#Aerospace Foams industry

Text

The aerospace foams market size is projected to grow from USD 4.4 billion in 2019 to USD 6.5 billion by 2024, at a CAGR of 8.2% from 2019 to 2024. The rising demand for lightweight and fuel-efficient aircraft have led to the extensive use of advanced materials such as PU foams and PE foams, among others, in the aerospace industry. The manufacture of advanced materials as well as new products launched by several prominent players for the aerospace industry is one of the key factors driving the growth of the aerospace foams industry across the globe.

Aerospace foams are advanced materials of various cell sizes, capacities, and properties. The cell sizes of the aerospace foams determine the flexibility or rigidity of the foams and thus, dictates the application areas where they can be used. Aerospace foams are manufactured using various materials, such as PU (polyurethane), PE (polyethylene), melamine, metal, and PMI/polyimide, among others, which meet the flame, smoke, and toxicity (FST) standards in the aerospace industry. These foams are used in various applications in aircrafts such as seating, seals, gaskets, carpet pads, headrests, rotor blades, doors, windshields, cockpit instrument panels, wingtip lens, and several others.

Based on material type, the aerospace foams market has been segmented into PU foams, PE foams, melamine foams, metal foams, PMI/polyimide foams, and others which includes PVDF foams, PPSU foams, silicone foams, ceramic foams, PEI foams, PET foams, PVC foams, and polycarbonate foams. The PU foams segment has the highest market share in terms of both value and volume, among all the material type segments in 2018. It is projected to follow the same trend from 2019 to 2024 in terms of both value and volume. PU foams are used in a variety of applications ranging from seating, airframes, interiors, and packaging in the aerospace industry. The availability in different forms ranging from low to high density with varying rigidity as well as ease-of-use makes them compatible to be used in a multitude of aerospace applications. Some useful properties of PU foams include durability, lightweight, and recyclability. These factors support the rising global demands for lightweight and fuel-efficient aircraft, which is one of the primary drivers of the aerospace foams market.

#Aerospace Foams Market#PU Foams#PE Foams#Melamine Foams#Metal Foams#PMI Foam#Polyimide Foams#erg metal foam#Global Aerospace Foams Market#COVID 19 impact on Aerospace Foams Market#Aviation foam suppliers#Aircraft structural foam#Aerospace Foams industry#Aerospace Foams Market Share#Aerospace Foams Market size#Demand of Aerospace Foams#Sales of Aerospace Foams#Aerospace Foams Market Manufacturers#Aerospace Foams Market Opportunity#growth of the aerospace foams industry#commercial aircraft Foams#aviation foams#PU aerospace foams

0 notes

Text

Navigating the Aerospace Foam Market Landscape: Key Players and Strategies

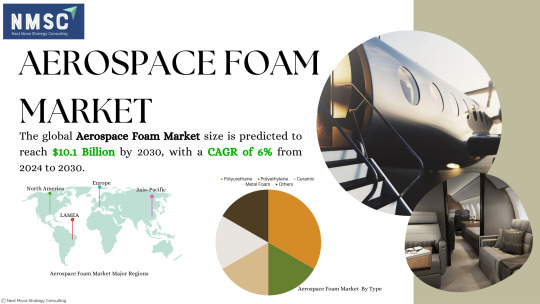

According to a comprehensive study conducted by Next Move Strategy Consulting, the global Aerospace Foam Market is poised to witness significant growth, with a predicted size of USD 10.1 billion and a compound annual growth rate (CAGR) of 5.8% by the year 2030.

This projection underscores the pivotal role that aerospace foam plays in shaping the trajectory of the aerospace industry, providing lightweight, durable, and innovative solutions to meet the evolving demands of modern aviation and space exploration.

Introduction:

The aerospace industry stands at the forefront of technological innovation, constantly pushing boundaries to enhance efficiency, safety, and performance. Central to this evolution is the integration of advanced materials, with aerospace foam emerging as a critical component in the pursuit of lightweight structures and enhanced functionalities.

Request for a sample, here: https://www.nextmsc.com/aerospace-foam-market/request-sample

Aerospace Foam Market Dynamics:

Understanding the dynamics of the aerospace foam market requires a closer look at the key players shaping its landscape. A multitude of factors, including technological advancements, market trends, and regulatory considerations, influence the strategies adopted by industry leaders.

Key Players in the Aerospace Foam Market:

Several prominent market players contribute to the growth and innovation within the aerospace foam market. Notable names such as BASF SE, Evonik Industries AG, Solvay, Greiner Aerospace, Boyd Corporation, Huntsman Corporation, Armacell, Pyrotek Inc., Zotefoams Plc, and General Plastics Manufacturing Company are among the industry giants actively engaged in developing and delivering cutting-edge solutions.

Strategies for Market Dominance:

Aerospace foam market players employ various strategies to maintain dominance and meet the ever-evolving needs of the industry. One common approach is the continuous launch of new and innovative products across different regions, enabling companies to stay ahead of the competition and cater to diverse market demands.

Strategic Partnerships: A notable example is the strategic partnership between Solvay and Zotefoams Plc. In June 2023, the two entities entered into a long-term supply agreement to enhance the availability of advanced cellular materials, including foams. This collaboration serves as a strategic move to address the growing demand for high-performance materials in critical applications, especially within the aerospace sector.

Innovative Product Launches: The aerospace industry demands materials that can withstand rigorous conditions while being lightweight and efficient. In May 2023, Huntsman Corporation announced the development of new materials specifically designed for aerospace applications. This innovation aims to meet the demanding requirements of the aerospace industry, focusing on enhancing performance and efficiency. The introduction of these materials underscores Huntsman's commitment to advancing technology in the aerospace foam market.

Strategic Investments: Evonik Industries AG, in March 2022, made a significant investment in a new production facility for Rohacell, a high-performance structural foam. This investment signals a commitment to advancing aerospace foam technology, catering to the increasing demand for lightweight and durable materials in the aerospace industry.

Market Trends and Future Outlook:

To navigate the aerospace foam market landscape effectively, it is crucial to stay abreast of emerging trends that influence industry dynamics. Key trends include:

Sustainability Initiatives: The aerospace industry is increasingly prioritizing sustainability, pushing market players to develop eco-friendly foam solutions that align with global environmental goals.

Digital Transformation: The integration of digital technologies is transforming manufacturing processes and supply chain management within the aerospace foam market, enhancing efficiency and reducing costs.

Urban Air Mobility (UAM): The rise of UAM presents new opportunities for aerospace foam market players, with the demand for lightweight materials in electric vertical takeoff and landing (eVTOL) vehicles.

