#Hydraulic Motor Market Growth

Text

#Hydraulic Motor Market COVID-19 Analysis Report#Hydraulic Motor Market Demand Outlook#Hydraulic Motor Market Primary Research#Hydraulic Motor Market Size and Growth#Hydraulic Motor Market Trends#Hydraulic Motor Market#global Hydraulic Motor market by Application#global Hydraulic Motor Market by rising trends#Hydraulic Motor Market Development#Hydraulic Motor market Future#Hydraulic Motor Market Growth#Hydraulic Motor market in Key Countries#Hydraulic Motor Market Latest Report#Hydraulic Motor market SWOT analysis#Hydraulic Motor market Top Manufacturers#Hydraulic Motor Sales market#Hydraulic Motor Market COVID-19 Impact Analysis Report#Hydraulic Motor Market Primary and Secondary Research#Hydraulic Motor Market Size#Hydraulic Motor Market Share#Hydraulic Motor Market Research Analysis#Hydraulic Motor Market Trends and Outlook#Hydraulic Motor Industry Analysis

1 note

·

View note

Text

#Hydraulic Motor Market COVID-19 Analysis Report#Hydraulic Motor Market Demand Outlook#Hydraulic Motor Market Primary Research#Hydraulic Motor Market Size and Growth#Hydraulic Motor Market Trends#Hydraulic Motor Market#global Hydraulic Motor market by Application#global Hydraulic Motor Market by rising trends#Hydraulic Motor Market Development#Hydraulic Motor market Future#Hydraulic Motor Market Growth#Hydraulic Motor market in Key Countries#Hydraulic Motor Market Latest Report#Hydraulic Motor market SWOT analysis#Hydraulic Motor market Top Manufacturers#Hydraulic Motor Sales market#Hydraulic Motor Market COVID-19 Impact Analysis Report#Hydraulic Motor Market Primary and Secondary Research#Hydraulic Motor Market Size#Hydraulic Motor Market Share#Hydraulic Motor Market Research Analysis#Hydraulic Motor Market Trends and Outlook#Hydraulic Motor Industry Analysis

0 notes

Text

#Global Hydraulic Power Motor Market Size#Share#Trends#Growth#Industry Analysis#Key Players#Revenue#Future Development & Forecast

0 notes

Text

Power Tools Market Demand, Supply, Growth Factors, Latest Rising Trends and Forecast to 2031

Power tools are a class of tools and mechanical devices that operate when a secondary power source and mechanism are activated rather than being operated manually. Electric motors and compressed or internal combustion engines are examples of this. From hand-held machine drills to hydraulic presses and pneumatic equipment, power tools cover a wide range of applications. Power tools can be used for a variety of tasks, including home chores, construction, and gardening. The key drivers of the power tool markets include increasing demand from the industrial sector, increasing demand from the professional segment, and increasing use of power tools for DIY and domestic activities. Power tools also have applications across various verticals.

0 notes

Text

0 notes

Text

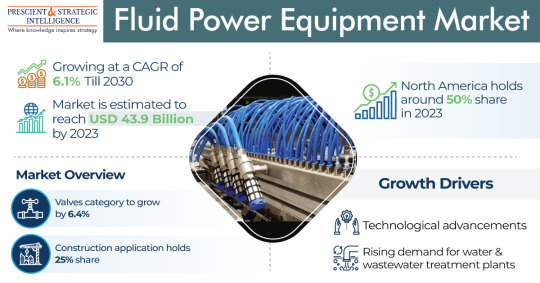

Fluid Power Equipment Market Will Touch USD 66.0 Billion in 2030

The fluid power equipment market was USD 43.9 billion in 2023, which will rise to USD 66.0 billion, advancing at a 6.1% compound annual growth rate, by 2030.

The growth of this industry is mainly because of the increasing need for water and wastewater treatment plants, and the continuous technological developments.

In 2023, hydraulic led the type category, with a revenue of USD 26.3 billion. This can be ascribed to the cost-effectiveness and high efficiency of this type, and its extensive adoption in oil & gas and construction applications.

The pneumatic category, on the other hand, will propel at a healthy rate during this decade. This is because these systems rely on compressed air pressure to send power and are extensively employed in numerous industrial applications.

Furthermore, pneumatic valves are available in different designs, sizes, and configurations, and thus, allow free flow in a single direction and avoid flow in the opposite direction.

In 2023, the construction category, based on end user, was the largest contributor to the fluid power equipment market, with a 25% share. This can be because of the high usefulness of these components in various applications like material demolition or handling in the construction sector.

The automotive category, on the other hand, is advancing at a tremendous rate, because of the increasing customer's disposable salary, along with the increasing standards of living, worldwide.

Motors is leading the component category. This can be because motor components provide great torque & power, and are extensively employed across various sectors, including agriculture, construction, and automotive.

Moreover, the developments in motor technologies enhance their performance and efficiency, and thus, are cost-effective solutions for businesses to utilize for different applications.

On the other hand, the valves category will advance at the highest rate during this decade. This is ascribed to the growing requirement for valves to track high pressure, which will boost the demand for valve components.

