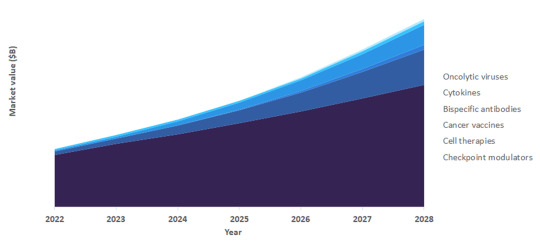

Immuno-oncology Clinical Trials Market Worth $15.1 Billion By 2028

The global immuno-oncology clinical trials market size is expected to reach USD 15.1 billion by 2028, according to a new report by Grand View Research, Inc. The market is expected to expand at a CAGR of 13.6% from 2021 to 2028. The rapidly growing field of Immuno-oncology has emerged as a novel therapeutic area within the oncology ecosystem, transforming the treatment of cancer.

From 2014 to…

View On WordPress

0 notes

Text

0 notes

Text

Using its unique expanded genetic code technology platform, Ambrx Biopharma Inc.(AMAM stock) , a clinical-stage biologics firm, discovers and creates tailored precision biologics. Its lead product candidate, ARX788, is an anti-HER2-drug conjugate (ADC) that is being studied in numerous clinical trials to treat of breast cancer, stomach junction cancer, as well as other solid tumors. These trials, which are currently in Phase 2 and Phase 3, are also being conducted for the treatment of gastric and breast cancers that have metastasized and are HER2-positive.

The company is also working on two earlier-stage product candidates: ARX305, an anti-CD70 ADC in investigational new chemical studies for the treatment of kidney cell carcinoma and other cancers. And ARX517, an anti-PSMA ADC in a Phase 1 clinical trial for the therapy of prostate cancer and other tumors.

It is also creating additional multiple product candidates with an eye toward immuno-oncology applications, such as ARX102, an immuno-oncology IL-2 path agonist that targets and gamma receptors on cytotoxic T cells to activate the patient's own immune system, and ARX822, a fab-small macromolecular bispecific that is used in preclinical phase for cancers. Bristol Myers Squibb Company, AbbVie Inc., BeiGene, Sino Biopharmaceutical Co., Ltd., NovoCodex, and Elanco Animal Health are all partners of Ambrx Biopharma Inc. The business was founded in 2003, and its main office is in La Jolla, California.

Who Are The Major Owners Of AMAM Stock?

17 investment banks and fund managers owned AMAM stock in Ambrx Biopharma over the previous two years. Fosun International Ltd ($37.88M), Adage Capital Partners GP L.L.C. ($17.37M), BlackRock Inc. ($11.75M), FMR LLC ($10.22M), Octagon Capital Advisors LP ($8.82M), Suvretta Capital Management LLC ($6.15M), and Millennium Management LLC ($2.82M) were the institutional investors with the largest investments.

AMAM stock is held by institutions 44.21% of the time. In the past 24 months, institutional investors have purchased 9,197,182 shares altogether. This volume of purchases entails about $158.86M in transactions.

In the past 24 months, investment banks have sold 274,909 shares in total. This share sale volume equates to roughly $1.55M in business. Institutional shareholders Cormorant Asset Management LP ($0.15M), BlackRock Inc. ($48.46K), Tudor Investment Corp Et Al ($39.86K), Ghisallo Capital Management LLC ($25K), and Renaissance Technologies LLC ($11.60K) all sold shares of Ambrx Biopharma in the past 24 months.

Short Sellers Of Ambrx Biopharma?

November saw a decrease in short interest in Ambrx Biopharma. 3,800 shares totaled short interest as of November 15th, which is a decrease of 20.8% from the 4,800 share total as of October 31st. The days-to-cover ratio is currently 0.1 days based on an average daily trading volume of 30,600 shares.

Short sales of the company's shares make up about 0.0% of the total. Any online trading account can be used to buy shares of AMAM stock. WeBull, Vanguard Brokerage Services, TD Ameritrade, E*TRADE, Robinhood, Fidelity, and Charles Schwab are a few well-known online brokerages providing access to the American stock market.