Regional Insights and Market Segmentation:

The aerospace foam market is inherently diverse, with different regions exhibiting unique challenges and opportunities. Understanding regional dynamics and market segmentation is crucial for companies aiming to establish a global presence.

BASF SE: As one of the leading players in the aerospace foam market, BASF SE continually strives for innovation. An in-depth exploration of the company's strategies, product launches, and market influence provides valuable insights into its role within the industry.

Boyd Corporation: Examining Boyd Corporation's approach to market challenges, product development, and strategic partnerships sheds light on how this player maintains its competitive edge.

Challenges and Opportunities:

Navigating the aerospace foam market landscape is not without its challenges. From stringent industry regulations to evolving consumer preferences, companies must be agile in addressing obstacles while seizing opportunities for growth.

Supply Chain Disruptions: Global events such as pandemics, natural disasters, or geopolitical tensions can disrupt the aerospace foam supply chain, impacting production schedules and increasing costs. Companies need robust contingency plans to mitigate the effects of such disruptions and ensure continuity of operations.

Technological Complexity: Developing advanced aerospace foam solutions requires significant investment in research and development. Companies must navigate the complexities of material science, manufacturing processes, and regulatory compliance to bring innovative products to market successfully.

Competition from Alternative Materials: While aerospace foam offers unique advantages in terms of weight reduction and performance, it faces competition from alternative materials such as composite materials, lightweight metals, and 3D-printed components. Companies must differentiate their offerings and demonstrate the superior benefits of foam-based solutions to maintain a competitive edge.

Environmental Sustainability: The aerospace industry is under increasing pressure to reduce its environmental footprint and embrace sustainable practices. Companies in the aerospace foam market must innovate to develop eco-friendly foam materials that minimize environmental impact while meeting stringent performance requirements.

Future Outlook:

Despite these challenges, the aerospace foam market presents significant opportunities for growth and innovation. Advancements in material science, manufacturing technologies, and market demand for more efficient and sustainable solutions are driving the evolution of the industry.

Emerging Markets: Rapid urbanization, economic growth, and increased air travel demand in emerging markets present new opportunities for aerospace foam manufacturers. Companies that can adapt their strategies to cater to the specific needs of these markets stand to gain a competitive advantage.

Integration of Advanced Technologies: The integration of advanced technologies such as artificial intelligence, machine learning, and additive manufacturing is revolutionizing the aerospace foam industry. Companies that embrace these technologies can enhance product development processes, optimize production efficiency, and deliver tailored solutions to customers.

Collaboration and Partnerships: Collaboration between industry stakeholders, including manufacturers, suppliers, research institutions, and government agencies, is essential for driving innovation and addressing common challenges. Strategic partnerships can leverage complementary expertise and resources to accelerate product development and market penetration.

Focus on Customer-Centric Solutions: As aerospace OEMs and end-users increasingly prioritize performance, reliability, and cost-effectiveness, companies in the aerospace foam market must focus on delivering customer-centric solutions. Understanding and anticipating customer needs, preferences, and pain points are critical for maintaining competitiveness and driving long-term growth.

Inquire before buying, here: https://www.nextmsc.com/aerospace-foam-market/inquire-before-buying

Conclusion:

In conclusion, the aerospace foam market is a dynamic and rapidly evolving sector within the broader aerospace industry. Key players are instrumental in shaping its trajectory through strategic partnerships, innovative product launches, and investments in advanced technologies. As the demand for lightweight, durable materials continues to rise, the aerospace foam market's future holds exciting possibilities, providing ample opportunities for companies to pioneer advancements and contribute to the next era of aerospace innovation.

0 notes

Text

Aerospace Foam Market will reach at a CAGR of 6.9% from 2023 to 2029

As per the new study published by Data Library Research, titled, “Aerospace Foam market by type, application, end user, and region: industry forecast and market potential analysis, 2023-2029,” the global Aerospace Foam market is rising at substantial rate and is projected to maintain its progress during the prediction period.

The study elaborates growth rate of the Aerospace Foam market…

View On WordPress

#Aerospace Foam#Aerospace Foam forecast#Aerospace Foam industry#Aerospace Foam market#Aerospace Foam price#Aerospace Foam share#Aerospace Foam trends

0 notes

Text

High Heat Foam Market

The report proves to be an effective tool that players can use to gain a competitive edge over their competitors and ensure lasting success in the global High Heat Foam market.

Download Free Research Report Sample PDF: https://cutt.ly/MMzVhFh

#highheatfoam#heatfoam#heatfoammarket#foam#foammarket#highheatfoammarket#heat#highheat#silicone#polyimide#melamine#polyethylene#automotive#industrial#aerospace#chemicals#chemicalsmarket#chemicalsindustry#chemicalsmanufacturer#statsmarketresearch

0 notes

Text

California State Senator Ben Allen represents the 24th Senate District, covering the Westside, Hollywood, South Bay, and Santa Monica Mountains communities of Los Angeles County. Ben was first elected in 2014 and is now serving his third and final term in the State Senate.

Ben chairs the Senate's Environmental Quality Committee and co-chairs the Legislature's Environmental Caucus, is a member of the Legislative Jewish Caucus, chairs the Legislature's Joint Committee on the Arts, and the Senate Select Committee on Aerospace and Defense. He previously served as Chair of the Education Committee (2017-2019) and Chair of the Elections and Constitutional Amendments Committee (2015-2016).

Ben has thrown himself into the important work of state government, focusing on wise decision-making and pushing for reforms that address systemic inadequacies in our state. He has authored nearly 60 new laws in various areas, from environmental protection to electoral reform.

During his first two terms in the Senate, fighting the climate crisis and protecting our state's precious natural resources have been among Ben's top priorities. CalMatters recently recognized him as one of the Legislature's foremost leaders in the field of environmental protection. He authored SB 54, groundbreaking legislation to address plastic pollution, which Governor Newsom signed into law to international acclaim. The New York Times called SB 54 "the most sweeping restrictions on plastics in the nation" and suggested the legislation is "another route for curbing carbon emissions and trying to sidestep the worst consequences of global warming" after the Supreme Court gutted the federal government's power to regulate carbon emissions. As Chair of the Senate Environmental Quality Committee, Ben worked with his colleagues to pass a powerful climate package requiring the state to become carbon-neutral by 2045 and produce 90% of its electricity from clean sources by 2035, among other measures. A member of the Ocean Protection Council and Coastal Conservancy, he has led a successful effort to phase out a dangerous carcinogen in firefighting foam, crafted a compromise to phase out destructive trawling gear, and brokered a major compromise that lessened the environmental impact of off-highway vehicle use at state facilities. "If only Congress could work out such compromises," wrote the Sacramento Bee editorial board about the bill.