North America led the industry in 2023, with a 50% share. This can be attributed to the existence of greater infrastructure, coupled with the rising progression in R&D and manufacturing activities.

Moreover, the increasing count of initiatives implemented to guarantee the worker's safety in oil & gas and chemicals sectors further boost the regional industry growth.

APAC will propel at the highest rate, of 6.5%, in the coming years. This will be because of the surging urbanized populace along with the increasing requirement for energy, and the progression of the construction and automobile sectors in Japan, China, and India.

With the rise in the requirement for water & wastewater treatment plants, the fluid power equipment industry will continuously progress in the coming years.

Source: P&S Intelligence

#Fluid Power Equipment Market Share#Fluid Power Equipment Market Size#Fluid Power Equipment Market Growth#Fluid Power Equipment Market Applications#Fluid Power Equipment Market Trends

1 note

·

View note

Text

Robot Tool Changers Market Recent Developments Study Analysis By 2033

A Robot Tool Changer (RTC) is a device used to quickly and easily change the tool or end-effector attached to a robot arm. This allows the robot to perform multiple tasks without the need to stop and change tools manually.

RTCs typically consist of two parts: a gripper that attaches to the robot arm and a tool-changing mechanism that is mounted on the robot. The gripper is opened and closed using a pneumatic or hydraulic cylinder, and the tool-changing mechanism is operated using an electric motor.

RTCs can be used with a variety of different robot types, including articulated, SCARA, and delta robots. They are often used in applications where the robot needs to perform multiple tasks, such as pick-and-place, welding, and assembly. For example, a robot that assembles cars might need to change its tool from a screwdriver to a wrench.

To Know More: https://www.globalinsightservices.com/reports/robot-tool-changers-market/?utm_id=Snehalkast

Market Outlook

In the current market scenario, there are various factors which are driving the growth of Robot Tool Changers market. Some of the key drivers are as follows:

Increasing demand for automation in various industries: With the increasing competition and need for efficiency and accuracy, there is a growing demand for automation in various industries such as automotive, food & beverage, pharmaceuticals, etc. This is one of the key drivers for the growth of Robot Tool Changers market as these devices help in increasing the productivity and efficiency of the manufacturing process.

Rising labor costs: The rising labor costs across the globe is another key driver for the growth of Robot Tool Changers market. These devices help in reducing the dependence on manual labor, thus leading to lower production costs.

Increasing adoption of collaborative robots: Collaborative robots are becoming increasingly popular in various industries as they offer several advantages over traditional robots such as being safe to work with, easy to program and operate, and cost-effective. This is leading to the increasing adoption of collaborative robots which in turn is driving the growth of Robot Tool Changers market.

Request Sample: https://www.globalinsightservices.com/request-sample/GIS10229/?utm_id=Snehalkast

Major Players

Some of the key players of Robot Tool Changers Market are ATI Industrial Automation Inc. (US), SCHUNK GmbH & Co. KG (Germany), Applied Robotics Inc. (US), Nitta Corporation (Japan), Carl Kurt Walther GmbH & Co. KG (Germany), DESTACO (US), Stäubli International AG (Switzerland), A Dover Company (US), American Grippers Inc (US), and PTM Präzisionstechnik GmbH (Germany).

0 notes

Text

Soaring High: Exploring Crane Manufacturers in India

In the bustling landscape of India's construction and industrial sectors, cranes stand as towering symbols of progress and efficiency. Let's take a closer look at some of the prominent crane manufacturers shaping India's skyline, including the renowned Indef brand.

1. TIL Limited (formerly Tata Motors): TIL Limited boasts a rich legacy of over 70 years in crane manufacturing. Renowned for its engineering excellence and innovative solutions, TIL offers a comprehensive range of cranes, including mobile, tower, and crawler variants. With a commitment to quality and customer satisfaction, TIL has established itself as a leader in the Indian crane industry.

2. ACE Cranes: ACE Cranes has emerged as a key player in India's crane manufacturing sector since its establishment in 1995. The company's focus on indigenous technology and customization has set it apart in the market. ACE's product portfolio includes hydraulic cranes, pick-n-carry cranes, and tower cranes, catering to diverse customer requirements with efficiency and reliability.

3. Escort Group: With a strong presence in the heavy engineering sector, Escort Group has made significant contributions to crane manufacturing in India. The company offers a range of cranes, including rough terrain and truck-mounted variants, known for their robustness and performance. Escort's cranes find applications in construction, infrastructure, and mining projects nationwide.

4. Indef: Indef, a leading name in the Indian crane industry, is renowned for its cutting-edge technology and superior quality. Specializing in material handling solutions, Indef offers a wide array of cranes, hoists, and lifting equipment tailored to meet the specific needs of various industries. The brand's commitment to innovation and reliability has earned it a loyal customer base across India.

5. Innovation and Global Reach: Indian crane manufacturers are embracing innovation to enhance efficiency, safety, and sustainability in crane operations. Technologies such as IoT and automation are being integrated to streamline processes and improve productivity. Furthermore, Indian cranes are gaining acceptance in international markets, contributing to the country's reputation as a hub for engineering excellence.