Competitors Of AMAM

The top rivals of Ambrx Biopharma include Elevation Oncology (ELEV), Cortexyme, Idera Pharmaceuticals (IDRA), Rubius Therapeutics (RUBY), Jasper Therapeutics (JSPR), Entera Bio (ENTX), AIM ImmunoTech (AIM), ERYTECH Pharma (ERYP), Genetic Technologies (GENE), Surrozen (SRZN), and (CRTX).

All of these businesses fall under the "medical" category. Ambrx Biopharma is not as well-liked by analysts as other Medical companies. AMAM stock has a consensus rating of Moderate Buy, whereas the typical consensus rating for healthcare firms is Buy.

Ambrx Biopharma is disliked by customers more than other Medical businesses. Ambrx Biopharma had an outperform vote from 52.38% of people, versus an average of 66.26% for medical firms.

Entera Bio And Ambrx Biopha

rma?

Compared to Ambrx Biopharma, Entera Bio has smaller revenue but larger earnings. Shares in Ambrx Biopharma are held by institutions 44.2% of the time. Comparatively, institutional investors own 17.1% of the shares in Entera Bio. Shares of Ambrx Biopharma are held by company insiders to a 5.1% stake. Comparatively, insiders own 5.2% of the shares in Entera Bio. Solid organizational ownership is a sign that endowments, hedge funds, and big money managers are betting on a company's long-term ability to outperform the market.

Compared to Entera Bio's profit income of -1,796.49%, Ambrx Biopharma has a net margin of 0.00%. Entera Bio's return on equity was beaten by Ambrx Biopharma's equity return of 0.00%. When compared by users, Entera Bio earned 157 more votes for outperformance than Ambrx Biopharma. Similarly, while just 52.38% of people gave Ambrx Biopharma an outstanding vote, 66.14% of users awarded Entera Bio an outperform rating.

With a beta of 1.34, AMAM stock price is 34% less volatile than that of the S&P 500. Compared to the S&P 500, Entera Bio's share price is 84% more unpredictable with a beta of 1.84. Ambrx Biopharma received 48 more media mentions than Entera Bio in the past week. Ambrx Biopharma received 49 mentions according to us, while Entera Bio received just one.

Shares Of Ambrx Rise After Promoting Early Safety

Preliminary safety and effectiveness findings from the Phase 2 ACE-Breast-03 study were released by Ambrx Biopharma Inc. (NASDAQ: AMAM), which encouraged early safety data from the breast cancer candidate.

In patients with HER2-positive mBC who are resistant or refractory to T-DM1, the data showed a 51.7% overall response rate (ORR) and a 100% disease control rate (DCR) after therapy with ARX788. Patients received therapy for a median of 7.2 months, as treatment is still ongoing.

In China, Amrbrx's partner NovoCodex Biopharmaceuticals is currently conducting two Phase 3 trials so one registration-enabled Phase 2 study with ARX788, with readouts expected in 2023. The last check Friday's premarket session saw AMAM shares up 180.6% to $1.15.

How Simple Is It For Ambrx Biopharma To Raise Money?

Many people may be thinking that Ambrx Biopharma has to raise more money in the future because its income is falling and its operating cash flow is rising. Companies have the option of raising capital through debt or equity.

Publicly traded corporations benefit greatly from the ability to sell investors shares in order to raise capital and finance expansion. By comparing a company's cash burn to its market capitalization, we may determine how much investors would be affected if the business had to issue capital to pay for the cash burn for an additional year.

Ambrx Biopharma seems to have a market value of $20 million and spent $7 million last year, or 350% of its market value. We believe there is a substantial risk of financial hardship given how big that expenditure is in comparison to the company's market value, and we would be extremely cautious about keeping the AMAM stock.

What Are The Average Rating And Price Objective For Ambrx Biopharma?

Based on the current 1 controlled transaction and 1 buy rating for AMAM, the consensus opinion for AMAM stock is Moderate Buy, according to the 2 analysts who have issued ratings in the past year. Ambrx Biopharma's average 12-month price objective is $4.00, with a premium price target of $4.00 and a low cost target of $4.00.

