#Limited Liability Partnership

Text

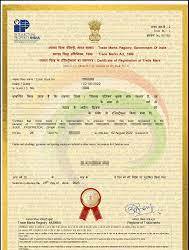

Online Trademark Registration Fees, Process, Documents

Trademark registration distinguishes your brand from competitors and help in identifying your product & services as source. Trademark could be a Name, Slogan, Logo or Number which a company uses on its business name, Product or services.

Registering a trademark could be a time taking process as brand registration could take minimum 6 months to 24 months of time depending upon the result of the Examination Report, that's why Professional Utilities provides Brand Name Search Report to get a fair idea about the turnaround time for registration.

Once a Trademark application is processed with the government department, applicants can start using the TM symbol on their mark & ® when the registration certificate has been issued. The registration of the trademark is valid for ten years & can be renewed after ten years. (Read More)

NOTE: If you are a manufacturer then you should also read about EPR Registration

#india#business#earnings#startup#trademark#intellectual property#intellectual disability#private limited company registration in chennai#private limited company registration in bangalore#private limited company registration online#sole proprietorship#limited liability partnership#limited liability company#ngo#ngo donation#nidhi company registration#partnership#partnership firm registration#manage business#taxes#income tax#management#accounting#entrepreneur#import export business#import export data#industry#commerce#government#marketplace

3 notes

·

View notes

Text

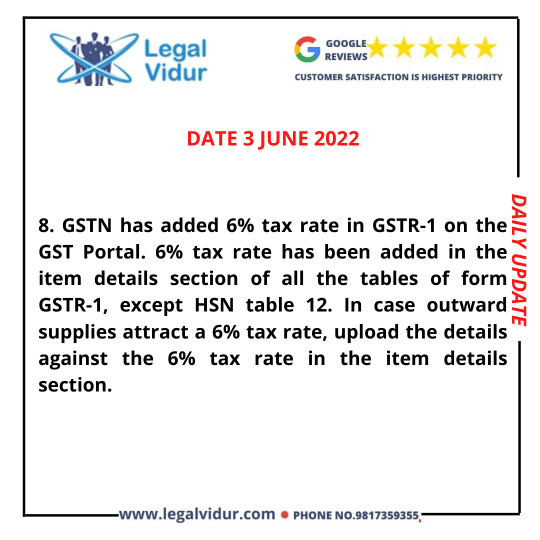

#Legal Vidur Daily Update

#Legal Vidur#Income Tax Return#One Person Company#Private Limited Company#Limited Liability Partnership#Public Limited Company#Startup India#FSSAI Registration#APEDA Registration#MSME Registration

2 notes

·

View notes

Text

Compliance for LLP in India

Once an LLP is incorporated, there is some mandatory compliance that an LLP is required to fulfill. If a Limited Liability Partnership fails to comply with these requirements, it may have to pay heavy penalties. Following is the list of vital compliance that an LLP needs to follow after the LLP Registration in India.

In India, LLP or Limited Liability Partnership enjoys a separate status and an organization needs to maintain its active status by regularly filing with MCA (Ministry of Corporate Affairs). Annual Compliance filing is compulsory for any LLP, whether having a business or not. LLP Compliance in India requires filing 2 separate forms. One form is for Annual Return and another one is for Statement of Accounts & Solvency. The forms are filed for reporting the activities & financial data for each Financial Year in the future. The failure to fulfill all the requirements for LLP Compliance levies an additional fee of Rs. 100 each day of a delay till the actual filing date. Hence, apart from the mandate, the heavy penalty compels the Partners to fulfill the requirements.

For LLP, the returns should be filed periodically to maintain compliance & avoid heavy penalties for non-compliance. An LLP has only a few compliances to be followed every year which is amazingly low as compared to the compliance requirements placed on the Private Limited Companies. Whilst non-compliance might only charge a Private Limited Company Rs. 1 lakh in terms of penalties and it might charge an LLP up to Rs. 5 lakhs.

Benefits of LLP Compliance in India

Following are some benefits of LLP Compliance in India:

1 : Easy Closer and Conversion of LLP: For the LLP Conversion into any other organization or company, annual filing is very important. Regular compliance records ease the conversion task. The same applies in the case of LLP Closure. Even if the Limited Liability Partnership was non-operational, the Registrar may ask to fulfill LLP Compliance, with an additional LLP filing fee (if applicable).