Among his efforts to reform California campaign finance and elections laws, Ben authored the landmark Voter's Choice Act of 2016 to implement more flexibility in how and where to vote, creating the vote center model used in the 2020 elections, which resulted in significantly increased voter turnout. Ben also has been a leader for campaign transparency, and was a leader in passing the Disclose Act and Petition Disclose Act and other transparency measures that have dramatically improved the disclosure of donors to political causes for the public. The California Clean Money Campaign has routinely ranked him top in the Legislature for his commitment to clean money political reform.

An advocate for the Golden State's continued leadership in arts and entertainment, Ben is a member of the California Film Commission. He was part of a legislative effort to extend the Film & TV Tax Credit Program to further support and invest in California’s unrivaled film industry. Ben also authored the law that reinstated teaching credentials for theatre and dance educators, and he continues to fight for expanded access to the arts in schools and underserved communities. Ben has been a champion for science and was a joint author of the state's groundbreaking law that increased vaccination rates among school children.

Prior to his election to the Senate, Ben served as President of the Santa Monica-Malibu Unified School District Board of Education, lecturer at UCLA Law School, and worked as an attorney at the law firms of Bryan Cave LLP and Richardson & Patel and at the nonprofit Spark Program. While at law school, Ben served as the voting student member of the University of California Board of Regents and was a summer judicial clerk with the United Nations International Criminal Tribunal for Rwanda. Prior to law school, Ben worked in Washington DC for the Latin American team of the National Democratic Institute for International Affairs (NDI), and then as Communications Director for Congressman Jose Serrano (D-NY).

Ben grew up in the 24th Senate District and attended public schools, graduating from Santa Monica High School in 1996. His father, Michael, spent his career on the English Department faculty at UCLA and mother, Elena, was a public school teacher and artist who served as Chair of the Santa Monica Arts Commission. Ben has a Bachelor of Arts degree magna cum laude in History from Harvard University; a Master's degree in Latin American Studies from the University of Cambridge; and a Juris Doctor degree from UC Berkeley. Fluent in Spanish, Ben is a Senior Fellow with the international human rights organization Humanity in Action, an Aspen Institute-Rodel Fellow, a Truman National Security Project Fellow, and a graduate of the Jewish Federation's New Leaders Project. He and his wife Melanie, an attorney, have a little son, Ezra.

3 notes

·

View notes

Text

We offer a range of industrial cleaning services – Ultra high-pressure (UHP) water jetting, Dry ice blasting + glass beads, Fin fan foam cleaning, and chemical cleaning to meet our customers’ requirements in different industries such as aerospace, oil & gas, automotive, food & packaging, foundry, medical, printing, marine, building & infrastructure, and more!

For more details about this service, drop us an email at [email protected] | visit us at petracarbon.com.sg

#engineering#industrial#cleaning#maintenancecare#water jets#dry ice blasting#solutions#services#oil and gas#marine#automotive

3 notes

·

View notes

Text

PUF Panels and Sandwich Panels: Applications Across Industries

Efficiency, durability, and versatility are essential in the realms of construction and industrial design. One innovation that has revolutionized these aspects is the introduction of Polyurethane Foam (PUF) panels and sandwich panels. These composite materials, consisting of a core sandwiched between two outer layers, offer numerous advantages and are widely used across various industries. In this text, we will explore the different areas where PUF panels and sandwich panels are commonly applied.

Cold Storage and Refrigeration: PUF panels excel in thermal insulation properties, making them ideal for cold storage facilities and refrigeration units. These panels create an efficient barrier against temperature fluctuations, helping to maintain the desired temperature inside the storage area. From food processing plants to pharmaceutical storage facilities, PUF panels ensure the integrity and freshness of perishable goods.

Commercial and Industrial Buildings: The versatility of PUF panels and sandwich panels extends to the realm of commercial and prefab construction. These panels are widely used for roofing, wall cladding, and partitioning in warehouse manufacturers, factories, workshops, and offices. Their lightweight nature facilitates quick installation, reducing construction time and costs. Moreover, their excellent insulation properties contribute to energy efficiency, leading to reduced heating and cooling expenses.

Modular Construction: The modular construction industry heavily relies on PUF panels and sandwich panels for their prefabricated structures. Whether it's modular homes, portable cabins, or temporary shelters, these panels offer a convenient solution for rapid assembly and disassembly. The modular nature of PUF panels allows for easy customization, enabling architects and designers to create versatile spaces tailored to specific needs.

Transportation Sector: PUF panels play a vital role in the transportation sector, particularly in the construction of refrigerated trucks, vans, and containers. These panels help to create insulated compartments that safeguard perishable goods during transit. Additionally, sandwich panels find applications in the aerospace industry for aircraft interiors, providing lightweight yet robust solutions for cabin walls and partitions.

Clean Rooms and Laboratories: Precision-controlled environments such as clean rooms and laboratories require stringent temperature and contamination control. PUF panels offer an ideal solution due to their ability to create airtight enclosures with superior insulation properties. These panels help maintain stable environmental conditions necessary for sensitive manufacturing processes, research, and testing activities.

Agricultural Sector: In agriculture, PUF panels are utilized for constructing storage facilities, cold rooms, and greenhouses. These panels help farmers and growers extend the shelf life of their produce by providing an insulated environment conducive to preservation. Additionally, sandwich panels are employed in livestock housing, offering comfortable and hygienic shelters for animals.

Conclusion: PUF panels and sandwich panels have emerged as indispensable materials across a myriad of industries, thanks to their exceptional thermal insulation, structural strength, and versatility. From cold storage facilities to commercial buildings, from transportation to clean room environments, the applications of these panels are diverse and far-reaching. As technology continues to advance, we can expect further innovations in the design and utilization of PUF panels, driving efficiency, sustainability, and performance across various sectors.

1 note

·

View note

Text

Acrylic Foam Tape Manufacturers Bring Perfect Adhesive Solutions in Cheap!

Acrylic foam tape revolutionizes bonding application across the industries with a versatile adhesive solution. This adhesive on both sides is composed of a viscoelastic acrylic foam core; with durability and strength this tape offers unexpected bonding. It has unique composition that allows it to conform to irregular surfaces while creating a strong bond and permanent bond that can resist the temperature fluctuations, UV exposure and moisture. One of the best features of this foam tape is that its ability to distribute stress evenly and the risk of substrate damage or failure are reduced. This makes an ideal choice for people to use it.

Brings innovative adhesive solutions

In supplying industries with innovative adhesive solutions Acrylic foam tape manufacturers plays a vital role while meeting diverse bonding needs. In research and development to engineer tapes that exhibit superior performance, versatility and durability this manufactures invest heavily. To produce acrylic foam tapes with consistent quality and adherence to stringent standards the leading manufacturers employ advanced manufacturing processes. Throughout the process they utilize state of the art facilities and stick to a strict quality control measures to ensure that each roll of tape meets or exceeds expectations of the customer. And where precision and reliability are supreme, acrylic foam tape finds application in electronics and aerospace industries.