According to two Wall Street experts who have predicted the price of AMAM for the next year, the average price target is $11.00, with the maximum prediction for the company being $16.00 and the lowest prediction being $6.00.

By April 2023, according to the majority of Wall Street analysts, the share price of Ambrx Biopharma might be $11.00.

Is AMAM A Successful Business?

The cash burn for AMAM is $70163000. It has at least a year's worth of coverage in the form of cash and short-term investments. AMAM has cash and short-term investments of

$111.72 million. This is sufficient to fund its $70.16M yearly cash burn.

AMAM has a small 0.28 debt to equity ratio. On the balance sheet of AMAM, short-term assets outnumber long-term liabilities. On the balance sheet of AMAM, short-term assets exceed short-term liabilities. Cons: Over the past year, AMAM's profit margin has decreased from 325.6% to 1.729.9%.

According to our examination of Ambrx Biopharma's cash position, its cash runway was comforting, but the ratio of its cash burn to market value has us a little concerned. We have very little faith in the company's capacity to control its cash burn after taking all the data stated in this article into account, and we predict it will need additional money.

The Basics Of Ambrx Biopharma

The value of AMAM stock is 43, which is higher than the average for the Biotechnology sector. Currently, 3 out of 7 due diligence tasks are being passed by AMAM. AMAM's Financials rating is 0, which is the same as the industry average for the Biotechnology sector.

AMAM stock is presently failing 0 of 7 checks for due diligence. The AMAM stock forecast score is 0, which is the same as the sector average for biotechnology. AMAM stock is presently failing 0 of 9 checks for due diligence.

The Performance score for AMAM stock is 71, which is higher than the industry average for biotechnology. Five out of ten due diligence checks are passing for AMAM. We disregard this dimension because Ambrx Biopharma has little or no historical dividend history.

Recommendations Most Recent From AMAM Analysts

On May 24, 2022, a Goldman Sachs analyst decreases their price objective for AMAM stock from $6 to $4 while maintaining a hold rating.

On April 7, 2022, Joel Beatty, a high 17% analyst from Baird, commences covering on AMAM with a buy recommendation and publishes their $16.00 price target.

On February 28, 2022, Corinne Jenkins of Goldman Sachs, a top 48% analyst, announces the beginning of covering on AMAM with such a hold recommendation and a $6.00 price target.

In 2022, Should I Buy Or Sell Ambrx Biopharma Stock?

In the past year, Ambrx Biopharma has received "buy," "hold," and "sell" evaluations from 2 Wall Street research analysts. For the stock, there is presently 1 hold rating and 1 buy rating. Wall Street research experts generally agree that investors should "buy" AMAM stock. On Friday, June 18th 2021, (AMAM) raised $126 million through an initial public offering.

At a price of $17.00–$19.00 per share, the corporation issued 7,000,000 shares. The underwriters for the initial public offering were Goldman Sachs, BofA Securities, and Cowen. The time it would take for a corporation to exhaust its cash on hand at its current cash burn rate is known as its cash runway. Ambrx Biopharma had 111 million dollars in cash and no debt as of June 2022.

Looking back at the previous year, the business spent $70 million. So, starting in June 2022, AMAM stock forecast had a financial runway of about 19 months. This is not too bad, and unless cash burn substantially decreases, it is safe to assume the financial runway is coming to an end.

Ambrx Biopharma Stock Forecast 2022

While it is not anticipated that AMAM stock forecast annual earnings rate of growth of N/A will surpass the statistically important earnings growth rate of 9.29% for the US biotechnology industry, neither is it anticipated to surpass the average AMAM stock forecast earnings rate of growth of 70.08% for the US market.

The revenue for AMAM stock forecast in 2022 is -$90,558,000. One Wall Street analyst predicted that AMAM stock forecast earnings would be -$75,691,975 on average in 2022, with the highest AMAM earnings prediction being -$75,691,975 and the top AMAM stock forecast being -$75,691,975.

The current Earnings Per Share (EPS) for Ambrx Biopharma is $6.72. Analysts expect AMAM stock forecast EPS to be -$0.28 on average for 2022, with the lowest and highest estimates both coming in at -$0.28.