6. Challenges and Opportunities: While the Indian crane industry holds immense potential for growth, it also faces challenges such as regulatory complexities and skilled labor shortages. However, these challenges present opportunities for innovation and collaboration. By leveraging technology and fostering skill development initiatives, manufacturers can overcome hurdles and drive sustainable growth.

7. Conclusion: In conclusion, crane manufacturers in India play a crucial role in the nation's development journey. With a blend of indigenous innovation, global best practices, and a commitment to quality, these companies are shaping India's infrastructure landscape and making their mark on the global stage.

As India continues to progress towards its vision of economic prosperity, the towering presence of cranes serves as a testament to the country's engineering prowess and determination.

0 notes

Text

Precision Planting Market Size & Share, Growth Report 2032

The global precision planting market is projected to reach USD 8.2 billion by 2027 from USD 5.0 billion in 2022; it is expected to grow at a CAGR of 10.3%.

Some of the Key factors propelling the market growth includes the substantial cost-savings associated with precision planting and seeding equipment, surge in the adoption of advanced technologies in precision agriculture to reduce labor cost, and increasing promotion of precision planting techniques by governments worldwide. Moreover, climate change and need to meet rising demand for food, and focus on integration of geo-mapping and sensor data with planting equipment will drive the growth of the industry in the near future.

Key players in the precision planting market include Deere & Company (US), Trimble Inc. (US), CNH Industrial N.V. (UK), Kinze Manufacturing Inc. (US), and Precision Planting (brand of AGCO) (US). Other players include Topcon Positioning Systems (US), Buhler Industries Inc. (CA), Vaderstad Industries Inc. (CA), Stara S/A (Brazil), Kasco Manufacturing Inc. (US), Davimac Group (Australia), Morris Industries Ltd. (CA), SeedMaster Manufacturing Ltd. (CA), The Climate Corporation (US), Ag Leader Technology (US), Bourgault Industries Ltd. (CA), DroneSeed (US), Dendra Systems (UK), Kubota Corporation (Japan), Hexagon Agriculture (Brazil), Dickey-John Corporation (US), Monosem (France), and White Planters (brand of AGCO) (US).

Download PDF Brochure:

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=96394217

Row crops application to account for a larger share of the precision planting market during the forecast period.

The precision planting market is likely to be dominated by row crops in 2023. In row crops, precision planting equipment and systems are widely used to distribute seeds precisely. For large farms, precision planting systems are mainly used to plant row crops. The singulation of seeds affects the yield of row crops such as corn, soybeans, and canola. The majority of these crops are sown on farms sized above 400 hectares, which are primarily found in the US, Canada, Argentina, Brazil, and Australia.

Farms below 400 ha will hold the largest market share during the forecast period

In Europe, Asia Pacific, and Africa, farms smaller than 400 hectares are common. Globally, there are more than 80 million farms between 100 and 400 hectares. These farms are more likely to use compact precision planting systems due to their benefits, such as high productivity due to precise seed inputs, superior seed-to-soil contact, and the ability to plant thousands of seeds per minute. A considerable amount of disposable income is available to these farmers, so they can invest in technologically advanced planting devices and equipment. Farms with a size less than 400 hectares also find high adoption of precision air seeders.

Hydraulic drive segment is likely to account for a larger share in the overall precision planting market from 2022 to 2027

As a result of its advanced features and ability to allow growers to reduce overlap between seeds, hydraulic drives are expected to hold a larger market share. Planters and seeders with an advanced drive system come with either an electric or hydraulic motor. Increasing adoption of high-speed precision planters and precision air seeders, as well as growing awareness of the benefits of precision planting systems, have contributed to the growth of hydraulic drive-based precision planting systems. The growing preference for high-speed precision planting systems with hydraulic drives to reduce manual labor and achieve cost savings has led to the growth of high-speed precision planting systems.

US likely to lead the global precision planting market by 2027

The US has a substantial market share in precision planting and seeding equipment markets. The country has large area for crops under cultivation; every year, more than 90 million ha are planted with row crops such as corn and soybean. High-speed precision planters are mainly used in commodity row crops in the US. The adoption rate of automation and digitalization of agriculture is high in large farms, which further allows farmers in the country to make use of modern and precise equipment for agriculture. To produce various types of row crops, farmers practice conventional tillage and soil preparation, which involve several steps, including preparing the soil bed and eliminating the weeds.

0 notes

Text

Segmenting the Power Tools Market: Strategies for Targeted Marketing Campaigns

Power Tools Market Overview:

In 2021, the power tools market was estimated to be worth USD 44.6 billion. According to projections, the power tools market will expand at a compound annual growth rate (CAGR) of 5.9% from USD 47.23 billion in 2022 to USD 73.8 billion by 2030.

Power tools play a pivotal role across various industries, providing efficiency, precision, and productivity in tasks ranging from construction and manufacturing to woodworking and DIY projects. The global power tools market has witnessed substantial growth driven by technological advancements, industrial automation, and increasing demand for high-performance tools. This article provides an in-depth overview of the power tools market, including segmentation analysis, key takeaways, and regional insights.