2 : Avoid Penalties: With an intention to avoid huge penalties & fees, regular filing of forms protects Partners from being declared as defaulters. It also avoids further disqualification of contracts. Hence, Limited Liability Partnership needs to fulfill the Annual Compliance requirements. The non-fulfillment of LLP Compliance adds up in the form of heavy penalties till the actual date of filing.

3 : High Credibility: Legal Compliance is the main requirement for any business in India. The status of the LLP Annual filing is shown in the Master Data of the Limited Liability Partnership on the MCA portal & any individual can access the same. For loan approvals or any other requirements, compliance is a primary criterion to measure the Company’s Credibility.

4 : Financial Worth Record: The Forms filed by the Limited Liability Partnership are accessible by Companies. Hence, while entering into major projects or contracts, the concerned party may also inspect the financial worth. The annual filing provides its financial worth record & capacity to an interested individual or party.

5: Greater Reputation: A vital requirement for any company is legal compliance. Anyone can access the Master Data of the LLP on the MCA portal to check the current status of the LLP Annual Filing. Compliance is a key factor in determining how trustworthy an organization or a Company is when approving loans or other needs of a similar nature.

0 notes

Text

https://eazybahi.com/limited-liability-partnership/

A Limited Liability Partnership (LLP) is a body corporate which is a distinct legal entity separate from that of its partners. It has perpetual succession and a common seal. It enjoys the benefits of a partnership firm while having the status of a body corporate.

Get Your Limited Liability Partnership registered along with name approval, PAN, TAN and GST registration and enjoys the benefits of a partnership firm at EazyBahi.

0 notes

Text

Limited Liability Partnership (LLP)

What is LLP?

LLP (limited liability partnership) is considered as a partnership in which a few or all company partners have limited liability. LLP is a legal entity separate from its partners.

What are the Characteristics of Limited Liability Partnership?

LLP provides your business a legal entity.

LLP requires less money to set up in comparison to other business forms including private limited company and public limited company.

Every partner in a LLP Company is liable to the business according to their contribution.

Limited liability partnership companies provide plenty of flexibility in terms of tax treatment. You have to file your LLC taxes or go for LLP Annual Filing as a sole proprietorship or as a partnership.

Advantages of LLP (limited liability Partnership)?

There are several advantages of a limited liability partnership firm and we have mentioned some of the key ones below.

No need of Minimum Capital Requirements

There is non requirement of minimum contribution in LLP. Limited liability partnership firms can be formed with the least capital amount.

No Limit on Partners and Owners

LLP needs a minimum of two partners and there is no limit on the maximum number of partners.

No Need of Audit

All organizations including private and public limited companies are needed to get their business accounts audited. However, in case of limited liability partnership, there is no need for compulsory audit.

0 notes

Text

Limited Liability Partnership (LLP): Bridging Security and Flexibility in Business Ventures

In the world of business, entrepreneurs are constantly seeking the ideal framework that balances liability protection and operational flexibility. The Limited Liability Partnership (LLP) has emerged as a popular business structure that fulfills this need, offering a unique blend of security and adaptability for various enterprises. Combining elements of traditional partnerships and corporations, an LLP provides entrepreneurs with a valuable tool to establish and grow their ventures while safeguarding their personal assets.

The fundamental characteristic of an LLP is the limited liability it offers to its partners. In a general partnership, partners are jointly and severally liable for the company's debts and obligations. This means that if the business faces financial troubles, the personal assets of individual partners can be at risk. However, in an LLP, partners enjoy limited liability, meaning their personal assets are shielded from the company's liabilities. This crucial aspect provides peace of mind to entrepreneurs, allowing them to focus on business growth without constant fear of personal financial ruin.

Forming an LLP involves compliance with specific regulatory requirements and filing the necessary documents with the appropriate government authorities. The process may vary depending on the jurisdiction, but typically, it includes providing essential details about the LLP, such as its name, address, partners' names, and their respective contributions. Once registered, the LLP gains a separate legal identity, capable of conducting business transactions, owning assets, and entering into contracts in its own name.