Ambrx Biopharma Stock Forecast

2023

AMAM stock forecast is anticipated to make -$67,582,121 in 2023, with the smallest earnings estimate being -$67,582,121 and the actual figure being -$67,582,121. By April 7, 2023, analysts on Wall Street believe the share price of Ambrx Biopharma might reach $11.00.

From the present share price of $4.54 for AMAM, the average AMAM stock forecast predicts a possible increase of 142.29%. AMAM stock forecast EPS is anticipated to be negative $0.25 in 2023.

0 notes

Text

Using its unique expanded genetic code technology platform, Ambrx Biopharma Inc.(AMAM stock) , a clinical-stage biologics firm, discovers and creates tailored precision biologics. Its lead product candidate, ARX788, is an anti-HER2-drug conjugate (ADC) that is being studied in numerous clinical trials to treat of breast cancer, stomach junction cancer, as well as other solid tumors. These trials, which are currently in Phase 2 and Phase 3, are also being conducted for the treatment of gastric and breast cancers that have metastasized and are HER2-positive.

The company is also working on two earlier-stage product candidates: ARX305, an anti-CD70 ADC in investigational new chemical studies for the treatment of kidney cell carcinoma and other cancers. And ARX517, an anti-PSMA ADC in a Phase 1 clinical trial for the therapy of prostate cancer and other tumors.

It is also creating additional multiple product candidates with an eye toward immuno-oncology applications, such as ARX102, an immuno-oncology IL-2 path agonist that targets and gamma receptors on cytotoxic T cells to activate the patient's own immune system, and ARX822, a fab-small macromolecular bispecific that is used in preclinical phase for cancers. Bristol Myers Squibb Company, AbbVie Inc., BeiGene, Sino Biopharmaceutical Co., Ltd., NovoCodex, and Elanco Animal Health are all partners of Ambrx Biopharma Inc. The business was founded in 2003, and its main office is in La Jolla, California.

Who Are The Major Owners Of AMAM Stock?

17 investment banks and fund managers owned AMAM stock in Ambrx Biopharma over the previous two years. Fosun International Ltd ($37.88M), Adage Capital Partners GP L.L.C. ($17.37M), BlackRock Inc. ($11.75M), FMR LLC ($10.22M), Octagon Capital Advisors LP ($8.82M), Suvretta Capital Management LLC ($6.15M), and Millennium Management LLC ($2.82M) were the institutional investors with the largest investments.

AMAM stock is held by institutions 44.21% of the time. In the past 24 months, institutional investors have purchased 9,197,182 shares altogether. This volume of purchases entails about $158.86M in transactions.

In the past 24 months, investment banks have sold 274,909 shares in total. This share sale volume equates to roughly $1.55M in business. Institutional shareholders Cormorant Asset Management LP ($0.15M), BlackRock Inc. ($48.46K), Tudor Investment Corp Et Al ($39.86K), Ghisallo Capital Management LLC ($25K), and Renaissance Technologies LLC ($11.60K) all sold shares of Ambrx Biopharma in the past 24 months.

Short Sellers Of Ambrx Biopharma?

November saw a decrease in short interest in Ambrx Biopharma. 3,800 shares totaled short interest as of November 15th, which is a decrease of 20.8% from the 4,800 share total as of October 31st. The days-to-cover ratio is currently 0.1 days based on an average daily trading volume of 30,600 shares.

Short sales of the company's shares make up about 0.0% of the total. Any online trading account can be used to buy shares of AMAM stock. WeBull, Vanguard Brokerage Services, TD Ameritrade, E*TRADE, Robinhood, Fidelity, and Charles Schwab are a few well-known online brokerages providing access to the American stock market.

Competitors Of AMAM

The top rivals of Ambrx Biopharma include Elevation Oncology (ELEV), Cortexyme, Idera Pharmaceuticals (IDRA), Rubius Therapeutics (RUBY), Jasper Therapeutics (JSPR), Entera Bio (ENTX), AIM ImmunoTech (AIM), ERYTECH Pharma (ERYP), Genetic Technologies (GENE), Surrozen (SRZN), and (CRTX).