For latest news and updates, request a free sample report of Power Tools Market

By Segmentation:

1. Product Type:

a. Electric Power Tools: This segment includes corded and cordless electric tools such as drills, saws, sanders, grinders, and routers, powered by electricity for versatile and efficient operation.

b. Pneumatic Power Tools: Pneumatic or air-powered tools utilize compressed air to drive mechanisms such as impact wrenches, nail guns, and sanders, offering high power-to-weight ratios and durability in industrial applications.

c. Hydraulic Power Tools: Hydraulic tools use hydraulic fluid to generate power for tasks such as cutting, bending, and pressing, commonly found in heavy-duty construction, automotive, and manufacturing operations.

2. End-User:

a. Construction: Power tools are indispensable in construction activities, including drilling, cutting, fastening, and finishing tasks, contributing to efficiency, accuracy, and safety on construction sites.

b. Manufacturing: Industries such as automotive, aerospace, electronics, and metal fabrication rely on power tools for precision machining, assembly, and surface finishing processes, enhancing productivity and product quality.

c. Woodworking: Woodworkers and carpenters utilize a wide range of power tools such as saws, routers, planers, and sanders to craft furniture, cabinets, and other wooden products with speed and precision.

d. DIY Enthusiasts: Homeowners and hobbyists use power tools for various do-it-yourself projects, renovations, and repairs, driving demand for compact, user-friendly tools with advanced features.

3. Region:

The global power tools market is segmented into key regions, including North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Each region exhibits distinct market dynamics influenced by factors such as industrialization, infrastructure development, technological adoption, and regulatory environment.

Key Takeaways:

1. Technological Advancements: Continuous innovation in power tool design, materials, and functionality, including brushless motors, lithium-ion batteries, and digital controls, enhances performance, durability, and user experience.

2. Industry 4.0 Integration: The convergence of power tools with digital technologies such as IoT (Internet of Things), AI (Artificial Intelligence), and cloud connectivity enables remote monitoring, predictive maintenance, and data-driven insights, optimizing operational efficiency and uptime.

3. Safety and Ergonomics: Manufacturers prioritize safety features and ergonomic designs in power tools to minimize user fatigue, reduce the risk of accidents and injuries, and enhance overall user comfort and productivity.

4. Market Expansion in Emerging Economies: Rapid urbanization, infrastructure development, and industrialization in emerging markets such as China, India, and Southeast Asia drive the demand for power tools, presenting growth opportunities for market players to expand their presence and product offerings.

Regional Insights:

1. North America: The United States and Canada lead the North American power tools market, driven by robust construction and manufacturing sectors, technological innovation, and a strong DIY culture.

2. Europe: Germany, the UK, and France are key markets in Europe, characterized by stringent safety regulations, emphasis on sustainability, and growing adoption of smart and connected power tools.

3. Asia Pacific: China, Japan, and India dominate the Asia Pacific market, fueled by rapid industrialization, urbanization, infrastructure investments, and increasing demand for high-quality power tools in manufacturing and construction sectors.

4. Latin America and the Middle East & Africa: These regions offer growth opportunities due to expanding construction activities, infrastructure projects, and investments in industrial development, driving demand for power tools and related equipment.

The power tools market continues to evolve with advancements in technology, changing end-user preferences, and evolving industry trends. Manufacturers, suppliers, and distributors need to adapt to these dynamics, focusing on innovation, safety, and market expansion to capitalize on growth opportunities globally. By understanding regional nuances and catering to diverse end-user needs, stakeholders can navigate the competitive landscape and drive sustainable growth in the dynamic power tools market.

Top trending report:

HVAC System Market

Industrial Hand Gloves Market

Water Purifier Market

Agriculture Equipment Market

Power Tools Market

0 notes

Text

Superconducting Magnets Market's Boundless Growth Beyond 2023 through Exhaustive Research

Cylindrical grinders are precision machining tools used to shape the outer surface of a workpiece. They are commonly used in manufacturing and metalworking industries to achieve high levels of accuracy and surface finish on cylindrical or tapered surfaces. The primary function of a cylindrical grinder is to remove material from the workpiece to create the desired shape and dimensions.

Here are some key features and components of cylindrical grinders:

Workpiece: The workpiece is the object being machined on the cylindrical grinder. It can be made of various materials such as metal, plastic, or ceramics. The workpiece is mounted on the grinder and rotates while being processed.

Request For Sample Report: Elevate Your Industry Intelligence with Actionable Insights

https://www.futuremarketinsights.com/reports/sample/rep-gb-17217

Grinding Wheel: The grinding wheel is a rotating abrasive wheel that removes material from the workpiece. It is typically made of abrasive particles bonded together in a specific shape and hardness. The grinding wheel can be adjusted for different diameters and surface finishes.

Wheelhead: The wheelhead is the part of the cylindrical grinder that houses the grinding wheel. It can be moved horizontally and vertically to position the grinding wheel accurately on the workpiece. The wheelhead can also rotate to perform external or internal grinding operations.