Comes with excellent adhesion and tack

Ensuring a strong bond upon the application the acrylic double sided tape provides an excellent initial tack and adhesion. Even in challenging conditions this tape maintains it's bonding strength over time and making it ideal for long term bonding solutions. In industries like automotive, electronics and construction this doubled sided tape is widely used. While offering a cleaner and more efficient alternative to traditional mechanical, the automotive manufacturers use this tape for attaching trim, molding and emblems. Providing a secure and aesthetically pleasing solution, in construction it is used for mounting mirrors, glass, and other elements that are architectural.

0 notes

Text

Eco-friendly Innovations Propel Industrial Foam Market Toward Sustainable Growth on Global Scale by 2033

Overview and Scope

Industrial foam is an expanded plastic and rubber created by forcing gas bubbles into a polymer material. Industrial foam is highly-efficient for insulation against water, air, chemical substances, and adhesives. Industrial foam is used as padding for several consumer and business products, such as mattresses, furniture, car interiors, carpet underlay, and packaging.

Sizing and Forecast

The industrial foam market size has grown strongly in recent years. It will grow from $63.14 billion in 2023 to $68.05 billion in 2024 at a compound annual growth rate (CAGR) of 7.8%.

The industrial foam market size is expected to see strong growth in the next few years. It will grow to $91.5 billion in 2028 at a compound annual growth rate (CAGR) of 7.7%.

To access more details regarding this report, visit the link:

https://www.thebusinessresearchcompany.com/report/industrial-foam-global-market-report

Segmentation & Regional Insights

The industrial foam market covered in this report is segmented –

1) By Foam Type: Flexible, Rigid

2) By Resin Type: Polyurethane, Polystyrene, Polyolefin, Phenolic, PET, Other Resin Types

3) By End-Use: Building And Construction, HVAC, Industrial Pipe Insulation, Marine, Aerospace, Industrial Cold Storage, Others End-Uses

Asia-Pacific was the largest region in the industrial foam market in 2023. Asia-Pacific is expected to be the fastest-growing region in the forecast period. The regions covered in the industrial foam market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East, Africa.

Intrigued to explore the contents? Secure your hands-on sample copy of the report:

https://www.thebusinessresearchcompany.com/sample.aspx?id=8209&type=smp

Major Driver Impacting Market Growth

Growing demand for energy-efficient and lightweight materials is expected to propel the industrial foam market. Lightweight materials are manufactured using lightweight raw materials that directly reduce the weight of the material while maintaining its performance. Industrial foam is a type of lightweight material made up of tiny cells filled with gas or air and used in applications such as insulation, packaging, and construction.

Key Industry Players

Major companies operating in the industrial foam market report are Covestro AG, BASF SE, Dow Inc., Huntsman Corporation, Sekisui Chemical Co. Ltd., Saint-Gobain S.A., Chemtura Corporation, Recticel N.V, Rogers Corporation

The industrial foam market report table of contents includes:

1. Executive Summary

2. Market Characteristics

3. Market Trends And Strategies

4. Impact Of COVID-19

5. Market Size And Growth

6. Segmentation

7. Regional And Country Analysis

.

.

.

27. Competitive Landscape And Company Profiles

28. Key Mergers And Acquisitions

29. Future Outlook and Potential Analysis

Contact Us:

The Business Research Company

Europe: +44 207 1930 708

Asia: +91 88972 63534

Americas: +1 315 623 0293

Email: [email protected]

Follow Us On:

LinkedIn: https://in.linkedin.com/company/the-business-research-company

Twitter: https://twitter.com/tbrc_info

Facebook: https://www.facebook.com/TheBusinessResearchCompany

YouTube: https://www.youtube.com/channel/UC24_fI0rV8cR5DxlCpgmyFQ

Blog: https://blog.tbrc.info/

Healthcare Blog: https://healthcareresearchreports.com/

Global Market Model: https://www.thebusinessresearchcompany.com/global-market-model

0 notes

Text

The aerospace foams market size is projected to grow from USD 4.4 billion in 2019 to USD 6.5 billion by 2024, at a CAGR of 8.2% from 2019 to 2024. The rising demand for lightweight and fuel-efficient aircraft have led to the extensive use of advanced materials such as PU foams and PE foams, among others, in the aerospace industry. The manufacture of advanced materials as well as new products launched by several prominent players for the aerospace industry is one of the key factors driving the growth of the aerospace foams industry across the globe.

Aerospace foams are advanced materials of various cell sizes, capacities, and properties. The cell sizes of the aerospace foams determine the flexibility or rigidity of the foams and thus, dictates the application areas where they can be used. Aerospace foams are manufactured using various materials, such as PU (polyurethane), PE (polyethylene), melamine, metal, and PMI/polyimide, among others, which meet the flame, smoke, and toxicity (FST) standards in the aerospace industry. These foams are used in various applications in aircrafts such as seating, seals, gaskets, carpet pads, headrests, rotor blades, doors, windshields, cockpit instrument panels, wingtip lens, and several others.

Based on material type, the aerospace foams market has been segmented into PU foams, PE foams, melamine foams, metal foams, PMI/polyimide foams, and others which includes PVDF foams, PPSU foams, silicone foams, ceramic foams, PEI foams, PET foams, PVC foams, and polycarbonate foams. The PU foams segment has the highest market share in terms of both value and volume, among all the material type segments in 2018. It is projected to follow the same trend from 2019 to 2024 in terms of both value and volume. PU foams are used in a variety of applications ranging from seating, airframes, interiors, and packaging in the aerospace industry. The availability in different forms ranging from low to high density with varying rigidity as well as ease-of-use makes them compatible to be used in a multitude of aerospace applications. Some useful properties of PU foams include durability, lightweight, and recyclability. These factors support the rising global demands for lightweight and fuel-efficient aircraft, which is one of the primary drivers of the aerospace foams market.

#Aerospace Foams Market#PU Foams#PE Foams#Melamine Foams#Metal Foams#PMI Foam#Polyimide Foams#erg metal foam#Global Aerospace Foams Market#COVID 19 impact on Aerospace Foams Market#Aviation foam suppliers#Aircraft structural foam#Aerospace Foams industry#Aerospace Foams Market Share#Aerospace Foams Market size#Demand of Aerospace Foams#Sales of Aerospace Foams#Aerospace Foams Market Manufacturers#Aerospace Foams Market Opportunity#growth of the aerospace foams industry#commercial aircraft Foams#aviation foams#PU aerospace foams

0 notes

Text

Technical Insulation Market: Trends, Growth, and Forecast

Introduction

The Technical Insulation Market plays a vital role in various industries by providing thermal, acoustic, and fire protection solutions. From residential buildings to industrial facilities, technical insulation is essential for optimizing energy efficiency, enhancing occupant comfort, and ensuring the safety and longevity of infrastructure. In this comprehensive analysis, we delve into the key trends, growth drivers, and future forecasts shaping the Technical Insulation Market.

