Last Seen Blogs

luis-aries

Mes Pas

lellu-0328-blog

♡i love jjba♡

creepyjoker

jokes on me

neeksxoxo

tsc, my entire will to live

agirlinacrazyworld

One Step Closer To Myself

Text

Loan borrowers are often confused why a major portion of EMI goes to interest and not the principal in the initial period of the loan

1. Is the Bank trying to make me pay more interest?

2. Is the Bank cheating me?

3. Why is such a big amount allocated to interest and not the principle?

These are the most common thoughts that come to a borrower who is a layman.

0 notes

Text

What is Oligopoly? Class 12, Economics

The word "Oligopoly" comes from two Greek words: oligo, which means "few" and polein, which means "sellers".

An oligopoly is a form of market wherein the market is dominated by small number of sellers. These sellers are called oligopolists.

A lot of industries in the developed economies are of oligopolistic form of market.

Close examples of oligopoly markets are:

(a) Credit Card Market in which a few players like Visa, Master Card and American Express dominate the whole market.

(b) Soft Drink Market in which Pepsi & Coca Cola dominate the whole market.

0 notes

Text

What are Fictitious Assets? - Bookkeeping and Accountancy

Fictitious Assets:

As the name suggests, these are not assets in a true sense. These generally include some one time heavy expenses which are not considered as an expense only in the year in which they were incurred. Rather, these expenses are shown as expenses over few accounting years. If the entire amount of these expenses is considered as an expense in the year of occurrence, these expenses may result in a big loss in that particular year. So these expenses are spread out over a few years.

For example, preliminary expenses. These are expenses incurred at the time of starting the business. If the entire amount of preliminary expenses is assigned to the first year only, it would result in a huge loss in the first year itself. So instead of treating the entire amount of preliminary expenses as an expense of the first year, these expenses would be spread out over a few accounting years. For example, say preliminary expenses are Rs.100/-. So what the firm may do is spread it over a period of say 5 years. So in the first year, only Rs.20/- (Rs.100 divided by 5) would be considered as preliminary expenses and balance Rs.80/- would be shown as an asset (fictitious asset) in the first year. During the second year, again Rs.20/- will be considered as preliminary expenses and balance Rs.60/- would be shown as an asset (fictitious) in the second year, so on and so forth. Thus, such expenses are spread out over a period of accounting years.

Another example would be discount on issue of shares/debentures.

0 notes

Text

What are Co-operative Banks? What are its Types?

Co-operative banks are the banks whose main objective is to provide financial assistance to economically weaker sections of the society.

Such banks are registered under the Cooperative Societies Act.

Examples of cooperative banks are The New India Cooperative Bank, Cosmos Co-op Bank etc.

There are three types of cooperative banks-

(a) Primary Credit Societies- These institutions are formed at village level or town level. The operations of such banks are limited to a very small area

(b) District Central Cooperative Banks- These banks operate at the district level. They act as a link between primary credit societies and state cooperative banks

(c) State Cooperative Banks- State Cooperative Banks are biggest forms of cooperative banks. They operate at the state level. Some of State Cooperative banks operate in multi States.

0 notes

Text

Difference between Intangible and Fictitious Assets

Intangible assets: These are the assets which do not have any physical existence. It is not possible to see, touch or feel them. For example, Goodwill (Goodwill is the reputation of the firm expressed in terms of money).

Fictitious Assets: As the name suggests, these are not assets in a true sense. These generally include some one time heavy expenses which are not considered as an expense only in the year in which they were incurred. If the entire amount of these expenses is considered as an expense in the year of occurrence, these expenses may result in a big loss in that particular year. So these expenses are spread out over a few years. For example, preliminary expenses. These are expenses incurred at the time of starting the business. If the entire amount of preliminary expenses is assigned to the first year only, it would result in a huge loss in the first year itself. So instead of treating the entire amount of preliminary expenses as an expense of the first year, these expenses would be spread out over a few accounting years. For example, say preliminary expenses are Rs.100/-. So what the firm may do is spread it over a period of say 5 years. So in the first year, only Rs.20/- (Rs.100 divided by 5) would be considered as preliminary expenses and balance Rs.80/- would be shown as an asset (fictitious asset) in the first year. During the second year, again Rs.20/- will be considered as preliminary expenses and balance Rs.60/- would be shown as an asset (fictitious) in the second year, so on and so forth. Thus, such expenses are spread out over a period of accounting years.

All fictitious assets are intangible, but not intangible assets are fictitious. For example, Goodwill is an intangible asset but not fictitious. Goodwill can be bought and sold.

0 notes

Text

What is Microeconomics? HSC/Class 11/12

Meaning of Microeconomics-

There are basically two branches of Economics - Microeconomics and Macroeconomics.