An LLP offers a unique advantage in terms of management and decision-making. Unlike corporations with rigid hierarchies, an LLP empowers partners to actively participate in running the business. This participatory management approach fosters collaboration and ensures that each partner's expertise is utilized effectively. Partners can collectively make strategic decisions and contribute to the business's growth, leading to a more inclusive and well-rounded organizational structure. Additionally, the flexibility in management allows partners to take on specific roles based on their strengths and interests, enhancing overall efficiency.

Furthermore, the tax treatment of an LLP is a significant benefit for both the business and its partners. The income earned by the LLP is not subject to entity-level taxation; instead, it "passes through" to the individual partners, who report their share of the profits on their personal tax returns. This pass-through taxation eliminates the issue of double taxation often faced by corporations, where both the company's profits and shareholders' dividends are taxed separately. As a result, an LLP can provide tax advantages and improved cash flow for the business and its partners.

LLPs are particularly well-suited for professional services firms, such as law firms, accounting practices, consulting agencies, and creative studios. These types of businesses often require collaboration among partners with diverse expertise. The limited liability and flexible management structure of an LLP create an ideal environment for professionals to work together seamlessly, share resources, and collectively build their ventures.

However, like any business structure, LLPs have certain considerations and limitations. While partners are protected from the actions of other partners, they may still be held personally liable for their own negligence or malpractice. It is essential for partners to maintain high professional standards and obtain appropriate insurance coverage to mitigate potential risks.

Additionally, the regulatory requirements and compliance obligations for LLPs may vary based on the jurisdiction in which the business operates. Entrepreneurs must ensure they stay informed and adhere to all legal obligations to maintain the LLP's status and fully enjoy its benefits.

In conclusion, the Limited Liability Partnership (LLP) stands as a compelling choice for entrepreneurs seeking a balanced business structure that provides liability protection and operational flexibility. With its limited liability feature, management adaptability, and tax advantages, an LLP offers a solid foundation for various enterprises to thrive and grow. However, a thorough understanding of the business's needs, compliance with legal requirements, and proactive risk management are crucial for maximizing the potential benefits of the LLP structure. When harnessed effectively, an LLP can be a valuable asset for entrepreneurs, bridging the gap between security and flexibility in their business ventures.

0 notes

Text

LIMITED LIABILITY PARTNERSHIP

Limited Liability Partnership is a different corporate business structure that combines a company's limited liability protections with a partnership's flexibility. For example, it can remain even if one of its partners changes. It can also hold assets in its name, enter into contracts on its behalf, and is liable for all its assets. However, the liability of the partners is only as significant as their agreed-upon investment in the LLP. Furthermore, none of the partners is liable for the independent or unlawful conduct of the other partners. Individual partners are therefore protected from joint liability brought about by another partner's bad business choices or wrongdoing.

In an LLP, the partners' mutual obligations and rights are governed. An agreement between the partners, or between the partners and the LLP, as the case may be, regulates the mutual rights and obligations of the partners within an LLP. Nonetheless, the LLP is still responsible for fulfilling its other obligations as a separate legal organization.

LLP is referred to as a hybrid between a company and a partnership since it has aspects of both a corporate structure and a firm partnership structure.

Features of Limited Liability Partnership:-

It has a separate legal entity, just like companies.

The liability of each partner is limited to the contribution made by the partner.

The cost of forming an LLP is low.

Less compliance and regulations.

No requirement for minimum capital contribution.

LLP REGISTRATION ONLINE

The steps to register a limited liability partnership online are as follows:-

1. Obtain Digital Signature Certificate (DSC)

You must apply for the designated partners of the proposed LLP's digital signature before starting the registration process. This is due to the fact that all LLP paperwork must be digitally signed and filed online. Therefore, the selected partner must acquire their digital signature certificates from certifying bodies that the government approves.

2. Apply for Director Identification Number (DIN)

All designated partners or those planning to become designated partners of the proposed LLP must submit applications for their DINs.

The needed papers, which are frequently Aadhaar and PAN, must be attached as scanned copies on the form. A full-time company secretary or the managing director, director, CEO, or chief financial officer of the current business in which the applicant will be appointed as a director must also sign the application.

3. Name Approval

The Limited Liability Partnership-Reserve Unique Name (LLP-RUN) form is submitted to reserve the name of the proposed LLP, and the Central Registration Center under the Non-STP category will handle it.