According to the study by Next Move Strategy Consulting, the global Technical Insulation Market size is predicted to reach USD 11.82 billion with a CAGR of 4.0% by 2030.

Request for a sample, here: https://www.nextmsc.com/technical-insulation-market/request-sample

Trends Shaping the Technical Insulation Market

Rising Demand for Energy Efficiency

The increasing emphasis on energy efficiency across industries is a primary driver fueling the demand for technical insulation solutions. As organizations strive to reduce energy consumption and minimize environmental impact, there is a growing preference for insulation materials that offer superior thermal performance. Technical insulation plays a crucial role in minimizing heat loss or gain in buildings, industrial equipment, and pipelines, thereby contributing to energy conservation efforts.

Advancements in insulation materials, such as aerogels, vacuum insulation panels, and eco-friendly foams, are enabling improved thermal insulation properties while ensuring sustainability. These innovative materials offer high thermal resistance and durability, making them ideal for applications where energy efficiency is paramount.

Advancements in Insulation Materials

Technological innovations have revolutionized the technical insulation industry, leading to the development of advanced materials with superior performance characteristics. Traditional insulation materials such as fiberglass and mineral wool are being augmented with newer options that offer enhanced thermal conductivity, moisture resistance, and fire retardancy.

Aerogels, for instance, are lightweight, highly porous materials with exceptional thermal insulating properties. These silica-based materials possess low thermal conductivity, making them effective insulators for a wide range of applications, including building envelopes, cryogenic systems, and aerospace components.

Vacuum insulation panels (VIPs) represent another breakthrough in insulation technology. Consisting of a rigid core encased in a gas-tight envelope, VIPs achieve extremely low thermal conductivity by minimizing convective and conductive heat transfer. These panels are increasingly being used in refrigeration, cold chain logistics, and building insulation applications.

Furthermore, eco-friendly insulation materials derived from renewable sources, such as soybean oil-based foams and cellulose insulation made from recycled paper, are gaining traction due to their sustainability credentials. These bio-based materials offer comparable thermal performance to traditional insulation options while reducing environmental impact.

Focus on Green Building Standards

The construction industry is undergoing a paradigm shift towards sustainable building practices, driven by increasing awareness of environmental conservation and energy efficiency. Green building standards and certifications, such as LEED (Leadership in Energy and Environmental Design) and BREEAM (Building Research Establishment Environmental Assessment Method), are becoming increasingly prevalent, influencing design and construction decisions worldwide.

Technical insulation plays a pivotal role in achieving green building certifications by enhancing energy efficiency and thermal comfort within buildings. By minimizing heat transfer through walls, roofs, and floors, insulation helps reduce heating and cooling loads, thereby lowering energy consumption and operational costs. Additionally, insulation materials with high recycled content and low embodied energy contribute to the overall sustainability of building projects.

Expansion in Industrial Infrastructure

The rapid expansion of industrial infrastructure, particularly in emerging economies, is driving significant demand for technical insulation solutions. Industries such as power generation, oil and gas, petrochemicals, and manufacturing rely heavily on insulation to maintain optimal operating temperatures, protect personnel and equipment, and ensure process efficiency.

In power generation facilities, for example, thermal insulation is critical for steam turbines, boilers, and piping systems to minimize heat losses and maximize energy conversion efficiency. Similarly, in the oil and gas sector, insulation is utilized in pipelines, storage tanks, and processing equipment to prevent heat transfer, reduce energy consumption, and mitigate the risk of corrosion under insulation (CUI).

The petrochemical industry also relies on technical insulation for maintaining process temperatures and ensuring product quality and safety. Insulation materials with excellent chemical resistance and thermal stability are essential for withstanding harsh operating conditions in chemical processing plants and refineries.

Growth Drivers of the Technical Insulation Market

Regulatory Mandates

Stringent regulations and building codes mandating the use of energy-efficient insulation materials are driving market growth across regions. Governments worldwide are implementing measures to reduce greenhouse gas emissions, combat climate change, and promote sustainable development. As a result, building energy codes are being updated to include requirements for enhanced thermal performance and insulation levels.

In Europe, for instance, the Energy Performance of Buildings Directive (EPBD) sets minimum energy performance standards for new and existing buildings, including requirements for thermal insulation. Similarly, in the United States, the International Energy Conservation Code (IECC) establishes criteria for building envelope insulation, HVAC systems, and lighting efficiency to improve overall energy efficiency.

Compliance with these regulatory mandates necessitates the adoption of advanced insulation materials and construction techniques to achieve the prescribed energy performance targets. As a result, manufacturers and suppliers of technical insulation products are witnessing increased demand for their solutions, particularly those that offer high thermal resistance, durability, and environmental sustainability.

Urbanization and Industrialization

The ongoing trends of urbanization and industrialization are driving the demand for technical insulation solutions globally. As populations migrate to urban centers in search of employment opportunities and better living standards, there is a corresponding need for infrastructure development to accommodate growing urban populations.

Residential and commercial construction projects in urban areas require effective insulation solutions to ensure thermal comfort, indoor air quality, and energy efficiency. Proper insulation of buildings helps reduce heating and cooling loads, thereby lowering energy consumption and utility bills for occupants.

In addition to urban construction, industrial infrastructure projects are also driving demand for technical insulation products. The expansion of manufacturing facilities, power plants, refineries, and chemical processing plants necessitates the installation of insulation systems to maintain process temperatures, protect equipment, and ensure operational reliability.

Focus on Renewable Energy

The global transition towards renewable energy sources, such as solar, wind, and geothermal power, is creating new opportunities for the technical insulation market. Renewable energy technologies rely on efficient insulation systems to maximize energy capture, storage, and distribution while minimizing heat losses and environmental impact.

Solar photovoltaic (PV) systems, for example, require insulation materials to protect electrical components, minimize thermal losses, and optimize performance under varying weather conditions. Insulated piping and storage tanks are essential for solar thermal systems used for heating water or generating steam for industrial processes.

Similarly, wind turbines utilize insulation to protect critical components such as gearboxes, generators, and control systems from temperature extremes, moisture ingress, and mechanical wear. Insulated enclosures and thermal barriers help maintain stable operating conditions within turbine nacelles, ensuring reliable performance and longevity.