The word Microeconomics is derived from the Greek word 'Mikros' which means 'Small'.

Microeconomics is the branch of economics, which studies the behaviour of individual economic units like an individual buyer, individual seller, etc. Microeconomics deals with the study of economic issues related to such individual economic units.

Under Microeconomics, we split the economy into small individual units and then study each individual unit separately.

0 notes

Text

Social Responsibility of the Business towards the Owners-HSC/SYJC/Class 12

Responsibility towards owners:

1. Reasonable Profit- Owners/Shareholders invest money to earn profits. Hence every business has responsibility to earn a reasonable amount of profit for the owners

2. Finding New Business Opportunities- Every company should keep on finding new business opportunities. If it finds any good business opportunity, it should try to make use of that opportunity.

3. Expansion and diversification- Every company should keep growing its business through expansion or by diversification to new business opportunities.

4. Best Utilization of Capital- Every company should ensure that capital of the business is utilized in the best possible manner to generate maximum profit. The company has to ensure the safety of capital invested by the owners

5. Regular updates- It’s the responsibility of every company to give periodic information to the owners about the business. The information provided should be accurate and complete in all respects.

6. Fair Practices on stock exchanges- Any company should not involve itself in any unfair practices related to stock exchange like providing misleading information to the stock exchanges or trying to make profits from secret information about the business.

7. Minimizing wastages- Every company should make optimum utilization of all the available resources and should minimize wastages. Minimizing wastages lead to better productivity

8. Creating Goodwill- Every company is responsible for creating a very good image of the company by providing high-quality products and services to all the customers.

0 notes

Text

Types of Demand - HSC, Class 12/11 Economics.

Various Types of Demand:

Joint Demand - This refers to a kind of demand where products are demanded jointly. For example, Inkpen and ink.

Competitive Demand - This refers to demand of products which are close substitutes of each other. For example, tea and coffee.

Derived Demand - When the demand of a product is derived from the demand of any other product, such a demand is called derived demand. For example, cement. Cement is demanded not for direct consumption but is demanded as there is demand for housing.

Direct Demand - This refers to demand of products which are directly consumed by people. For example, all consumer electronics.

Composite Demand - This refers to the demand of the products which have multiple uses. For example, electricity.

0 notes

Text

Features of Utility - Class 11, HSC, Economics

Features of Utility-

Relative concept - Utility of a particular commodity changes from time to time and place to place. For example, the utility of umbrella is higher during monsoon season than in any other season.

Subjective concept - Utility of a particular commodity is not same for all the individuals. It differs from person to person.

Ethically Neutral - Study of Ethics deals with the study of what is good & what is bad, what is moral & what is immoral. The utility has nothing to do with ethics. Any commodity which has a want-satisfying power has utility. For example, Knife has utility in cooking at the same time it has utility for a murderer also

Utility and usefulness are not one and the same- Utility is different from usefulness. A commodity may have utility, but it may not be useful. For example, cigarette has a utility for a smoker, but it is not useful to him as it is injurious to health

Utility and pleasure are not one and the same - The commodity which has utility may not be pleasurable. For example, medicines/injections have utility during illness but are not pleasurable

Utility differs from satisfaction - Utility and satisfaction are two different terms. Satisfaction is the feeling that you get after consumption of a particular commodity. On the other hand, utility means expected satisfaction from a particular commodity.

Not measurable - You cannot measure utility. You can just experience it. You can just feel it, but you cannot express utility in numeric terms

Depends upon the intensity of want - Utility also depends on intensity of wants. For example, water has more utility for you when you are thirsty whereas its utility reduces if you are not thirsty.

Utility Forms Basis of demand - There will be a demand for a particular commodity only if it has utility.

0 notes

Text

Specialised Banks in India

Specialized Banks- These banks specialize in providing financial assistance to a particular industry or sector. For example, EXIM Bank, SIDBI, NABARD etc.

(a) EXIM Bank stands for Export-Import Bank. This Bank specializes in providing financial assistance to the import and export sector. The services of Exim Bank are Limited only to export and import sector. EXIM Bank provides all the required support to exporters and importers.

(b). SIDBI stands for Small Industries Development Bank of India. SIDBI specializes in providing financial assistance to small industries. They provide loans on easy terms to small industries

(c) NABARD stands for National Bank for Agricultural and Rural Development. NABARD specializes in providing financial support to the agricultural sector in the rural areas.

0 notes

Text

Major reasons behind rejection of a home loan application

Following are some of the most common reasons why your home loan application can get rejected-

1. Bad Credit History - If you have not paid your past loans regularly, most frontline institutions would reject your home loan application.