4. Incorporation of LLP

The FiLLiP (Form for incorporation of Limited Liability Partnership) is the document used for incorporation, and it must be filed with the Registrar, who has jurisdiction over the state where the LLP's registered office is located. The form is going to be incorporated.

5. File Limited Liability Partnership (LLP) Agreement

Documents Required for limited liability partnership

-PAN Card

PAN Card of each partner, if there's any foreign national may provide a passport

-Partners Address Proof

Aadhar Card/ Voter ID/ Passport/ Driving License of each partner

-Photograph

Passport-size photograph of each partner

-Business Address Proof

Electricity Bill/ Telephone Bill of the registered office address

-NOC from the owner

No Objection Certificate is to be obtained from the owner of the registered office

-Rent Agreement

The rent Agreement of the registered office should be provided, if any

LIMITED LIABILITY PARTNERSHIP REGISTRATION IN INDIA

An alternative business structure that combines a company's benefits with a partnership firm's adaptability is known as an LLP Registration in India. The Limited Liability Partnership Act of 2008 brought the LLP concept to India. Small- and medium-sized business establishments can use this unique hybrid.

In India, managing and forming a Limited Liability Partnership is simple. A minimum of two partners are needed to register an LLP; there is no maximum. The Partners' obligations and rights are outlined in the LLP agreement. One partner in an LLP is not liable for the wrongdoing and carelessness of the other partner. The partners are accountable for adhering to all the mentioned provisions in the LLP agreement.

Benefits of LLP registration in India

Partners' Liabilities are Limited

The fact that a Limited Liability Partnership counts as an independent legal identity is the primary benefit of registering as one as opposed to a Partnership Firm. As a result, LLP offers its partners the benefit of restricted liability. According to the LLP agreement, the partners' liability in case of a business loss or insolvency is limited to the capital contribution. Furthermore, neither partner is accountable for the negligence or misbehavior of the other partner.

Separate Legal Existence

Registering a limited liability partnership gives it a distinct legal identity from its partners. It can enter into agreements with other legal entities, file lawsuits, possess property, and take out loans in its name, thanks to the LLP Act of 2008. It also enables the company to continue operating independently and indefinitely, regardless of partner changes or deaths.

Operational Flexibility

The functional structure of an LLP, including the rights and obligations of the partners, is described in the LLP Agreement, a deed between the partners. The "Designated Member" who oversees daily operations is the norm for LLPs. Additionally, it may have members who are already established individuals or companies. Also, this structure enables us to identify the partners' roles and obligations clearly. Additionally, it might aid in defending the partner's interest in the event of loss brought on by another partner's illegal behavior.

Lower Compliance Requirement

Compared to Private Limited Businesses, LLPs have fewer compliance responsibilities. An audit is only required once a specific amount of turnover or contribution is completed. Unlike corporations, LLPs are exempt from compliance requirements pertaining to board meetings, statutory meetings, etc. Professional compliance services are frequently more affordable than those for businesses, making this type of formation more affordable to maintain

0 notes

Text

The LLP (Limited Liability Partnership) Agreement holds several benefits for the partners involved in the LLP:

Limited Liability: The primary advantage of an LLP is that it offers limited liability protection to its partners. This means that the personal assets of partners are not at risk for business debts and liabilities. Each partner is responsible for their actions, and they are not liable for the misconduct or negligence of other partners.

Flexible Management Structure: LLPs allow flexibility in the management structure. Partners can decide the roles and responsibilities of each partner according to their expertise and contribution to the business. This provides a more adaptable and customized management approach.

Ease of Formation: Forming an LLP is relatively straightforward and involves less paperwork and compliance compared to a private limited company. The registration process is quicker, making it a favorable option for startups and small businesses.

No Minimum Capital Requirement: LLPs do not require a minimum capital contribution, unlike private limited companies. Partners can contribute varying amounts of capital, depending on their agreed-upon terms.

Ease of Transfer of Ownership: The ownership interest in an LLP can be easily transferred or assigned to another person by way of a written agreement. This facilitates changes in ownership without affecting the LLP's legal existence.