Geothermal heating and cooling systems also rely on effective insulation to enhance energy efficiency and thermal stability. Underground piping networks, heat exchangers, and thermal storage tanks are insulated to minimize heat loss during heat transfer processes, thereby improving system efficiency and reducing operating costs.

Forecast for the Technical Insulation Market

The outlook for the technical insulation market remains promising, with sustained growth expected in the coming years. Factors such as increasing investments in infrastructure development, regulatory support for energy efficiency initiatives, and the expansion of end-use industries will drive market expansion across regions.

Furthermore, advancements in insulation materials, manufacturing processes, and installation techniques will continue to drive innovation and product development in the technical insulation sector. Manufacturers are investing in research and development to enhance the performance, sustainability, and cost-effectiveness of their insulation products, thereby addressing evolving customer needs and market demands.

Regional Insights and Market Dynamics

North America

North America is a significant market for technical insulation products, driven by robust construction activity, industrial expansion, and regulatory mandates for energy efficiency. The United States and Canada are witnessing increased adoption of insulation solutions in residential, commercial, and industrial applications to meet stringent building codes and sustainability goals.

In the United States, initiatives such as the Department of Energy's Better Buildings Challenge and the Environmental Protection Agency's ENERGY STAR program are driving demand for energy-efficient building solutions, including insulation upgrades and retrofits. Building owners and facility managers are investing in insulation improvements to reduce energy consumption, lower operating costs, and enhance occupant comfort.

Inquire before buying, here: https://www.nextmsc.com/technical-insulation-market/inquire-before-buying

Europe

Europe leads the global technical insulation market, supported by stringent energy efficiency regulations, green building standards, and sustainability initiatives. Countries such as Germany, the United Kingdom, France, and Scandinavia are at the forefront of sustainable construction practices, driving demand for high-performance insulation materials and systems.

The European Union's Energy Efficiency Directive (EED) sets ambitious targets for reducing energy consumption and greenhouse gas emissions, spurring investments in energy-efficient building envelopes and HVAC systems. The nearly-zero energy building (NZEB) concept, which aims to minimize energy demand and maximize renewable energy use in new construction, is driving the adoption of advanced insulation solutions across Europe.

Asia Pacific

Asia Pacific is emerging as a lucrative market for technical insulation products, fueled by rapid urbanization, industrialization, and infrastructure development. Countries such as China, India, Japan, South Korea, and Australia are witnessing significant investments in residential, commercial, and industrial construction projects, driving demand for insulation materials and systems.

In China, the government's focus on sustainable development and green building initiatives is driving the adoption of energy-efficient building materials, including insulation products. The implementation of building energy codes and certification programs, such as Three-Star and Green Building Label, incentivizes developers and building owners to invest in insulation upgrades and energy-saving measures.

In India, the construction of smart cities, industrial corridors, and infrastructure projects is driving demand for technical insulation solutions to enhance energy efficiency, occupant comfort, and environmental sustainability. Insulation manufacturers are partnering with developers, architects, and contractors to promote the use of advanced insulation materials and construction techniques in building projects.

Latin America

Latin America is experiencing steady growth in the technical insulation market, driven by infrastructure investments, urban development, and regulatory measures to promote energy efficiency. Countries such as Brazil, Mexico, Argentina, and Chile are witnessing increased demand for insulation products in residential, commercial, and industrial applications.

In Brazil, the construction of new residential complexes, commercial buildings, and industrial facilities is driving demand for thermal insulation materials to improve energy efficiency and indoor comfort. The government's My House My Life program, aimed at providing affordable housing to low-income families, includes provisions for energy-efficient building design and insulation installation.

In Mexico, the implementation of building energy codes and standards is driving the adoption of insulation solutions in new construction and retrofit projects. The National Housing Commission (CONAVI) promotes sustainable building practices and energy-efficient technologies, encouraging developers to incorporate insulation upgrades and energy-saving measures in housing projects.

Middle East and Africa

The Middle East and Africa region is witnessing increasing demand for technical insulation products, driven by infrastructure development, urbanization, and industrial expansion. Countries such as Saudi Arabia, the United Arab Emirates, South Africa, and Nigeria are investing in construction projects and energy infrastructure, driving demand for insulation materials and systems.

In the Gulf Cooperation Council (GCC) countries, the construction of residential, commercial, and industrial buildings is driving demand for insulation solutions to mitigate heat transfer and enhance energy efficiency. Insulation manufacturers are leveraging innovative materials and technologies to address the region's unique climate challenges and regulatory requirements.

In South Africa, the government's focus on sustainable development and energy efficiency is driving investments in green building initiatives and renewable energy projects. The Green Building Council of South Africa (GBCSA) promotes green building practices and certification programs, incentivizing developers to incorporate insulation upgrades and energy-saving measures in building projects.

Conclusion

In conclusion, the Technical Insulation Market is poised for significant growth driven by evolving trends, regulatory mandates, and the need for sustainable solutions. Advancements in insulation materials, technological innovations, and market dynamics will continue to shape the industry landscape, presenting opportunities for stakeholders across the value chain.

As industries strive to enhance energy efficiency, reduce environmental impact, and comply with regulatory requirements, the demand for technical insulation solutions will continue to rise. Manufacturers, suppliers, contractors, and end-users must collaborate to develop and implement cost-effective, high-performance insulation solutions that meet the evolving needs of the market.

By embracing innovation, sustainability, and collaboration, the Technical Insulation Market can play a pivotal role in advancing energy conservation, environmental stewardship, and sustainable development worldwide.

#technical insulation#materials#chemicals#metals#minerals#business insights#market research#market trends

0 notes

Text

Double Sided Adhesive Tape Manufacturers: Innovating Bonding Solutions

Introduction:

Double-sided adhesive tapes double sided adhesive tape manufacturer have revolutionized the way we bond materials together. They offer versatility, convenience, and reliable adhesion, making them indispensable in various industries. Double-sided adhesive tape manufacturers play a crucial role in developing high-quality products that meet the diverse needs of their customers. In this article, we will explore the world of double-sided adhesive tape manufacturers, their manufacturing processes, product innovations, and their impact on different sectors.