Workhead: The workhead holds the workpiece and provides rotational movement. It can be driven by various mechanisms, such as electric motors or hydraulic systems, to rotate the workpiece at the desired speed and direction.

Tailstock: The tailstock is located opposite the wheelhead and supports the other end of the workpiece. It can be moved along the bed of the grinder to accommodate different workpiece lengths. The tailstock may have a center for supporting the workpiece or other devices for specific grinding operations.

Bed: The bed is the main base of the cylindrical grinder, providing stability and support for the various components. It is typically made of a heavy and rigid material, such as cast iron, to minimize vibrations and ensure accuracy during grinding operations.

0 notes

Text

Aircraft Electrical System Market May Set New Growth Story

Advance Market Analytics published a new research publication on "Aircraft Electrical System Market Insights, to 2028" with 232 pages and enriched with self-explained Tables and charts in presentable format. In the Study you will find new evolving Trends, Drivers, Restraints, Opportunities generated by targeting market associated stakeholders. The growth of the Aircraft Electrical System market was mainly driven by the increasing R&D spending across the world.

Get Free Exclusive PDF Sample Copy of This Research @ https://www.advancemarketanalytics.com/sample-report/63856-global-aircraft-electrical-system-market-1

The Aircraft Electrical System Market report covers extensive analysis of the key market players, along with their business overview, expansion plans, and strategies. The key players studied in the report include: AMETEK, Inc. (United States), Safran S.A. (France), Astronics Corporation (United States), Amphenol Corporation (United States), Esterline Technologies (United States), Honeywell Corporation (United States), Meggitt PLC (United Kingdom), Thales Group (France), United Technologies Corporation (United States), Crane Aerospace & Electronics (United States)

Definition:

Advancements in High-Density Battery Solutions for Electric Aircraft will help to boost global aircraft electrical system market in the forecasted period. An aircraft electrical system is a significant part of aircraft that has the capability to generate electricity. It is an independent network of components that generate, distribute, utilize, and store electrical energy .It is mainly driven by APU (auxiliary power unit) and a hydraulic motor or a RAT (Ram Air Turbine). Most aircraft are equipped with either a 28-volt- or a 14-volt direct current electrical system.

The following fragment talks about the Aircraft Electrical System market types, applications, End-Users, Deployment model etc. A thorough analysis of Aircraft Electrical System Market Segmentation: by Application (Aircraft Utility Management, Configuration Management, Power Generation Management, Flight Controls & Operations), Platform (Commercial Aviation, Military Aviation, Business & General Aviation), Component (Variable Frequency Generator, Generator Control Unit, Power Electronics, Transformer Rectifier Unit, Power Distribution Systems, Integrated Drive Generator), System (Power Generation, Conversion, Distribution, Energy Storage)

Aircraft Electrical System Market Drivers:

Upsurging Technological Advancements in Aircraft Based Electric Systems

Enhanced Aircraft Performance with The Increasing Uses of Electrical Energy

Aircraft Electrical System Market Trends:

Introduction to High-Density Battery Solutions for Electric Aircraft

Growing Adoption of No-Bleed Systems Aircraft Architecture and Hybrid Or Electric Propulsion System Design

Aircraft Electrical System Market Growth Opportunities:

Growing Use of Lightweight Wiring in Aircraft Electrical Systems

Introduction to Fuel Cell Technology, and Electric Actuation System

As the Aircraft Electrical System market is becoming increasingly competitive, it has become imperative for businesses to keep a constant watch on their competitor strategies and other changing trends in the Aircraft Electrical System market. Scope of Aircraft Electrical System market intelligence has proliferated to include comprehensive analysis and analytics that can help revamp business models and projections to suit current business requirements.

We help our customers settle on more intelligent choices to accomplish quick business development. Our strength lies in the unbeaten diversity of our global market research teams, innovative research methodologies, and unique perspective that merge seamlessly to offer customized solutions for your every business requirement.

Have Any Questions Regarding Global Aircraft Electrical System Market Report, Ask Our Experts@ https://www.advancemarketanalytics.com/enquiry-before-buy/63856-global-aircraft-electrical-system-market-1

Strategic Points Covered in Table of Content of Global Aircraft Electrical System Market:

Chapter 1: Introduction, market driving force product Objective of Study and Research Scope the Aircraft Electrical System market

Chapter 2: Exclusive Summary and the basic information of the Aircraft Electrical System Market.

Chapter 3: Displaying the Market Dynamics- Drivers, Trends and Challenges & Opportunities of the Aircraft Electrical System

Chapter 4: Presenting the Aircraft Electrical System Market Factor Analysis, Porters Five Forces, Supply/Value Chain, PESTEL analysis, Market Entropy, Patent/Trademark Analysis.

Chapter 5: Displaying the by Type, End User and Region/Country 2018-2022

Chapter 6: Evaluating the leading manufacturers of the Aircraft Electrical System market which consists of its Competitive Landscape, Peer Group Analysis, BCG Matrix & Company Profile

Chapter 7: To evaluate the market by segments, by countries and by Manufacturers/Company with revenue share and sales by key countries in these various regions (2023-2028)

Chapter 8 & 9: Displaying the Appendix, Methodology and Data Source

Finally, Aircraft Electrical System Market is a valuable source of guidance for individuals and companies.