2. Title of the property is not clear - The property that you are purchasing should have a clear and marketable title. If the lender feels that the title of the property is not clear, the loan may be rejected

3. If the property you are buying falls in a negative area - Some banks do mark some areas as negative areas. These are generally the areas where recovery of the loans may be difficult or the areas where properties generally have structural issues. So if the property you intend to buy falls in the negative area of the bank to which you have applied for a home loan, your home loan application would be turned down

4. Dishonor of processing fee cheque - If the processing fees cheque gets dishonored, your home loan will not be disbursed.

5. Inter-Family Transactions - If you are buying the property from anyone who has a blood relation with you, your loan might get rejected, as most banks do not offer home loans on Inter-Family Transactions.

6. Cheque Bounces in your Bank a/c - Too many cheque bounces in your bank a/c may also lead to rejection of your loan.

7. Deliberate Hiding of some vital Information - It's always advisable to correctly reveal all the important information sought by the lender. A deliberate hiding of any material information may lead to immediate rejection of your loan.

0 notes

Text

Types of Commercial Banks in India

Commercial banks- Commercial banks are the banks which do the banking business with the aim of earning profits. They accept deposits from the public and lend them to traders, manufacturers, and businessmen. There are three types of commercial banks-

(a) Public sector banks- These are banks where the majority of the shares are held by the Government or the Reserve Bank of India. Examples of public sector banks are State Bank of India, Bank of Baroda, Bank of India etc.

(b) Private sector banks- These are the banks where the majority of shares are held by private individuals/entities. Example, HDFC Bank, ICICI Bank, Axis Bank etc.

(c) Foreign banks- These are the banks which are registered outside of India, but have their branches in India. Example, Citibank, Standard Chartered Bank, HSBC etc.

0 notes

Text

Do luxury goods have elastic demand? - Economics

Nature of Goods is one of the factors affecting elasticity of Demand -

Elasticity of demand also depends on whether the commodity is a necessity or a luxury.

Goods which are necessities tend to have inelastic demand whereas demand of luxury goods tend to be relatively elastic.

People generally prefer not to cut down consumption of necessities even in case of price increase.

However, in case of luxury products, a consumer may postpone his decision to buy the product if price is too high thereby making demand of luxury goods more elastic as compared to necessary goods.

0 notes

Text

Difference between Ltd (Limited) and Pvt Ltd (Private Limited)-Class 11

Both are forms of joint stock companies -

In simple words, a joint stock company is a form of business organization where there are multiple owners.

There are broadly 2 different types of Joint Stock Companies-

1. Private Limited Company and

2. Public Limited Company which is also referred to as ‘Limited Company’

What is a Private Limited Company?

In a private limited company, the minimum number of owners are 2 and maximum no of owners are 50.

Also in the case of a private limited company, there are restrictions on the transfer of shares. The shares of a private limited company cannot be transferred freely unlike public limited company where the shares can be transferred freely through a stock exchange.

A private limited company cannot invite the public to subscribe for its shares or debentures. A private limited company cannot accept deposits from anyone except its members (owners), directors or their relatives.

A private limited company must have a minimum paid up share capital of Rupees One Lakh. So before starting the business, the owners need to invest minimum One Lakh Rupees as the capital of their own pocket. All private limited companies must use the words "Private Limited" at the end of their name (Example, Xxx Pvt Ltd)

What is a Public Limited Company (Limited Company)?

A public company is a form of joint stock company which is not a private limited company

In the case of a public company, there is no restriction on transfer of its shares. The shares can be transferred freely through stock exchanges. There should be minimum 7 members (owners) in a public company

A public company must have a minimum paid up share capital of Rupees 5 lakhs. In other words, owners have to invest minimum Rupees Five Lakhs from their pocket in the company

A public company can invite public to subscribe to its shares. It can invite and accept deposits from public

There is no maximum limit on the number of members(owners) that a public company can have.

In the case of a public company, it is mandatory that the company must use word "Limited" after its name. For example Xxx Limited.

A public limited company must have at least 3 directors. Directors are the people elected by the shareholders/owners to run the business on their behalf.

0 notes

Text

Types of Bank Accounts-HSC, Class 12/11, Money and Banking

There are basically four different types of bank accounts.

They are as follows-

1. Current Account - This account is generally meant for businessmen. This is because they have a high frequency of bank transactions. Under this account, there is no restriction on the number of withdrawals and hence is most suitable for businessmen. Some current account holders are also given overdraft facility. The customer gets cheque book facility for current account

2. Savings Account - This account is made for the general public especially salaried people. The main objective of having the savings account is to cultivate the habit of saving among people. Interest is also paid by the banks on the savings account. However, there are restrictions on the number of withdrawals that can be made through savings account and hence this type of account is not suitable for businessmen. Customers are generally required to maintain a certain minimum balance in the account.