Manufacturing Process and Expertise:

Double-sided adhesive tape manufacturers employ advanced manufacturing processes to produce tapes that deliver exceptional bonding performance. The process typically involves the following key steps:

a. Adhesive Formulation: Manufacturers carefully select and blend adhesive materials to achieve the desired properties, such as adhesion strength, temperature resistance, and durability. They may use various types of adhesives, including acrylic, rubber, silicone, or foam-based adhesives, depending on the application requirements.

b. Coating and Lamination: The adhesive formulation is then coated onto a carrier material, such as a film or a non-woven fabric. Precision coating techniques, such as reverse roll coating or hot-melt coating, ensure an even and consistent application of the adhesive. The adhesive-coated carrier is then laminated with a release liner for protection and ease of handling.

c. Slitting and Cutting: The laminated tape is slit into narrower widths and cut into desired lengths, catering to specific customer requirements. Manufacturers utilize high-precision slitting and cutting equipment to ensure uniformity and accuracy.

d. Quality Control: Stringent quality control measures are implemented throughout the manufacturing process. Manufacturers conduct rigorous testing to assess adhesive performance, dimensional accuracy, and overall tape quality. This ensures that the final product meets industry standards and customer expectations.

Product Innovations and Advancements:

Double-sided adhesive tape manufacturers are at the forefront of product innovation, constantly developing solutions to address evolving customer needs. Some notable advancements include:

a. High-Temperature Resistance: Manufacturers have engineered double-sided adhesive tapes with enhanced temperature resistance, allowing them to withstand extreme heat or cold conditions without compromising adhesion. These tapes find applications in the automotive, electronics, and aerospace industries.

b. Foam Tapes: Foam-based double-sided adhesive tapes provide excellent conformability, cushioning, and insulation properties. They are widely used in mounting applications, where irregular or textured surfaces need to be bonded securely.

c. Transparent Tapes: Transparent double-sided adhesive tapes are designed for inconspicuous bonding applications, where aesthetics are crucial. These tapes find applications in the signage, display, and retail industries.

d. VHB Tapes: VHB (Very High Bond) tapes are a specialized type of double-sided adhesive tape known for their exceptional bonding strength. They can bond a wide range of materials, including metals, plastics, and glass, without the need for mechanical fasteners.

e. Removable Tapes: Manufacturers have developed double-sided adhesive tapes with removable properties, allowing for temporary bonding or repositioning. These tapes find applications in the graphics, exhibition, and temporary signage industries.

Applications in Various Industries:

Double-sided adhesive tapes have found extensive applications in numerous industries:

a. Automotive: Double-sided adhesive tapes are used in the automotive industry for bonding components such as trims, emblems, and interior panels. They provide a strong and durable bond while reducing the need for mechanical fasteners, resulting in improved aesthetics and weight reduction.

b. Electronics: Double-sided adhesive tapes play a critical role in the electronics industry, where they are used for mounting components, securing displays, and managing heat dissipation. These tapes provide reliable adhesion, electrical insulation, and vibration damping properties.

c. Construction: Double-sided adhesive tapes are widely used in the construction industry for bonding materials such as metal panels, glass, and signage. They offer weather resistance, high bond strength, and ease of application, making them an ideal choice for architectural and structural applications.

d. Packaging: Double-sided adhesive tapes are employed in the packaging industry for carton sealing, splicing, and label attachment. They provide secure and tamper-evident bonding, ensuring the integrity and safety of packaged goods.

e. Medical: Double-sided adhesive tapes find applications in the medical industry for wound dressings, medical device assembly, and securement. These tapes are designed to be hypoallergenic, gentle on the skin, and provide reliable adhesion in challenging environments.

Global Reach and Industry Impact:

Double-sided adhesive tape manufacturers have a significant global presence and impact:

a. Market Expansion: Manufacturers cater to a broad customer base, ranging from small-scale businesses to multinational corporations. They supply tapes globally, meeting the demands of industries across regions.

b. Customization and OEM Partnerships: Double-sided adhesive tape manufacturers collaborate with customers to provide customized solutions tailored to specific requirements. They work closely with original equipment manufacturers (OEMs) to develop tapes that meet precise application needs.

c. Technological Collaboration: Manufacturers actively engage in collaborative partnerships with material suppliers, research institutions, and industry experts to drive technological advancements in double-sided adhesive tapes. These collaborations foster innovation, leading to the development of new tape formulations, improved performance, and novel applications.

d. Sustainability Initiatives: Double-sided adhesive tape manufacturers recognize the importance of sustainability and are taking measures to reduce their environmental footprint. They invest in eco-friendly materials, implement waste reduction strategies, and explore recyclable or biodegradable options.

Quality Assurance and Standards:

Double-sided adhesive tape manufacturers prioritize quality assurance to deliver reliable and consistent products. They adhere to international standards and certifications, such as ISO 9001, ISO 14001, and IATF 16949. Quality control processes encompass raw material testing, in-line inspections, and final product testing to ensure adherence to specifications and performance requirements.

Looking Ahead:

The future of double-sided adhesive tape manufacturing is poised for continued growth and innovation. Manufacturers will focus on addressing emerging industry trends and challenges, such as:

a. Miniaturization: As technology advances and devices become smaller, double-sided adhesive tapes will need to adapt to bond miniature components effectively. Manufacturers will develop ultra-thin tapes with high bond strength to meet these demands.

b. Sustainable Solutions: Manufacturers will continue to explore eco-friendly materials, recyclable options, and manufacturing processes that minimize environmental impact. They will work towards achieving sustainability goals and meeting customer demands for environmentally responsible products.

c. Advanced Bonding Solutions: Manufacturers will invest in research and development to create tapes with superior bonding performance in challenging applications. This includes adhesion to low surface energy substrates, high-temperature resistance, and enhanced durability.

d. Digitalization and Automation: Manufacturers will leverage digital technologies and automation to enhance production efficiency, improve quality control processes, and optimize supply chain management.

Conclusion:

Double-sided adhesive tape manufacturers play a vital role in providing innovative bonding solutions to industries worldwide. Their expertise, manufacturing capabilities, and commitment to quality have made them essential partners for a wide range of applications. As technology advances and market demands evolve, manufacturers will continue to push the boundaries of adhesive tape performance, ensuring reliable bonding solutions that meet the diverse needs of industries ranging from automotive and electronics to construction and medical. With their focus on innovation, sustainability, and customer-centric solutions, double-sided adhesive tape manufacturers are poised to shape the future of the adhesive industry.

0 notes

Text

0 notes

Text

Disk Type Shaper Cutters

Disk type shaper cutters are versatile tools used in machining processes to shape various materials, including wood, metal, and plastic. These cutters consist of a disk-shaped body with sharp cutting edges arranged around the circumference. They are commonly used in shaping operations where precise and intricate cuts are required.

One of the primary advantages of disk type shaper cutters is their ability to produce complex shapes with high accuracy. Their design allows for a wide range of cutting profiles to be achieved, making them suitable for a variety of applications, from creating decorative moldings to shaping gears and other components.

Additionally, disk type shaper cutters can operate at high speeds, enabling efficient material removal and reducing machining time. This speed, coupled with their precision, makes them valuable tools in industries where productivity and quality are paramount.