Tax Benefits: LLPs offer the benefit of "pass-through taxation," where the LLP itself is not taxed. Instead, the profits are passed on to the partners, and they are individually taxed based on their share in the LLP.

Separate Legal Entity: Like a company, an LLP is a separate legal entity, which enhances its credibility and trustworthiness in the eyes of clients, suppliers, and financial institutions.

Perpetual Succession: LLPs have perpetual succession, meaning the LLP continues to exist even if one or more partners leave or new partners join. This ensures continuity in the business operations.

Confidentiality: LLP Agreements are not required to be filed publicly, which provides a level of confidentiality regarding the LLP's internal affairs and agreements among the partners.

Flexibility in Profit Sharing: LLP partners can agree on the distribution of profits based on their contributions, efforts, or any other mutually agreed-upon terms. This flexibility allows for more equitable profit-sharing arrangements.

Foreign Investment: LLPs can attract foreign investment as they offer a business structure with limited liability and simplified compliance requirements.

Regulatory Compliance: While LLPs have fewer compliance requirements compared to companies, they still offer a degree of regulatory structure, ensuring better governance and transparency within the organization.

Overall, the LLP Agreement provides partners with legal protection, operational flexibility, and taxation benefits, making it a preferred choice for certain types of businesses, especially those with a collaborative business structure. However, it is essential for partners to draft a comprehensive and well-defined LLP Agreement to address specific business needs and ensure smooth functioning throughout the partnership.

Read more: https://myefilings.com/format-of-supplementary-llp-agreement-for-admission-registration-of-partner/

#myefilings#business#taxes#india#company#limited liability partnership#private limited company#business registration#small business

0 notes

Text

https://taxesquire.in/limited-liability-partnership/

#company registration#chartered accountant#taxesquire#Limited Liability Partnership#register your business

0 notes

Text

Justifications for Selecting An LLP (Limited Liability Partnership)

LLP stands for a Limited Liability Partnership form. It is an alternative business form that offers limited liability protection for all businesses as well as the flexibility of a partnership. Changes in the partnership structure of the company have no impact on this kind of corporate structure. Many licensed professionals, including attorneys, doctors, accountants, and others, use this dynamic structure as their standard form of company organization. This business strategy is well regarded even in nations like the United States, the United Kingdom, Australia, and Germany.

An LLP's protection of individual partners from joint liability and the errors of other partners in a partnership firm is one of its key advantages. Even though there are other business structures available, the LLP structure is a popular option today. To fully grasp why, it is vital to go over the benefits of selecting LLP as your business structure. Continue reading to learn more about LLPs, as doing so will help you choose the most manageable and suitable company form for your startup.

Why Do You Want to Use an LLP Structure for Your Business?

Using an LLP as your business structure has many benefits. Let's examine them in greater detail:

Convenient Formation with Low Investment

A little Liability Partnership (LLP) enables partners to work together even if they have few resources because there is no minimum capital requirement for formation. Additionally, capital contributions can be made in any tangible form, including intangible assets, machinery, and land.

Having an Unlimited Number of Business Owners

As long as there are at least two members, an LLP may have any number of partners. The maximum number of partners an LLP can have is unrestricted.

Limited Liability

LLPs are distinct from the people who own them legally. The firm, not the members, is responsible for any liabilities incurred by LLP, including those for paying off debt or facing legal action.

Modularity in Management

The LLP Act of 2008 gives total authority over its business operations. The LLP agreement gives owners the freedom to choose how they want their company to function and grow. The LLP partners may also decide to assign the management of day-to-day operations to a managing partner or a committee run by partners. An LLP offers total management flexibility because its partners are free to divide duties according to their expertise.

Ability to File a Lawsuit

A Limited Liability Partnership has the legal capacity to bring claims on its own behalf and to be sued on behalf of others. The partners cannot be held accountable for unpaid dues.

Low Registration Fees

Compared to other business entities (public or private limited companies), an LLP has a low registration fee. The registration process is also rather simple, taking an average of 15 to 20 days to complete.

Pooling of Group Resources

The majority are created by a skilled and experienced team of experts, each with its own set of resources. They can each combine their capabilities to lower operating expenses while simultaneously boosting the company's potential for expansion.

Audits are optional.