3. Recurring Deposit Account - This type of an account is also called as the cumulative time deposit account. It is meant to cultivate the habit of savings among economically weaker section of the society. Under this type of an account, the customer is allowed to deposit a certain small but fixed amount (Rs.50, Rs.100, Rs.500 etc.) every month for a fixed period of time. The customer gets back the total amount deposited along with interest at the end of the specified period.

4. Fixed Deposit Account - Under this type of account, a one-time lump-sum deposit is made by the customer for a fixed period of time (generally 3 months to 10 years). The customer cannot withdraw the amount during this period (These days most banks allow pre-mature withdrawal with a minor penalty). However, he can take a temporary loan against the fixed deposit receipt (FDR). At the end of the fixed period, the customer can either withdraw the amount or renew the fixed deposit.

Following hybrid account is also offered by a lot of banks now-

Multiple Option Deposit Account : It is a type of Saving Bank Account in which deposit in excess of a particular limit gets automatically transferred into Fixed Deposit. On the other hand, in case adequate fund is not available in our Saving Bank Account so as to honour a cheque that we have issued, the required amount gets automatically transferred from Fixed Deposit to the Saving Bank Account. The balance amount continues as Fixed Deposit and earns interest as per existing rate of interest. One can earn higher rate of interest from a Fixed Deposit Account than from a Saving Bank Account.

#bankaccounts#types#savingsaccounts#savingsaccount#currentaccounts#currentaccount#fixeddeposit#recurringdeposit

0 notes

Text

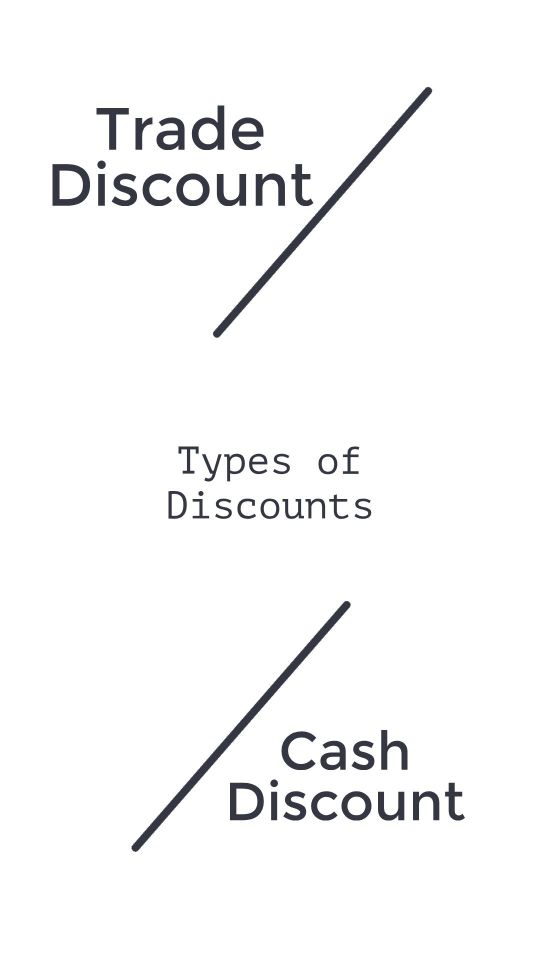

Trade Discount and Cash Discount Explained

Discounts - Discounts are of two types -

(a) Trade Discount. Trade discount means the discount given to the customer/purchaser on the printed price of the product. For example, if the printed price of a particular product is Rs.10,000/- and it is sold for Rs. 8,000/- by the firm, then Rs.2000/- is considered as a trade discount.

(b) Cash Discount - It means discount offered to someone for making a prompt payment or payment before the date on which the amount is due. It acts as an incentive for the customers/purchasers of the firm to make early payments to the firm.

0 notes

Text

Sundry Debtors and Sundry Creditors - Meaning

Debtors- Debtors refer to people who owe money to the firm on account of goods sold to them on credit. In other words, debtors are customers or purchasers who have purchased the goods from the firm on credit. However, this does not include loans and advances granted by the firm to someone.

Creditors - A person to whom the firm owes money due to the purchase of goods on credit from them is called as a creditor. So, creditors are the suppliers from whom business may have purchased the goods on credit. The term Creditors does not include any loans and advances taken or availed by the firm. If the business or the firm has taken some loan from the bank, then the bank would not be considered as a creditor of the firm.

The terms Sundry Debtors and Sundry Creditors are not defined clearly.

Sometimes,

The term Sundry Debtors is used to refer to sum total of all debtors and the term Sundry Creditors is used to refer to sum total of all creditors

And sometimes, the term Sundry Debtors is used to refer to sum total of small (miscellaneous) debtors and the term Sundry Creditors are used to refer to sum total of small (miscellaneous) creditors.

0 notes