However, there are some limitations to consider when using disk type shaper cutters. Their effectiveness can be affected by factors such as the hardness and thickness of the material being cut, as well as the machine's power and stability. Furthermore, the complexity of the shapes they can produce may require careful planning and setup to ensure optimal results.

Disk-type shaper cutters find applications in various industries where precision shaping of materials is required. Some common applications include:

Woodworking: Disk-type shaper cutters are extensively used in woodworking for shaping edges, profiles, and contours on wooden workpieces. They can create intricate designs and smooth finishes on furniture components, cabinetry, moldings, and other wooden products.

Metalworking: In metalworking, disk-type shaper cutters are employed for cutting, shaping, and profiling metal components. They are used in industries such as automotive, aerospace, and machinery manufacturing for producing gears, sprockets, pulleys, and other metal parts with precise dimensions and surface finishes.

Plastic and Composite Materials: Disk-type shaper cutters are utilized in the fabrication of plastic and composite materials for shaping and trimming applications. They are commonly used in industries like automotive, electronics, and consumer goods manufacturing for producing plastic components, composite panels, and molded parts.

Foam Cutting: Disk-type shaper cutters are also employed in the foam processing industry for cutting and shaping foam materials used in furniture upholstery, packaging, insulation, and other applications. They help in achieving clean and accurate cuts on foam blocks and sheets.

Sign Making and Engraving: In the signage industry, disk-type shaper cutters are used for cutting and engraving various materials such as wood, plastic, acrylic, and metal. They enable the creation of intricate designs, letters, and patterns for signage, displays, and decorative purposes.

Ceramic and Stone Fabrication: Disk-type shaper cutters are employed in the fabrication of ceramic tiles, stone countertops, and other architectural elements. They help in cutting, profiling, and edging ceramic and stone materials to precise specifications for construction and interior design applications.

These are just a few examples of the diverse applications of disk-type shaper cutters across different industries. Their versatility, precision, and efficiency make them essential tools for shaping a

In conclusion, disk type shaper cutters are valuable tools for machining operations that require precision and versatility. While they offer numerous benefits, including the ability to create intricate shapes quickly and accurately, they also have limitations that need to be taken into account during the machining process. Overall, when used correctly, disk type shaper cutters can greatly enhance productivity and quality in various manufacturing applications.

0 notes

Text

At Foam Packaging Specialties we understand the responsibility of delivering packaging solutions without the fear of contamination. Our on-site ISO 7 (class 10,000) cleanroom allows us to custom manufacture, fabricate and assemble foam inserts and packaging solutions that meet your stringent quality production specifications. We specialize in creating custom designed packaging for the semiconductor, aerospace and medical industries with technical and environmental compliance. For more information, contact us today at (480) 966-6889 or click the link below:

#cleanroom#CleanRoomSolutions#cleanroomtechnology#cleanroomequipment#cleanroomdesign#iso7#packagingsolutions#packaging#CustomPackaging#productpackaging#foaminserts#arizonabusiness#Arizona

#packaging#custom packaging#protective packaging#foam packaging#iso 7#custom boxes#government contracts#packaging boxes

0 notes

Text

Navigating the Aerospace Grade Foam Core Materials Market Market: Trends and Insights by 2031

“Unpacking Aerospace Grade Foam Core Materials Market Market Share Dynamics: Insights from 2024 and Projections for 2032”

Global “Aerospace Grade Foam Core Materials Market Market” report offers a comprehensive analysis of market capacity, market share, ongoing trends, and forthcoming predictions. Its objective is to provide an in-depth examination of the global Aerospace Grade Foam Core Materials Market market segmented by product type, applications, and regions. The report delves into detailed analysis of Aerospace Grade Foam Core Materials Market, encompassing market size, share, growth, and demand forecasts. It also incorporates research methodology, value chain analysis, and industry insights regarding the power of suppliers and consumers. Additionally, the report highlights emerging technologies within the Aerospace Grade Foam Core Materials Market industry that will benefit our clients.

Get a Sample Copy of the Report at - https://www.marketresearchguru.com/enquiry/request-sample/1720

The Following Manufacturers Covered in the Aerospace Grade Foam Core Materials Market Market Report:

3A Composites Core Materials (U.S)

Amorim Cork Composites (Portugal)

Armacell (Luxembourg)

CoreLite (U.S)

DEFEX (U.S)

Evonik (Germany)

General Plastics (U.S)

Gurit (Switzerland)

Polyumac (Germany)

Diab (Sweden)

Market split by Type, can be divided into:

PVC Foam Core Materials

Polystyrene Foam Core Materials

Polyurethane Foam Core Materials

PMMA Foam Core Materials

Others

Market split by Application, can be divided into:

Exteriors

Interiors

Assembly Components

Others

Regional Analysis:

North America (United States, Canada and Mexico)

Europe (Germany, UK, France, Italy, Russia and Turkey etc.)

Asia-Pacific (China, Japan, Korea, India, Australia, Indonesia, Thailand, Philippines, Malaysia and Vietnam)

South America (Brazil etc.)

Middle East and Africa (Egypt and GCC Countries)

Inquire or Share Your Questions If Any Before the Purchasing This Report - https://www.marketresearchguru.com/enquiry/pre-order-enquiry/1720

The objective of this Aerospace Grade Foam Core Materials Market market research report is: –

To provide actionable intelligence alongside the Aerospace Grade Foam Core Materials Market market size of various segments.

To detail major factors influencing the Aerospace Grade Foam Core Materials Market market (drivers, opportunities, industry-specific challenges, and other critical issues).

To determine the geographic breakdown of the Aerospace Grade Foam Core Materials Market market in terms of detailed analysis and impact.

To analyze business dimensions with an eye on individual growth trends and contribution of upcoming Aerospace Grade Foam Core Materials Market market segments.

To track the competitive landscape of the market.

Key Questions Covered in Aerospace Grade Foam Core Materials Market Market Report:

What will be the Aerospace Grade Foam Core Materials Market market growth rate and value in 2031?

What are the Aerospace Grade Foam Core Materials Market market trends during the forecast period?

Who are the Major players in the keyword Industry?

What is driving and Restraining this sector?

What are the conditions to market growth?

What are the opportunities in this industry and segment risks faced by the main vendors?

What are the forces and weaknesses of the main vendors?

Purchase this Report (Price 3200 USD for a Single-User License) - https://marketresearchguru.com/purchase/1720

0 notes

Last Seen Blogs

bigfootsmom

hit me with ur car pls

salomewithfeather

Sal Writes

asadsailboat

hm

ksenex-blog

ksenex

mindseyedecor

Untitled