Compared to limited liability companies, limited liability partnership firms benefit from different compliance advantages because audits are not required. For those launching an LLP, this is a considerable advantage. Only in cases where annual donations exceed 25 lakh rupees and annual revenue surpasses 40 lakh rupees are tax audits required.

Mid-Way Partner Entry or Exit

One further fundamental aspect is accommodated by the LLP agreement: new partners with their own businesses can be added and old partners can easily leave the company. However, the existing partners typically need to approve adding a new partner.

Taxation Outlook

The tax rate for limited liability firms is a flat 30% of their whole revenue. An LLP must also pay an additional 12% surcharge on the income tax if the total income is more than one crore rupees. In addition to the income tax plus surcharge, there is a 4% health and education cess that must be paid.

Final Verdict

A demand for the structure is created by the circumstance of a growing market. Businesses that offer services or operate in professional or technological domains benefit the most from a structure like this. Additionally, organisations who offer venture capital funds may find it useful.

Read Our Other Blogs to Know More about LLP- Some Ideas on Forming a Limited Liability Partnership for Your Small Business

#llp#limited liability partnership#llp registration#llp registration consultant#llp company#llp company registration

0 notes

Text

Make sure your company registration is completed right the first time by getting a top-notch guide from industry experts through fin Legal. Register your company now!

#registering a private limited company online#private limited company online#limited liability partnership#entrepreneurs

0 notes

Text

Limited Liability Partnership | Online Registration for Limited Liability Partnerships

0 notes

Text

How to Register an Online Limited Liability Partnership

LLPs, or LLPs for short, combine the benefits of partnerships and LLCs.In order to combine the advantages of partnership taxation with limited liability, LLPs were introduced in the Rajya Sabha on December 15, 2006.

There are fewer regulations that must be adhered to in an LLP than in a company, making it easier to establish and operate one.Learn more about how to register LL.P online in India.

Partners in an LLP can be any of the following:

A limited liability partnership is formed in accordance with the Limited Liability Partnership Act of 2008 (the Act).There is no limit on the number of partners in an LLP; individuals Limited Liability Partnerships Companies Foreign Limited Liability PartnershipsThe Act, on the other hand, requires at least two partners.You should follow the steps in this article to incorporate an LLP.

Step 1: For LLP designated partners to obtain, a Digital Signature Certificate (DSC) and a Designated Partner Identification Number are required.To electronically submit forms through the MCA portal, a DSC is required.Only organizations that have received government approval can provide DSCs.

After the DSC has been obtained, the Designated Partner Identification Number (DPIN) can be obtained by submitting Form DIR-3.In order to be considered a designated partner under the Act, you must satisfy this condition.Form DIR-3 requires both proof of identity and proof of residence.

Step 2: Reservation of the LLP's name Prior to forming a new LLP or converting an existing business or organization into one, the name must be reserved. Reservation requests can only be made through the MCA portal.The Reserve Unique Name-LLP (RUN-LLP) form must be completed before this application can be submitted.A name reservation request will be looked at by the Central Registration Centre (CRC) and, if possible, approved.

Step 3: A LLP Integrated Incorporation Form (FiLLiP) must be filed after the name has been reserved.The subscriber's form, which includes consent, the names and DPINs of the designated partners, the total contribution of each partner, the proposed or approved name of the limited liability company, the limited liability company's business activity, and the registered office's address.

Step 4: Certificate of Incorporation LLPs receive a Form 16 Incorporation Certificate upon successful registration.This certificate bears the LLP Identification Number (LLPIN).

Step 5: A Limited Liability Partnership Agreement specifies the rights and responsibilities of the partners and the LLP.After their LLP is registered, partners may enter into this agreement.The LLP agreement specifies the terms and conditions for admitting or removing partners, the consequences of death, and the division of profits and losses.Form 3 must be submitted to the RoC after the agreement has been registered and ratified by the partners. No agreement will change the partners' relationship with the LLP, which is governed by the First Schedule.

0 notes

Link

The Limited Liability Partnership Act, 2008" established LLP in India. Professionals, Micro, and Small Businesses that are family-owned or closely-held prefer LLP.

0 notes

Last Seen Blogs

babyfoxcollectionthings

Variette

graphitesblog

fantabulous thing

yourwholeworld

oops..

danielstock

The_Line

ahakivili

sheperd