All of these businesses fall under the "medical" category. Ambrx Biopharma is not as well-liked by analysts as other Medical companies. AMAM stock has a consensus rating of Moderate Buy, whereas the typical consensus rating for healthcare firms is Buy.

Ambrx Biopharma is disliked by customers more than other Medical businesses. Ambrx Biopharma had an outperform vote from 52.38% of people, versus an average of 66.26% for medical firms.

Entera Bio And Ambrx Biopha

rma?

Compared to Ambrx Biopharma, Entera Bio has smaller revenue but larger earnings. Shares in Ambrx Biopharma are held by institutions 44.2% of the time. Comparatively, institutional investors own 17.1% of the shares in Entera Bio. Shares of Ambrx Biopharma are held by company insiders to a 5.1% stake. Comparatively, insiders own 5.2% of the shares in Entera Bio. Solid organizational ownership is a sign that endowments, hedge funds, and big money managers are betting on a company's long-term ability to outperform the market.

Compared to Entera Bio's profit income of -1,796.49%, Ambrx Biopharma has a net margin of 0.00%. Entera Bio's return on equity was beaten by Ambrx Biopharma's equity return of 0.00%. When compared by users, Entera Bio earned 157 more votes for outperformance than Ambrx Biopharma. Similarly, while just 52.38% of people gave Ambrx Biopharma an outstanding vote, 66.14% of users awarded Entera Bio an outperform rating.

With a beta of 1.34, AMAM stock price is 34% less volatile than that of the S&P 500. Compared to the S&P 500, Entera Bio's share price is 84% more unpredictable with a beta of 1.84. Ambrx Biopharma received 48 more media mentions than Entera Bio in the past week. Ambrx Biopharma received 49 mentions according to us, while Entera Bio received just one.

Shares Of Ambrx Rise After Promoting Early Safety

Preliminary safety and effectiveness findings from the Phase 2 ACE-Breast-03 study were released by Ambrx Biopharma Inc. (NASDAQ: AMAM), which encouraged early safety data from the breast cancer candidate.

In patients with HER2-positive mBC who are resistant or refractory to T-DM1, the data showed a 51.7% overall response rate (ORR) and a 100% disease control rate (DCR) after therapy with ARX788. Patients received therapy for a median of 7.2 months, as treatment is still ongoing.

In China, Amrbrx's partner NovoCodex Biopharmaceuticals is currently conducting two Phase 3 trials so one registration-enabled Phase 2 study with ARX788, with readouts expected in 2023. The last check Friday's premarket session saw AMAM shares up 180.6% to $1.15.

How Simple Is It For Ambrx Biopharma To Raise Money?

Many people may be thinking that Ambrx Biopharma has to raise more money in the future because its income is falling and its operating cash flow is rising. Companies have the option of raising capital through debt or equity.

Publicly traded corporations benefit greatly from the ability to sell investors shares in order to raise capital and finance expansion. By comparing a company's cash burn to its market capitalization, we may determine how much investors would be affected if the business had to issue capital to pay for the cash burn for an additional year.

Ambrx Biopharma seems to have a market value of $20 million and spent $7 million last year, or 350% of its market value. We believe there is a substantial risk of financial hardship given how big that expenditure is in comparison to the company's market value, and we would be extremely cautious about keeping the AMAM stock.

What Are The Average Rating And Price Objective For Ambrx Biopharma?

Based on the current 1 controlled transaction and 1 buy rating for AMAM, the consensus opinion for AMAM stock is Moderate Buy, according to the 2 analysts who have issued ratings in the past year. Ambrx Biopharma's average 12-month price objective is $4.00, with a premium price target of $4.00 and a low cost target of $4.00.

According to two Wall Street experts who have predicted the price of AMAM for the next year, the average price target is $11.00, with the maximum prediction for the company being $16.00 and the lowest prediction being $6.00.

By April 2023, according to the majority of Wall Street analysts, the share price of Ambrx Biopharma might be $11.00.

Is AMAM A Successful Business?