Read Detailed Index of full Research Study at @ https://www.advancemarketanalytics.com/reports/63856-global-aircraft-electrical-system-market-1

What benefits does AMA research study is going to provide?

Latest industry influencing trends and development scenario

Open up New Markets

To Seize powerful market opportunities

Key decision in planning and to further expand market share

Identify Key Business Segments, Market proposition & Gap Analysis

Assisting in allocating marketing investments

Thanks for reading this article; you can also get individual chapter wise section or region wise report version like North America, Middle East, Africa, Europe or LATAM, Southeast Asia.

Contact US :

Craig Francis (PR & Marketing Manager)

AMA Research & Media LLP

Unit No. 429, Parsonage Road Edison, NJ

New Jersey USA – 08837

Phone: +1 201 565 3262, +44 161 818 8166

[email protected]

#Global Aircraft Electrical System Market#Aircraft Electrical System Market Demand#Aircraft Electrical System Market Trends#Aircraft Electrical System Market Analysis#Aircraft Electrical System Market Growth#Aircraft Electrical System Market Share#Aircraft Electrical System Market Forecast#Aircraft Electrical System Market Challenges

0 notes

Text

#Global Hydraulic Power Motor Market Size#Share#Trends#Growth#Industry Analysis#Key Players#Revenue#Future Development & Forecast

0 notes

Text

Powering Precision: The Hydraulic Motor Revolutionizing Injection Moulding in India

In the dynamic landscape of manufacturing, precision and efficiency are paramount. When it comes to injection moulding machines, the heart of the operation lies in the power source that drives its intricate mechanisms. This is where Polaris Hydrotechnik steps in, revolutionizing the industry with its cutting-edge hydraulic motors that redefine performance standards in India's manufacturing sector.

Introducing Polaris Hydrotechnik: A Beacon of Innovation

Polaris Hydrotechnik, a prominent name in the realm of hydraulic solutions, has been at the forefront of innovation for decades. Their commitment to excellence and relentless pursuit of technological advancement has positioned them as a leader in the market. With a focus on meeting the unique demands of the Indian manufacturing landscape, Polaris Hydrotechnik has introduced a range of hydraulic motors specifically tailored for injection moulding machines.

Precision Engineering: The Core of Polaris Hydraulic Motors

At the heart of every injection moulding machine lies a hydraulic motor that drives the intricate process of material injection with unparalleled precision. Polaris Hydrotechnik understands the critical role these motors play in the manufacturing process and has engineered its products to deliver exceptional performance, reliability, and efficiency.

Key Features and Benefits

Optimized Performance: Polaris hydraulic motors are designed to deliver optimized performance, ensuring smooth and consistent operation even under the most demanding conditions. With high torque and speed capabilities, these motors enable faster cycle times and increased productivity.

Energy Efficiency: In today's eco-conscious world, energy efficiency is non-negotiable. Polaris hydraulic motors are engineered to minimize energy consumption without compromising on performance, helping manufacturers reduce their carbon footprint and operating costs.

Durability and Reliability: Built to withstand the rigors of industrial use, Polaris hydraulic motors are constructed from high-quality materials and undergo rigorous testing to ensure maximum durability and reliability. This translates to minimal downtime and long-term cost savings for manufacturers.

Customization Options: Recognizing that every manufacturing process is unique, Polaris Hydrotechnik offers customization options to meet specific customer requirements. Whether it's adjusting motor size, mounting configuration, or performance characteristics, their team of experts works closely with clients to deliver tailored solutions that optimize productivity and efficiency.

Empowering Indian Manufacturers

India's manufacturing sector is experiencing rapid growth, driven by increasing demand for quality products across various industries. Polaris Hydrotechnik is committed to empowering Indian manufacturers with the tools they need to stay ahead of the curve. By providing innovative hydraulic motor solutions that enhance productivity, efficiency, and reliability, they are playing a pivotal role in fueling the country's industrial progress.

Conclusion

Innovation is the lifeblood of the manufacturing industry, and Polaris Hydrotechnik is leading the charge with its revolutionary hydraulic motor solutions. By combining cutting-edge technology with a deep understanding of customer needs, they are setting new benchmarks for performance, reliability, and efficiency in the injection moulding sector. As India continues to solidify its position as a global manufacturing powerhouse, Polaris Hydrotechnik stands ready to support the nation's growth trajectory with its unrivaled hydraulic motor solutions.

Visit us https://indiahydraulicmotors.com/application/

#Hydraulic motor for mobile cranes manufacturer in india#Hydraulic motor for injection moulding machine manufacturer in india

0 notes

Text

The Automobile Liquid Accumulator Market Is Estimated To Witness High Growth Owing To Rising Automobile Production And Sales Globally

The automobile liquid accumulator is a pressure vessel that is used in automobile braking and suspension systems to store hydraulic or nitrogen gas under pressure. It maintains reasonable pressure in the lines even when the pump is not working. The growing automobile production and sales globally is fueling the demand for automobile liquid accumulators that are used in braking and suspension systems of vehicles. The global automobile market has been witnessing strong growth over the past few years with developing regions leading the sales.