The cash burn for AMAM is $70163000. It has at least a year's worth of coverage in the form of cash and short-term investments. AMAM has cash and short-term investments of

$111.72 million. This is sufficient to fund its $70.16M yearly cash burn.

AMAM has a small 0.28 debt to equity ratio. On the balance sheet of AMAM, short-term assets outnumber long-term liabilities. On the balance sheet of AMAM, short-term assets exceed short-term liabilities. Cons: Over the past year, AMAM's profit margin has decreased from 325.6% to 1.729.9%.

According to our examination of Ambrx Biopharma's cash position, its cash runway was comforting, but the ratio of its cash burn to market value has us a little concerned. We have very little faith in the company's capacity to control its cash burn after taking all the data stated in this article into account, and we predict it will need additional money.

The Basics Of Ambrx Biopharma

The value of AMAM stock is 43, which is higher than the average for the Biotechnology sector. Currently, 3 out of 7 due diligence tasks are being passed by AMAM. AMAM's Financials rating is 0, which is the same as the industry average for the Biotechnology sector.

AMAM stock is presently failing 0 of 7 checks for due diligence. The AMAM stock forecast score is 0, which is the same as the sector average for biotechnology. AMAM stock is presently failing 0 of 9 checks for due diligence.

The Performance score for AMAM stock is 71, which is higher than the industry average for biotechnology. Five out of ten due diligence checks are passing for AMAM. We disregard this dimension because Ambrx Biopharma has little or no historical dividend history.

Recommendations Most Recent From AMAM Analysts

On May 24, 2022, a Goldman Sachs analyst decreases their price objective for AMAM stock from $6 to $4 while maintaining a hold rating.

On April 7, 2022, Joel Beatty, a high 17% analyst from Baird, commences covering on AMAM with a buy recommendation and publishes their $16.00 price target.

On February 28, 2022, Corinne Jenkins of Goldman Sachs, a top 48% analyst, announces the beginning of covering on AMAM with such a hold recommendation and a $6.00 price target.

In 2022, Should I Buy Or Sell Ambrx Biopharma Stock?

In the past year, Ambrx Biopharma has received "buy," "hold," and "sell" evaluations from 2 Wall Street research analysts. For the stock, there is presently 1 hold rating and 1 buy rating. Wall Street research experts generally agree that investors should "buy" AMAM stock. On Friday, June 18th 2021, (AMAM) raised $126 million through an initial public offering.

At a price of $17.00–$19.00 per share, the corporation issued 7,000,000 shares. The underwriters for the initial public offering were Goldman Sachs, BofA Securities, and Cowen. The time it would take for a corporation to exhaust its cash on hand at its current cash burn rate is known as its cash runway. Ambrx Biopharma had 111 million dollars in cash and no debt as of June 2022.

Looking back at the previous year, the business spent $70 million. So, starting in June 2022, AMAM stock forecast had a financial runway of about 19 months. This is not too bad, and unless cash burn substantially decreases, it is safe to assume the financial runway is coming to an end.

Ambrx Biopharma Stock Forecast 2022

While it is not anticipated that AMAM stock forecast annual earnings rate of growth of N/A will surpass the statistically important earnings growth rate of 9.29% for the US biotechnology industry, neither is it anticipated to surpass the average AMAM stock forecast earnings rate of growth of 70.08% for the US market.

The revenue for AMAM stock forecast in 2022 is -$90,558,000. One Wall Street analyst predicted that AMAM stock forecast earnings would be -$75,691,975 on average in 2022, with the highest AMAM earnings prediction being -$75,691,975 and the top AMAM stock forecast being -$75,691,975.

The current Earnings Per Share (EPS) for Ambrx Biopharma is $6.72. Analysts expect AMAM stock forecast EPS to be -$0.28 on average for 2022, with the lowest and highest estimates both coming in at -$0.28.

Ambrx Biopharma Stock Forecast

2023

AMAM stock forecast is anticipated to make -$67,582,121 in 2023, with the smallest earnings estimate being -$67,582,121 and the actual figure being -$67,582,121. By April 7, 2023, analysts on Wall Street believe the share price of Ambrx Biopharma might reach $11.00.