The global Automobile Liquid Accumulator Market is estimated to be valued at US$ 2080.75 Mn in 2023 and is expected to exhibit a CAGR of 4.1% over the forecast period 2024 to 2031, as highlighted in a new report published by Coherent Market Insights.

Market Dynamics:

One of the key drivers for the growth of the automobile liquid accumulator market is the rising automobile production and sales globally. As per data by International Organization of Motor Vehicle Manufacturers, total automobile sales reached over 95 million units in 2021 registering a growth of 3.3% from 2020. Developing regions like Asia Pacific witnessed strong sales growth over the past decade led by countries like China and India. This rising automobile demand is fueling the need for automobile suspension and braking systems, which in turn is driving the demand for automobile liquid accumulators used in these systems. Moreover, the increasing technological advancements in suspension and braking systems by automakers to improve vehicle performance and safety is further augmenting the market growth of automobile liquid accumulators over the forecast period.

SWOT Analysis

Strength: The automobile liquid accumulator market has strong growth prospects due to increasing vehicle production and sales globally. Automobile manufacturers are focusing on developing advanced accumulator systems to improve vehicle efficiency and performance. New product launches catering to electric and hybrid vehicles will further drive their demand.

Weakness: High costs associated with research and development of advanced accumulator technologies can restrain market growth. Stringent emissions norms requiring upgrades to existing accumulator designs also increase production expenses.

Opportunity: Rising demand for fuel-efficient vehicles especially in developing nations provides major opportunities for accumulator manufacturers. The growing electric vehicle market also offers scope to develop customized accumulator solutions. Hybrid versions of commercial vehicles could boost replacement demand.

Threats: Trade wars and economic uncertainty impact automobile sales negatively affecting accumulator demand. Strict environmental rules pose compliance challenges. New energy technologies for vehicles may replace conventional accumulator usage over the long term.

Key Takeaways

The global automobile liquid accumulator market growth is expected to witness high growth over the forecast period driven by increasing vehicle production worldwide. The global Automobile Liquid Accumulator Market is estimated to be valued at US$ 2080.75 Mn in 2023 and is expected to exhibit a CAGR of 4.1% over the forecast period 2024 to 2031.

Regional analysis:

Asia Pacific dominates automobile liquid accumulator usage owing to its large automobile manufacturing base. China is currently the largest producer and consumer of vehicles globally with annual output exceeding 25 million units. Other Asian countries like India and Japan also have sizable automobile industries relying heavily on accumulators. The Asia Pacific region accounts for over 60% of the global market share currently.

Key players:

Key players operating in the automobile liquid accumulator market are Liebherr-International AG, Shanghai Zhenhua Heavy Industries Co., Ltd., Wison Group, Konecranes, Kalmar, Kranunion GmbH, Sany Group Co., Ltd., Noell Crane Systems (China) Limited, Anupam Industries Limited. They cater to original equipment manufacturers as well as the aftermarket through product innovations and expansions.

Get more insights on this topic: https://www.newsstatix.com/automobile-liquid-accumulator-market-industry-insights-trends-automobile-liquid-accumulator-market/

Explore more information on this topic, Please visit: https://techaxen.com/forging-an-ancientals-forming-process-still-thriving-in-modern-times/

#Automobile Liquid Accumulator#Automobile Liquid Accumulator Market size#Automobile Liquid Accumulator Market share#Automobile Liquid Accumulator Market demand#Automobile Liquid Accumulator Market analysis

0 notes

Text

Industrial Robotic

The Genesis of Industrial Robots: A Historical Perspective

Industrial robots have been an integral part of the manufacturing industry for decades. The evolution of industrial robots can be traced back to the 1930s when the earliest known industrial robot was created by Griffith “Bill” P. Taylor. Since then, the development of industrial robots has been marked by several key milestones and breakthroughs. In the 1950s, George Devol developed the first industrial robot, a two-ton device that autonomously transferred objects from one place to another with hydraulic actuators. In the 1960s, the first industrial robot was installed in a General Motors plant in New Jersey. In the 1970s, the first microprocessor-controlled robot was developed. In the 1980s, the first robot with six degrees of freedom was introduced. In the 1990s, the first collaborative robot was developed. Today, industrial robots are used in a wide range of applications, from welding and painting to assembly and packaging.

The global industrial robotics market is poised for dynamic growth. The report identifies several qualitative factors that are driving this growth, including dramatic developments in technology and new applications as well as global trends of rising labour costs, increasing labour turnover and shortages, and decreasing equipment costs and global competition. The report also identifies key options for unleashing the market’s full growth potential, including developing standards for interoperability, promoting robotics-related upskilling and retraining at scale, and bringing robotics to small and medium-sized companies.

Types of Industrial Robots: From Assembly Lines to Smart Factories

Industrial robots are used in a wide range of applications, from welding and painting to assembly and packaging. There are several types of industrial robots available on the market, each with its unique capabilities and strengths. Here’s a brief overview of some of the most common types of industrial robots:

Articulated Robots: These robots have a flexible movement and can be quite powerful, capable of lifting heavy objects. They are most commonly used for tasks like picking and placing, sorting, assembling, welding, and finishing.

Cartesian Robots: These robots move in straight lines along three axes and are ideal for tasks that require high precision and repeatability, such as drilling, milling, and cutting.

SCARA Robots: These robots have a horizontal arm that can move in a circular motion and are ideal for tasks that require high speed and precision, such as assembly and packaging.

Delta Robots: These robots have a unique design that allows them to move very quickly and are ideal for tasks that require high speed and precision, such as pick-and-place operations.

Gantry Robots: These robots have a large work envelope and are ideal for tasks that require high payloads and long reach, such as material handling and palletizing.

Cylindrical Robots: These robots have a cylindrical work envelope and are ideal for tasks that require high speed and precision, such as assembly and packaging.

Collaborative Robots (Cobots): These robots are designed to work safely alongside humans and are ideal for tasks that require human-robot collaboration, such as assembly, packaging, and inspection.

Advanced Sensor Technologies: Enhancing Precision and Safety in Industrial Robotics

Advanced Sensor Technologies are revolutionizing the field of industrial robotics by enhancing precision and safety. These sensors are designed to capture data from the environment, robot, and/or user, and play a crucial role in increasing the safety, autonomy, and adaptability of robots.

Magnetic sensors contribute to self-diagnostics and fault detection, improving system reliability. Vision sensors provide visual perception capabilities, enabling robots to analyze and interpret visual information for complex tasks.

In addition, smart sensors are an integral part of the Fourth Industrial Revolution and are widely used to add safety measures to human-robot interaction applications. With the advancement of machine learning methods in resource-constrained environments, smart sensor systems have become increasingly powerful.

The presence of robots in a variety of scenarios has increased substantially in recent years, as their ability to solve diverse tasks has improved. In all cases, sensing technologies play a crucial role in capturing the necessary information from the environment, robot, and/or user. To address any specific task, the robot has to be equipped with different kinds of sensors to perceive the surroundings, such as touch sensors, laser rangefinders, GPS, visual sensors or combined vision-depth platforms. In some applications, a combination of these is used, and data-fusion algorithms must be implemented. Currently, machine learning and deep learning approaches may play an important role in data analysis, interpretation, and fusion. Additionally, some specific tasks can be performed more efficiently if a team of robots is used, so an optimal combination of the information captured between the different sensors is crucial. In this sense, IoT (Internet of Things) approaches may ease this labour

Programming Industrial Robots: Bridging the Gap Between Man and Machine

Programming industrial robots is a complex task that requires a deep understanding of the underlying hardware and software. Industrial robots are designed to perform repetitive tasks with high precision and accuracy, and they are widely used in manufacturing, assembly, and other industries. In recent years, there has been a growing interest in bridging the gap between man and machine, and this has led to the development of new programming techniques and tools.

it is essential to have a deep understanding of the underlying hardware and software of industrial robots. Robot programming languages are sometimes needed to implement robot-specific functionality, and a helpful tool for bridging the gap between high-level languages and robot controllers. It allows easily reading and writing a robot controller’s variables from a Java program.

In addition, machine learning and deep learning approaches may play an important role in data analysis, interpretation, and fusion1. Currently, machine learning methods are being used to improve the performance of industrial robots, and this has led to the development of new programming techniques and tools.

Industry 4.0 and the Rise of Smart Manufacturing: Integrating Robotics into the Digital Landscape

The integration of robotics into the digital landscape is a key component of Industry 4.0. Robots are increasingly used in manufacturing for tasks ranging from repetitive assembly to complex quality control. The development of mobile robots capable of navigating complex environments and working in teams to complete tasks is a hallmark of Industry 4.0. The use of robots in manufacturing not only reduces labor costs but also enhances precision and consistency. The integration of robotics into the digital landscape has enabled manufacturers to optimize their operations, reduce costs, and improve product quality.

Industrial robotics has been a rapidly growing field in recent years, with the potential to increase efficiency and productivity in industrial settings. However, the high implementation costs of robots mean that large organizations tend to invest more than SMEs in using and integrating robots into their operations. The report highlights the challenges faced by operators, such as interoperability and cybersecurity vulnerabilities, as they strive to incorporate evolving technologies. One trend that is likely to gain traction is the incorporation of AI and machine learning in robots to aid decision-making 1. The report also includes country-level data on new installations and growth and highlights how robots contribute to a reduced carbon footprint, making them an imperative tool for driving sustainability efforts.

In terms of future trends, path smoothing techniques in robot navigation are an area of active research. The aim of this research is to improve the efficiency and safety of robot navigation in industrial settings. Both autonomous mobile robots and autonomous vehicles (outdoor robots or self-driving cars) are discussed.

For more information visit our website: www.unboxindustry.com

1 note

·

View note

Last Seen Blogs

acploves2run

Be unapologetic in the ways you are powerful.

hhhhhh33

无标题

biponk

captugraphe

jacksino5

Untitled

kimoglaze222

Untitled