From the present share price of $4.54 for AMAM, the average AMAM stock forecast predicts a possible increase of 142.29%. AMAM stock forecast EPS is anticipated to be negative $0.25 in 2023.

0 notes

Text

Immuno-Oncology Assay Market Competition from Opponents, Dynamics, Demand and Risk to 20231

Market Overview

The global immune-oncology assay market was valued at USD 4.2 billion in 2021 and it is anticipated to grow further up to USD 14.1 billion by 2031, at a CAGR of 12.9% during the forecast period.

One kind of immunoassay that is mostly used to diagnose cancer is the immuno-oncology assay. It is a process that profiles different analytes by simultaneously detecting and measuring them, including proteins, biomolecules, growth factors, cytokines, and chemokines. This method primarily targets and eliminates cancer cells using the body’s natural defensive mechanism. This assay is used for in vitro research to investigate the complex tumor microenvironment, the dynamic interactions between cancer cells and immune cells, and the perception of immunoreactivity in a variety of cell-based assays to determine the mode of action.

View Detailed Report Description: https://www.globalinsightservices.com/reports/immuno-oncology-assays-market/

Market Dynamics

As a multi-stage carcinogenesis process involving numerous molecular pathway events, cancer is a complex illness that arises. So, the diagnosis, prognosis, and treatment of cancer are all accompanied with a number of challenges. In this aspect, a single marker is not useful due to the complexity of cancer. Each cancer also differs from other cancer kinds in terms of its molecular profile. As a result, the use of immuno-oncology assays has proved crucial for comprehending cancer signatures and creating individualized treatments. Over the past few years, cancer has become more commonplace across the globe. In 2018, there were 9.6 million fatalities due to cancer, which has overtaken all other causes of mortality in the world. GLOBOCAN predicts that by 2040, there would be over 30 million new instances of cancer, up from 18 million in 2018. Africa, Asia, Central and South America account for more than 60% of all new cancer cases, and these regions also account for 70% of all cancer-related fatalities worldwide. As a result, there is a need for considerable research to be done for cancer detection and therapy, and immuno-oncology assays play a significant role in this study.

The discovery, development, and validation of biomarkers demand large capital expenditures. Additionally, diagnostic manufacturers have major financial difficulties as a result of the high drug attrition in clinical trials (with about 30% of medications failing in Phase III). In order for manufacturers to receive regulatory permission for in vitro diagnostics (IVD), Phase III clinical trials that rely on reliable biomarker tests must be successful. The cost of conducting clinical trials and meeting onerous regulatory criteria severely limits innovation and makes it difficult for small businesses to develop biomarkers. As a result, in addition to the high capital expenditures, the low cost-benefit ratio is impeding the expansion of the market for immuno-oncology assays for biomarker identification.

Get Free Sample Copy of This Report: https://www.globalinsightservices.com/request-sample/GIS10299

The key players studied in the market are Thermo Fisher Scientific, Inc. (US), F. Hoffmann-La Roche Ltd. (Switzerland), Agilent Technologies, Inc. (US), Illumina, Inc. (US), NanoString Technologies, Inc. (US), Sartorius AG (Germany), HTG Molecular Diagnostics, Inc. (US), QIAGEN N.V. (Netherlands), Merck Millipore (US), PerkinElmer, Inc. (US), Abbott Laboratories, Inc. (US), Guardant Health, Inc. (US), and bioMérieux SA (France) among others.

About Global Insight Services:

Global Insight Services (GIS) is a leading multi-industry market research firm headquartered in Delaware, US. We are committed to providing our clients with highest quality data, analysis, and tools to meet all their market research needs. With GIS, you can be assured of the quality of the deliverables, robust & transparent research methodology, and superior service.

Contact Us:

Global Insight Services LLC

16192, Coastal Highway, Lewes DE 19958

E-mail: [email protected]

Phone: +1–833–761–1700

0 notes

Last Seen Blogs

noyeshr

NOYES

exposingryanmondoley

Take Down Rapists and Abusers

virgenmaria

Sin título

realifedreamgirl

Real Life Bombshell